"The Global Industrial Hose market Size was valued at USD 14.5 billion in 2024 and is projected to reach USD 15.2 billion in 2025. Worldwide sales of Industrial Hose are expected to grow at a significant CAGR of 5.6%, reaching USD 25.3 billion by the end of the forecast period in 2034."

Introduction and Overview

The industrial hose market is a dynamic sector driven by the extensive use of hoses across various industries, including manufacturing, construction, agriculture, and automotive. Industrial hoses are crucial for the transportation of fluids and gases, offering solutions for high-pressure, high-temperature, and chemical applications. Their versatility is evident in applications ranging from transferring water and oil to handling abrasive materials and toxic chemicals. The market is characterized by a diverse range of products designed to meet specific industry requirements, such as rubber, plastic, and metal hoses. The increasing industrial activities and infrastructural developments worldwide are bolstering the demand for industrial hoses, making them an essential component in modern industrial operations.

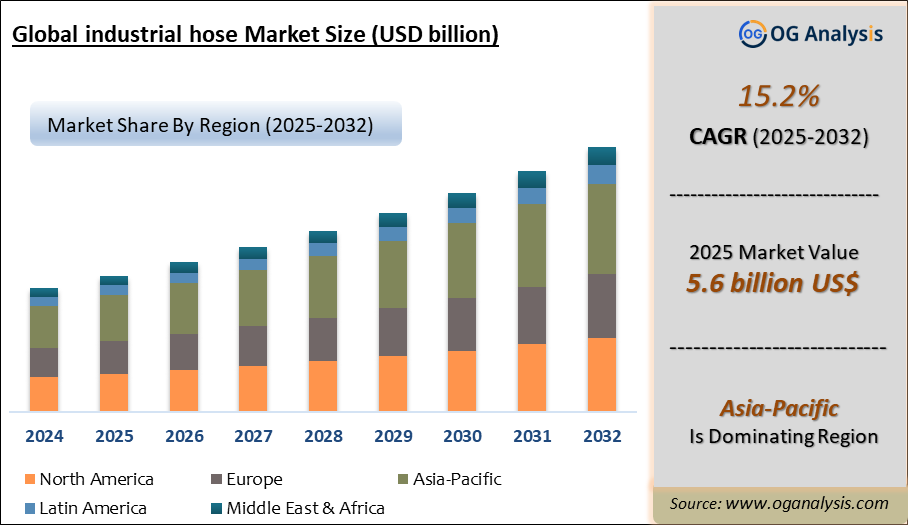

Regionally, the industrial hose market is experiencing significant growth in Asia-Pacific, driven by rapid industrialization and infrastructure development. Countries like China and India are investing heavily in industrial projects and manufacturing capabilities, fueling the demand for industrial hoses. Similarly, North America and Europe remain key markets due to their established industrial bases and advanced manufacturing technologies. The market dynamics are influenced by factors such as technological advancements, regulatory standards, and shifting consumer preferences. As industries evolve and seek more efficient and durable solutions, the industrial hose market is poised for continuous growth and innovation.

Asia-Pacific dominates the global industrial hose market, accounting for approximately 37.3% of the total share, driven by rapid industrialization and infrastructure development across China, India, and Southeast Asia. Among product segments, the rubber hose segment holds the largest market share, owing to its superior flexibility, durability, and widespread use in automotive and construction applications.

Global Rubber hoses, not reinforced, with fittings Trade, Imports, USD million, 2020-24

Trade Intelligence for industrial hose market

| Global Rubber hoses, not reinforced, with fittings Trade, Imports, USD million, 2020-24 | |||||

|

| 2020 | 2021 | 2022 | 2023 | 2024 |

| World | 602 | 698 | 707 | 740 | 736 |

| United States of America | 118 | 131 | 153 | 144 | 147 |

| Germany | 53.4 | 61.8 | 56.1 | 60.3 | 59.3 |

| Mexico | 35.2 | 37.5 | 42.4 | 49.9 | 46.4 |

| China | 41.4 | 37.9 | 34.1 | 35.8 | 36.5 |

| Brazil | 21.3 | 23.7 | 30.8 | 31.4 | 33.7 |

| Source: OGAnalysis, International Trade Centre (ITC) | |||||

- United States of America, Germany, Mexico, China and Brazil are the top five countries importing 43.8% of global Rubber hoses, not reinforced, with fittings in 2024

- Global Rubber hoses, not reinforced, with fittings Imports increased by 22.3% between 2020 and 2024

- United States of America accounts for 19.9% of global Rubber hoses, not reinforced, with fittings trade in 2024

- Germany accounts for 8.1% of global Rubber hoses, not reinforced, with fittings trade in 2024

- Mexico accounts for 6.3% of global Rubber hoses, not reinforced, with fittings trade in 2024

| Global Rubber hoses, not reinforced, with fittings Export Prices, USD/Ton, 2020-24 |

|

|

| Source: OGAnalysis |

Global industrial hose market-Latest Trends,Drivers,Challenges

One prominent trend in the industrial hose market is the increasing adoption of high-performance and specialized hoses. These hoses are designed to withstand extreme conditions, such as high temperatures, corrosive environments, and high pressures. The demand for hoses that can handle specialized fluids and gases, such as those used in the oil and gas industry or chemical processing, is rising. Manufacturers are focusing on developing hoses with enhanced durability and safety features, such as improved abrasion resistance and better chemical compatibility, to meet the stringent requirements of these demanding applications.

Another significant trend is the growing emphasis on sustainability and environmental impact. There is a push towards using eco-friendly materials and manufacturing processes in the production of industrial hoses. Companies are exploring alternatives to traditional materials, such as recycled plastics and biodegradable options, to reduce the environmental footprint of their products. Additionally, there is an increasing focus on designing hoses that are more energy-efficient and reduce the waste generated during their lifecycle. This trend reflects the broader industry shift towards sustainability and aligns with global environmental regulations and consumer expectations.

The integration of smart technology into industrial hoses is also gaining traction. Smart hoses equipped with sensors and monitoring systems are being developed to provide real-time data on pressure, temperature, and flow rates. This technology enables predictive maintenance, reduces downtime, and enhances operational efficiency. By leveraging advancements in IoT and data analytics, smart industrial hoses offer significant benefits in terms of performance optimization and safety. This trend is particularly relevant in industries where precise control and monitoring of fluid transfer are critical, such as in aerospace and petrochemicals.

Several key drivers are propelling the growth of the industrial hose market. One major driver is the expanding industrial and manufacturing sectors worldwide. As industries grow and diversify, the need for reliable and efficient hose solutions increases. Industrial hoses play a critical role in various processes, including fluid transfer, material handling, and equipment cooling, making them indispensable in modern industrial operations. The rise in infrastructure projects, particularly in emerging economies, further fuels the demand for industrial hoses as part of construction and development activities.

Technological advancements are another significant driver of market growth. Innovations in hose materials and design have led to the development of products with enhanced performance characteristics, such as higher pressure ratings, better chemical resistance, and improved durability. These advancements cater to the evolving needs of industries that require hoses capable of handling more demanding applications. The continuous research and development efforts by manufacturers to create specialized and high-performance hoses contribute to the market's expansion and competitiveness.

The increasing focus on safety and regulatory compliance is also driving the industrial hose market. Stricter regulations concerning industrial safety and environmental standards are prompting industries to invest in hoses that meet these requirements. For example, hoses used in hazardous environments must adhere to stringent safety standards to prevent leaks and accidents. The demand for hoses that comply with regulatory standards and provide reliable performance in critical applications is driving market growth and encouraging innovation in hose design and materials.

Despite its growth, the industrial hose market faces several challenges. One major issue is the variability in raw material prices, which can impact production costs and pricing stability. The cost of materials such as rubber, plastics, and metals can fluctuate based on market conditions and supply chain disruptions, affecting the overall cost of industrial hoses. Additionally, the market is highly competitive, with numerous players offering a wide range of products. This intense competition can lead to price wars and pressure on profit margins, challenging manufacturers to balance cost and quality. Furthermore, the need to continuously innovate and meet evolving industry standards adds to the complexity of operating in this market. Manufacturers must navigate these challenges while striving to deliver high-quality and cost-effective hose solutions to maintain their market position.

Market Players

1. Colex International Limited

2. Dyna Flex, Inc.

3. Eaton

4. Flexaust Inc.

5. Hose Master LLC

6. Kanaflex Corporation Co.,ltd.

7. KURIYAMA OF AMERICA, INC.

8. Kurt Manufacturing

9. MerlettTecnoplasticSpA

10. NORRES Schlauchtechnik GmbH

Report Scope

| Parameter | industrial hose market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By Material Type, By End-Use Industry, By Distribution Channel |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Product Type

- Rubber Hoses

- Plastic Hoses

- Metal Hoses

- Composite Hoses

By Material Type

- Natural Rubber

- Nitrile Rubber

- PVC

- PU (Polyurethane)

- Stainless Steel

- Others

By End-Use Industry

- Oil & Gas

- Chemical

- Mining

- Water & Wastewater

- Automotive

- Food & Beverage

- Construction

- Others

By Distribution Channel

- Online Retail

- Offline Retail (Specialized Stores)

- Direct Sales (B2B)

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Recent Developments

- JRE Private Limited announced delivery of advanced rubber hoses and couplings tailored for harsh-environment industrial use.

- Parker Hannifin, Gates, and Continental were recognized as leaders in digital, motion control, and fluid power innovation in an industry evaluation report.

- TIPCO’s Alternative Hose opened its fourth Arizona facility in Tucson to strengthen local service and inventory access.

- Alternative Hose Inc. revealed plans to open a sixth branch in Ontario, California, featuring a flagship showroom, lounge, and fluid-power museum.

- Unisource Manufacturing Inc. celebrated its 45th anniversary, reinforcing its long-standing presence in the industrial hose sector.

- Continental (ContiTech) commissioned a new €3 million production line in Korbach for high-pressure hydrogen hoses, aimed at hydrogen refueling and transport infrastructure.

- PIRTEK USA expanded with 20 new territories and 10 new locations, including its first branches in Kansas and Delaware.

- Gates introduced “Data Master MegaFlex,” a large-diameter cooling hose designed specifically for data center applications.

- NRP Jones was awarded “Domestic Hose Manufacturer of the Year,” emphasizing its role in U.S. oilfield and hydraulic hose manufacturing.

FAQ's

The Industrial Hose Market is estimated to reach USD 22.4 billion by 2032.

The Global Industrial Hose Market is estimated to generate USD 14.5 billion in revenue in 2024.

The Global Industrial Hose Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 5.6% during the forecast period from 2025 to 2032.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!