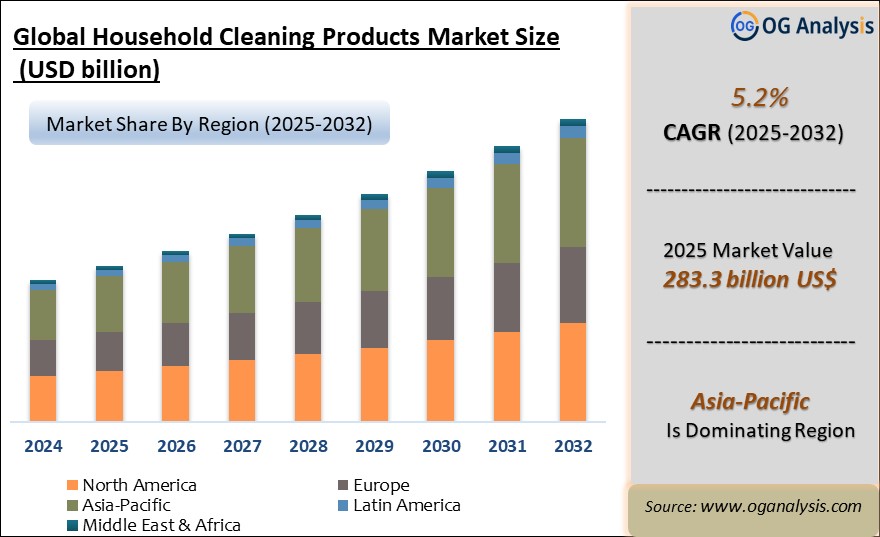

"The Global Household Cleaning Products Market Size was valued at USD 271.3 billion in 2024 and is projected to reach USD 283.3 billion in 2025. Worldwide sales of Household Cleaning Products are expected to grow at a significant CAGR of 5.2%, reaching USD 453.6 billion by the end of the forecast period in 2034."

Introduction and Overview

The Household Cleaning Products Market encompasses a wide array of goods designed to maintain hygiene and cleanliness in residential environments. This market includes items such as detergents, disinfectants, and multi-surface cleaners, which are integral to daily household upkeep. As urbanization and rising standards of living increase, so does the demand for effective and convenient cleaning solutions. Innovations in product formulations, along with the growing awareness of health and environmental concerns, are shaping the market landscape. With a heightened focus on sustainability and eco-friendly ingredients, the industry is experiencing a shift toward greener alternatives that align with consumers' preferences for safer and more responsible products.

In recent years, the Household Cleaning Products Market has witnessed a significant evolution driven by technological advancements and changing consumer behaviors. Companies are increasingly leveraging research and development to create products that not only deliver superior cleaning performance but also address specific consumer needs, such as hypoallergenic and natural formulations. The rise of e-commerce has further expanded market reach, offering consumers a wider selection of products and convenient purchasing options. This dynamic environment presents both opportunities and challenges for market players as they navigate the demands for innovation, quality, and sustainability in a competitive landscape.

Asia Pacific is the leading region in the Household Cleaning Products Market, propelled by rapid urbanization, increasing hygiene awareness, and a growing middle-class population with rising disposable incomes.

The surface cleaners segment is the dominating segment in the Household Cleaning Products Market, fueled by heightened consumer focus on cleanliness, frequent product innovation, and increased demand for disinfectant-based solutions, especially post-pandemic.

Trade Intelligence for Household Cleaning Products Market

| Global washing preparations, auxiliary washing preparations and cleaning Trade, Imports, USD million, 2020-24 | |||||

|

| 2020 | 2021 | 2022 | 2023 | 2024 |

| World | 17,563 | 18,140 | 1,154 | 623 | 187 |

| Guatemala | 48.3 | 56.2 | 80.3 | 99.1 | 104 |

| Trinidad and Tobago | 20.6 | 18.7 | 23.6 | 19.4 | 20.8 |

| Guyana | 6.8 | 11.2 | 11.4 | 13.4 | 12.9 |

| Barbados | 7.6 | 7.6 | 9.0 | 8.9 | 9.2 |

| French Polynesia | 9.3 | 8.2 | 9.7 | 8.3 | 5.7 |

| Source: OGAnalysis, International Trade Centre (ITC) | |||||

- Guatemala, Trinidad and Tobago, Guyana, Barbados and French Polynesia are the top five countries importing 81.6% of global washing preparations, auxiliary washing preparations and cleaning in 2024

- Global washing preparations, auxiliary washing preparations and cleaning Imports decreased by 98.9% between 2020 and 2024

- Guatemala accounts for 55.6% of global washing preparations, auxiliary washing preparations and cleaning trade in 2024

- Trinidad and Tobago accounts for 11.1% of global washing preparations, auxiliary washing preparations and cleaning trade in 2024

- Guyana accounts for 6.9% of global washing preparations, auxiliary washing preparations and cleaning trade in 2024

| Global washing preparations, auxiliary washing preparations and cleaning Export Prices, USD/Ton, 2020-24 |

|

|

| Source: OGAnalysis |

Household Cleaning Products Market Trends

One of the most notable trends in the Household Cleaning Products Market is the shift towards eco-friendly and sustainable solutions. Consumers are becoming increasingly conscious of the environmental impact of their choices, leading to a surge in demand for products made from natural, biodegradable ingredients. This trend is driving companies to invest in green chemistry and sustainable packaging, which not only appeal to eco-conscious buyers but also contribute to a reduction in the environmental footprint of cleaning products. Additionally, brands are adopting transparency in labeling to provide clear information about product ingredients and their environmental effects, enhancing consumer trust and loyalty.

Another significant trend is the growing popularity of multi-purpose and concentrated cleaning products. These products offer consumers convenience by reducing the number of different cleaners needed and minimizing packaging waste. Concentrated formulations also cater to the demand for more cost-effective solutions, as they often require smaller quantities for the same level of efficacy. The innovation in product design, such as easy-to-use dispensing systems and refillable options, further aligns with the modern consumer's preference for practicality and sustainability.

Technology integration is also reshaping the Household Cleaning Products Market. Smart cleaning devices and automated systems are becoming increasingly prevalent, offering advanced features such as IoT connectivity and programmable cleaning schedules. These innovations cater to the growing demand for convenience and efficiency in home maintenance. Additionally, companies are leveraging data analytics to better understand consumer preferences and optimize product development and marketing strategies. This technological advancement is enhancing the overall user experience and driving growth in the market.

Household Cleaning Products Market Drivers

The primary drivers of growth in the Household Cleaning Products Market include increasing urbanization and a rising focus on health and hygiene. As urban areas expand and living standards improve, the need for effective cleaning solutions grows. Consumers are more aware of the importance of maintaining a clean living environment to prevent health issues, which boosts demand for household cleaners. Additionally, the growing middle-class population in emerging markets is contributing to increased spending on home care products, further driving market growth.

Consumer preferences for convenience and time-saving solutions are also fueling market expansion. With busy lifestyles and dual-income households becoming more common, there is a higher demand for products that simplify cleaning tasks and offer quick and effective results. This trend is leading to the development of innovative products and cleaning systems that cater to the modern consumer's needs. The availability of a wide range of cleaning solutions through online platforms has also made it easier for consumers to access and purchase products, supporting market growth.

Regulatory pressures and increased awareness regarding environmental issues are driving the market towards sustainable practices. Governments and environmental organizations are implementing stricter regulations on the use of harmful chemicals and promoting eco-friendly alternatives. This regulatory environment encourages manufacturers to adopt greener practices and develop products with minimal environmental impact. The emphasis on corporate social responsibility and sustainable business practices is becoming a key factor in shaping market dynamics and influencing consumer preferences.

Household Cleaning Products Market Challenges

Despite the positive growth trajectory, the Household Cleaning Products Market faces several challenges. One of the primary issues is the high level of competition and market saturation, which makes it difficult for new entrants to establish themselves and for existing companies to differentiate their products. Additionally, fluctuating raw material costs and supply chain disruptions can impact production costs and product pricing. The need for continuous innovation to meet evolving consumer demands and regulatory requirements adds to the complexity and expense of maintaining a competitive edge in the market. Balancing sustainability with cost-effectiveness remains a significant challenge for many companies as they strive to align with consumer expectations while managing their operational expenses.

Market Players

1. Procter & Gamble Co.

2. Unilever PLC

3. SC Johnson & Son, Inc.

4. Colgate-Palmolive Company

5. Henkel AG & Co. KGaA

6. Reckitt Benckiser Group PLC

7. Clorox Company

8. Ecolab Inc.

9. Seventh Generation Inc.

10. Kirkland Signature (Costco)

Report Scope

| Parameter | Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By Distribution Channel |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Product Type

- Laundry Detergents

- Surface Cleaners

- Dishwashing Products

- Toilet Cleaners

- Others

By Distribution Channel

- Direct B2B

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Recent Developments

- P&G, Emami and Hindustan Unilever announced price reductions across household cleaning and personal care products, passing on benefits from lower tax rates to consumers.

- Reckitt confirmed the sale of its Essential Home cleaning products division, which includes brands like Cillit Bang and Air Wick, to Advent International, while retaining a minority stake.

- Neogen completed the divestment of its global cleaners and disinfectants business, transferring the unit to Kersia Group as part of its portfolio streamlining strategy.

FAQ's

The Household Cleaning Products Market is estimated to reach USD 407 billion by 2032.

The Global Household Cleaning Products Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 5.2% during the forecast period from 2025 to 2032.

The Global Household Cleaning Products Market is estimated to generate USD 271.3 billion in revenue in 2024.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!