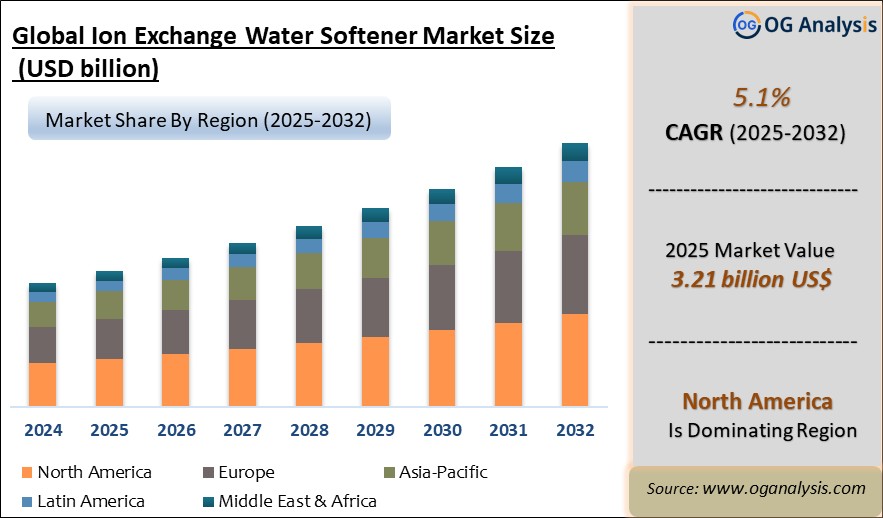

"The Global Ion Exchange Water Softener Market Size is valued at USD 3.21 Billion in 2025. Worldwide sales of Ion Exchange Water Softener Market are expected to grow at a significant CAGR of 5.1%, reaching USD 4.53 Billion by the end of the forecast period in 2032."

The Ion Exchange Water Softener Market is a vital segment of the global water treatment industry, providing solutions to reduce water hardness by removing calcium and magnesium ions through the ion exchange process. These systems are widely used in residential, commercial, and industrial applications where hard water can cause scaling, reduce the efficiency of appliances, and affect product quality in manufacturing. The core technology involves passing hard water through a resin bed that exchanges hardness ions with sodium or potassium ions, delivering softened water downstream. With the increasing need for efficient water use, appliance longevity, and reduced energy consumption, ion exchange water softeners are being adopted not only in homes and offices but also in sectors like food & beverage, hospitality, healthcare, and textiles where water quality directly impacts operations and compliance.

In 2024, the market is seeing strong momentum driven by the growing awareness of water quality issues, particularly in urban regions facing hard water challenges. Manufacturers are focusing on developing compact, digitally controlled softening units that offer remote monitoring, automated regeneration cycles, and efficient salt usage. Regulatory frameworks promoting water conservation and energy efficiency are also influencing product design and innovation. Asia-Pacific is emerging as a high-growth region due to urbanization and industrial expansion, while North America and Europe maintain strong demand due to higher awareness and mature infrastructure. Additionally, smart home integration and sustainability trends are influencing buyer behavior, pushing demand for systems that provide performance analytics and reduce environmental footprint. With the rise in consumer preferences for low-maintenance and long-lasting systems, companies are emphasizing extended warranty models and service-inclusive offerings to capture long-term customer loyalty.

North America is the leading region in the ion exchange water softener market, fueled by high consumer awareness, established residential infrastructure, and stringent water quality regulations.The residential segment is the dominating segment in the ion exchange water softener market, propelled by rising concerns over hard water, increasing adoption of in-home water treatment solutions, and growing emphasis on health and appliance longevity.

Key Takeaways – Ion Exchange Water Softener Market

- Ion exchange water softeners are essential in preventing scaling and corrosion in plumbing systems, industrial machinery, and household appliances.

- Residential demand is growing as more consumers seek solutions for hard water problems that affect cleaning efficiency, skin health, and appliance durability.

- Digital and automated water softeners with programmable regeneration and smart diagnostics are becoming the industry standard.

- Water-intensive industries like textile, healthcare, and food & beverage are key adopters due to the impact of water quality on product consistency and compliance.

- Sustainability is influencing product development, with innovations focused on salt-saving, energy-efficient regeneration, and longer resin lifespans.

- One major driver is increased urbanization and infrastructure development, especially in emerging economies where hard water issues are widespread.

- Asia-Pacific is the fastest-growing regional market due to rising urban populations, increased water stress, and demand for compact water treatment systems.

- North America and Europe dominate in terms of mature usage patterns, high product penetration, and strong after-sales service infrastructure.

- Challenges include high initial system costs and the need for routine maintenance, which may deter budget-sensitive consumers.

- Another challenge is the growing scrutiny on sodium discharge from softeners, prompting interest in alternative regeneration technologies.

- Smart integration with home automation and IoT platforms is creating a new wave of consumer engagement and data-driven system optimization.

- Companies are enhancing their offerings with value-added services such as on-site testing, installation support, and extended service contracts.

- Retailers and e-commerce platforms are expanding product access, particularly for DIY-friendly units and compact residential systems.

- Product bundling with filtration and purification technologies is becoming a common sales strategy to offer complete water treatment solutions.

- Strategic partnerships between resin suppliers and equipment manufacturers are supporting innovation in long-life and eco-friendly ion exchange media.

Market Scope

| Parameter | Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By Application, By End User, By Technology, By Distribution Channel |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Ion Exchange Water Softener Market Segmentation

By Type

- Residential

- Commercial

- Industrial

By Application

- Household

- Municipal

- Industrial Process

By End User

- Residential Users

- Hospitality

- Food & Beverage

- Pharmaceutical

By Technology

- Single Tank Systems

- Twin Tank Systems

By Distribution Channel

- Online

- Offline

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Top 15 Companies Operating in the Ion Exchange Water Softener Market

- Culligan International Company

- EcoWater Systems LLC

- Kinetico Incorporated

- A. O. Smith Corporation

- 3M Company

- Pentair plc

- GE Appliances (a Haier company)

- Canature Environmental Products Co., Ltd.

- Whirlpool Corporation

- Harvey Water Softeners Ltd.

- Ion Exchange (India) Ltd.

- Hydranautics (a Nitto Group company)

- AXEON Water Technologies

- Watts Water Technologies, Inc.

- Soft Water Systems Inc.

FAQ's

The Global Ion Exchange Water Softener Market is estimated to generate USD 3.21 Billion in revenue in 2025.

The Global Ion Exchange Water Softener Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 5.1% during the forecast period from 2025 to 2032.

The Ion Exchange Water Softener Market is estimated to reach USD 4.53 Billion by 2032.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!