"The global Homeland Security Market was valued at $ 478.2 billion in 2025 and is projected to reach $ 1045.9 billion by 2034, growing at a CAGR of 9.1%."

The Homeland Security Market encompasses a broad spectrum of technologies, services, and infrastructure aimed at protecting a nation’s citizens, assets, and critical infrastructure from natural and man-made threats. It includes segments such as border security, aviation and maritime security, cyber security, critical infrastructure protection, CBRN (chemical, biological, radiological, nuclear) defense, law enforcement, and emergency management. The market is primarily driven by rising geopolitical tensions, evolving terrorism threats, organized crime, and cyberattacks targeting critical systems. Governments worldwide are making significant investments in modernizing surveillance systems, enhancing emergency response networks, and upgrading national defense frameworks to safeguard both physical and digital domains. Innovations in biometrics, artificial intelligence, drone surveillance, and command & control systems are redefining how threats are detected and neutralized in real time.

The market is undergoing a significant transformation due to technological convergence and public-private partnerships. AI-enabled analytics, predictive policing platforms, and autonomous systems are enhancing situational awareness and decision-making in homeland security operations. Moreover, governments are increasingly focused on integrating cybersecurity measures within traditional security frameworks as cyber warfare becomes more prevalent. The pandemic also expanded the definition of homeland threats, bringing biosecurity and public health preparedness to the forefront. Across regions, North America leads the market with strong federal spending on border surveillance and cybersecurity, while Europe emphasizes counter-terrorism and civil protection. In Asia Pacific, rapid urbanization and rising cross-border threats are pushing countries like India, China, and South Korea to expand homeland defense capabilities. As climate change also introduces new vulnerabilities—from wildfire management to coastal defense—the homeland security market is evolving into a multi-disciplinary sector that blends military-grade technologies with civil resilience infrastructure. This evolution is attracting investments from both traditional defense contractors and emerging tech companies looking to offer integrated, next-generation homeland protection solutions.

Key Insights_ Homeland Security Market

-

The homeland security market is expanding rapidly due to escalating threats from terrorism, cyberattacks, and natural disasters, compelling governments worldwide to strengthen national security infrastructure across physical and digital domains.

-

Cybersecurity has emerged as the fastest-growing segment within homeland security, as state-sponsored cyberattacks, ransomware, and digital sabotage pose severe risks to government operations, defense systems, utilities, and financial networks.

-

Advanced surveillance technologies such as facial recognition, biometrics, AI-based video analytics, and UAVs (unmanned aerial vehicles) are transforming border and perimeter security by enabling real-time threat detection and automated response systems.

-

The integration of artificial intelligence and machine learning into command-and-control centers allows for predictive intelligence, risk modeling, and rapid situational analysis, especially useful for law enforcement and emergency response applications.

-

Governments are increasingly investing in CBRN (chemical, biological, radiological, and nuclear) defense systems to counter non-conventional warfare threats and bolster national preparedness against pandemics and biological incidents.

-

Public-private partnerships are playing a vital role in enhancing homeland security capabilities, with technology companies collaborating with government agencies to co-develop software platforms, secure networks, and emergency communication systems.

-

North America remains the dominant region due to consistent federal funding for cybersecurity, infrastructure protection, and counterterrorism initiatives, particularly in the United States, where the Department of Homeland Security spearheads comprehensive threat response programs.

-

In Europe, homeland security efforts are focusing on integrated border management, anti-radicalization measures, and cyber-resilience, particularly in response to increasing domestic terrorism and geopolitical unrest.

-

Asia Pacific is witnessing rapid growth driven by rising internal and cross-border threats, leading to major investments in smart city surveillance, biometric border control, and disaster management frameworks in countries like India and China.

-

The rise of climate-induced risks, including wildfires, floods, and hurricanes, has pushed governments to incorporate environmental resilience into their homeland security strategies, thereby broadening the scope of security preparedness beyond conventional threats.

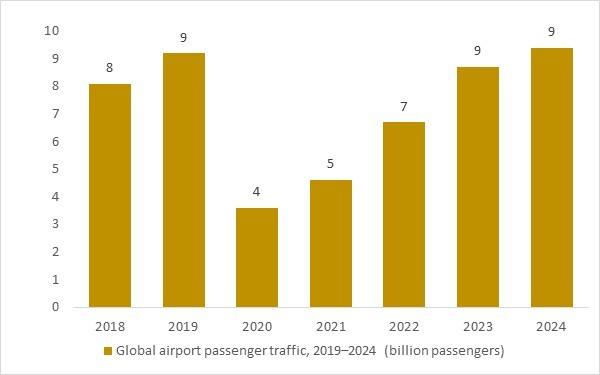

global airport passenger traffic, 2018–2024 (billion passengers)

Figure: Global airport passenger traffic fell from 9.2 billion passengers (2019) to 3.6 billion (2020), then recovered to 4.6 billion (2021) and 6.7 billion (2022) before rising to 8.7 billion (2023) and 9.4 billion (2024). This rebound expands the throughput base that directly drives homeland-security investments in aviation screening capacity, biometric identity verification/e-gates, perimeter surveillance, and command-and-control modernization at airports and key ports of entry.

Global airport passenger traffic—a direct throughput driver for aviation security and border-control operations—collapsed in 2020 and then rebounded strongly through 2024, returning above pre-pandemic levels. This recovery expands the operational load on airports and ports of entry, reinforcing sustained investment in higher-capacity checkpoint and hold-baggage screening systems, automated identity verification (biometrics/e-gates), integrated video surveillance and perimeter protection, and centralized command-and-control upgrades. As passenger volumes normalize at scale, homeland security demand increasingly shifts from temporary capacity fixes toward multi-year modernization programs focused on faster throughput, higher detection performance, and improved traveler experience while maintaining compliance with evolving threat scenarios.

North America Homeland Security Market Analysis

In North America, the homeland security market is well-established, with the United States being the primary driver through sustained federal spending on border protection, cybersecurity, counterterrorism, and disaster response. Government agencies continue to prioritize AI-based threat detection, critical infrastructure defense, and drone surveillance systems. The modernization of border management systems and emphasis on integrated cyber-physical security platforms offer strong opportunities for tech and defense firms. Additionally, climate-related challenges such as wildfires and hurricanes are prompting investments in emergency response technologies and environmental resilience programs.

The United States is the dominating country in the Homeland Security Market, driven by its extensive federal budget allocations, advanced technological infrastructure, and comprehensive threat mitigation strategies across cyber, border, aviation, and emergency response domains. The presence of key agencies like the Department of Homeland Security and strong collaboration with private defense and tech firms further solidify its leadership position globally.

Asia Pacific Homeland Security Market Analysis

The Asia Pacific homeland security market is expanding rapidly, fueled by increasing geopolitical tensions, insurgency threats, and the need for cross-border coordination. Countries such as China, India, South Korea, and Japan are heavily investing in smart surveillance networks, CBRN defense systems, and biometric access control technologies. Urbanization and growing cyber risks have led to enhanced focus on safeguarding digital infrastructure, smart cities, and public transportation hubs. This region presents high potential for global vendors offering scalable and cost-efficient security solutions tailored for large and diverse populations.

Europe Homeland Security Market Analysis

In Europe, homeland security efforts are shaped by the growing frequency of domestic terrorism, cyberattacks, and refugee management challenges. Governments across the region are strengthening border control through advanced monitoring systems, data-sharing protocols, and biometric verification. The adoption of AI and predictive analytics is accelerating in law enforcement and civil protection programs. Europe also shows increased commitment to climate security and critical infrastructure resilience, driving demand for multi-domain threat management solutions. The European market offers strong prospects for suppliers that comply with stringent regional data privacy and ethical security standards.

Report Scope

| Parameter | Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Type, By Technology, By End-User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Homeland Security Market Segmentation

By Type

- Border Security

- Aviation Security

- Maritime Security

- Critical Infrastructure Security

- Cyber Security

- Mass Transport Security

- Law Enforcement

- Corn (Chemical

- Biological

- Radiological And Nuclear) Security

- Other Type (First Responders

- Counter Terror Intelligence

- C3i

- And Pipeline Security)

By Technology

- Recognition And Surveillance Systems

- AI-based Solutions

- Security Platforms

- Other Technology (CBRN Solutions and Communication Platforms)

By End-User

- Public Sector

- Private Sector

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Companies Analysed

General Dynamics Corporation, L3Harris Technologies Inc., Leonardo S.p.A., Northrop Grumman Corporation, Thales Group, Unisys Corporation, FLIR Systems Inc., Raytheon Company, Leidos Holdings Inc., Boeing Company, Rafael Advanced Defense Systems Ltd., Elta Systems Ltd., Accenture plc, Lockheed Martin Corporation, BAE Systems plc, Elbit Systems ltd., Inter-Con Security Systems Inc., NetCentrics Corporation, Stealth Power, Adams Communication & Engineering Technology, ZeroEyes Inc., Evolv Technology, Uveye Inc., Red Balloon Security Inc., Aptima Inc., VideoRay LLC, Alphacore Inc., City Labs Inc., Fujitsu Limited, FJC Security Services Inc..

Recent Developments

July 2025 – U.S. President signed executive orders to accelerate domestic drone technology deployment and strengthen counter-UAS capabilities, paving the way for expanded commercial drone use and enhanced anti-drone systems for public safety agencies.

July 2025 – DHS Science & Technology Directorate launched Phase 2 of the Remote Identity Validation rally, challenging private-sector innovators to develop secure remote ID technologies for enhanced screening and fraud prevention in immigration and travel workflows.

July 2025 – A hearing was convened in the House Subcommittee on Counterterrorism to evaluate existing federal authorities on counter-unmanned aircraft systems (C-UAS) in law enforcement, highlighting a legislative push to update legal frameworks for drone threats.

June 2025 – Ondas Holdings partnered with Mistral Inc. to integrate its autonomous drone platforms (Optimus and Iron Drone Raider) into homeland security and defense markets, aiming to enhance aerial intelligence and counter-drone operations.

June 2025 – Senate Armed Services Committee proposed legislation to formally recognize combat drone pilots as veterans, extending access to healthcare and support services for personnel operating remotely piloted aircraft.

April 2025 – ICE awarded a $30 million contract to Palantir for its “ImmigrationOS” platform, leveraging real-time data analytics and biometrics to streamline tracking and enforcement of immigration and deportation processes.

July 2025 – DHS Science & Technology Directorate unveiled improvements to its MQ‑9 “Big Wing” drone capability and evaluated Blue UAS-approved systems, enhancing operational readiness for border surveillance and public safety missions.

FAQ's

The Global Homeland Security Market is estimated to generate USD 478.2 billion in revenue in 2025.

The Global Homeland Security Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 9.09% during the forecast period from 2025 to 2034.

The Homeland Security Market is estimated to reach USD 1045.9 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!