"The Metaverse Market was valued at $ 152.22 billion in 2025 and is projected to reach $ 2106 billion by 2034, growing at a CAGR of 33.9%."

The metaverse market is an emerging and transformative digital domain that merges augmented reality (AR), virtual reality (VR), blockchain, artificial intelligence (AI), and advanced connectivity to create shared, persistent, and highly immersive virtual environments. Within these interconnected 3D spaces, users can interact socially, conduct business, learn, play, and explore digital worlds in real time. The concept extends beyond gaming into a full-fledged digital economy, where virtual goods, real estate, services, and events hold tangible value. Enabled by blockchain technology, digital currencies, and non-fungible tokens (NFTs), the metaverse allows for secure ownership, trade, and monetization of virtual assets. Market growth is being fueled by increasing consumer interest in immersive entertainment, the evolution of social media into 3D interactive platforms, and enterprise investments in digital transformation. Enhanced by the rollout of 5G and edge computing, the metaverse offers low-latency, high-fidelity experiences that are becoming increasingly accessible to global audiences.

The evolution of the metaverse market is also reshaping industries such as retail, healthcare, manufacturing, education, and real estate by enabling innovative business models and operational efficiencies. Enterprises are utilizing virtual environments for collaborative workspaces, immersive training programs, digital twin simulations, and customer engagement strategies. This transformation is creating new opportunities for technology providers, developers, and content creators to build tools, applications, and platforms that support interoperability, identity management, and cross-platform integration. Meanwhile, challenges around data privacy, security, intellectual property rights, and ethical governance are prompting discussions among policymakers, industry leaders, and technology communities. As hardware such as VR headsets and AR glasses becomes more affordable and content creation tools evolve, the metaverse is expected to shift from niche adoption to widespread integration into daily life and enterprise operations, solidifying its role as a key driver of the next digital economy.

Key Market Insights

- The metaverse market is expanding rapidly as advancements in AR, VR, AI, blockchain, and high-speed connectivity converge to create immersive, persistent virtual environments. These technologies collectively enable users to engage in social, commercial, and creative activities within dynamic 3D spaces, driving both consumer and enterprise adoption.

- Gaming remains the primary gateway to the metaverse, but its applications are diversifying into sectors such as education, retail, healthcare, manufacturing, and real estate. Immersive training, digital showrooms, virtual tourism, and remote collaboration are emerging as high-value use cases fueling market penetration.

- Blockchain integration is a core enabler of the metaverse economy, facilitating secure ownership and trade of virtual assets through NFTs and digital currencies. This capability is fostering new revenue streams for creators, brands, and developers while supporting decentralized governance models.

- The rollout of 5G and advancements in edge computing are critical to delivering low-latency, high-fidelity metaverse experiences. These infrastructure developments enhance real-time interactions, enable richer graphics, and expand access to mobile-based immersive environments.

- Interoperability is a key market focus, with technology providers working on platforms and standards that allow seamless movement of assets, avatars, and experiences across different virtual worlds. Achieving this will be essential for sustaining user engagement and ecosystem growth.

- Virtual commerce is gaining momentum as brands create immersive shopping environments where consumers can explore products, customize options, and complete transactions entirely within the metaverse. This is transforming traditional e-commerce into experiential retail.

- Digital twin technology is emerging as a significant metaverse application, enabling real-time simulations of physical assets, processes, and environments for industries such as manufacturing, energy, and infrastructure. This supports predictive maintenance, operational efficiency, and strategic planning.

- Data privacy and cybersecurity are increasingly critical concerns, as metaverse platforms handle vast amounts of personal, behavioral, and transactional data. Developers are prioritizing encryption, identity verification, and compliance frameworks to safeguard users.

- Content creation tools are evolving to support low-code and no-code development, enabling a wider range of creators to design immersive experiences. This democratization of content production is accelerating the pace of innovation and diversity in metaverse offerings.

- Investment in metaverse startups and infrastructure is accelerating, with technology giants, venture capital firms, and governments allocating substantial resources to build the foundation of the virtual economy. Strategic partnerships and acquisitions are becoming common to strengthen market positions.

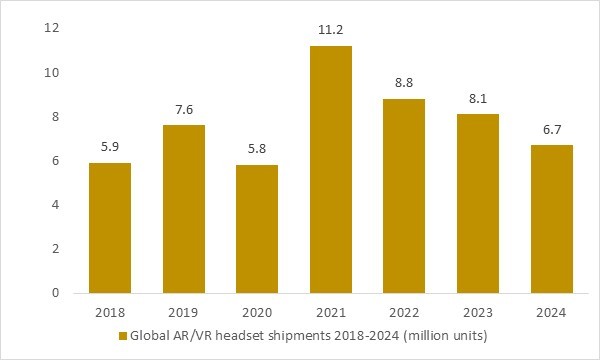

Global AR/VR headset shipments 2018-2024 (million units)

Figure: Global AR/VR headset shipments increased from 5.9 million units in 2018 to a peak of 11.2 million units in 2021, before moderating to an estimated 6.7 million units in 2024e, reflecting the hardware adoption cycle shaping metaverse user reach. As immersive devices become more capable and accessible, enterprises and consumers expand use cases across gaming, social interaction, training simulations, and virtual collaboration, strengthening platform engagement and content monetization potential. OG Analysis estimates, derived from global XR device shipment tracking and industry market studies, illustrate how the installed-base trajectory influences developer investment, ecosystem maturity, and long-term growth opportunities in the metaverse market.

- Global AR/VR headset shipments rose from 5.9 million units in 2018 to a peak of 11.2 million units in 2021, signaling rapid expansion of metaverse-ready hardware adoption. Shipments then moderated to 8.8 million units in 2022 and 8.1 million units in 2023 as the market entered a consolidation phase. The estimated 6.7 million units in 2024e reflect short-term demand normalization amid pricing, content maturity, and enterprise ROI considerations. Overall, this shipment trajectory highlights that near-term metaverse growth is increasingly driven by software depth, enterprise use cases, and ecosystem engagement rather than hardware volumes alone.

Regional Insights

North America Metaverse Market

North America’s metaverse market is driven by robust content ecosystems, cloud and edge infrastructure maturity, and strong enterprise experimentation across retail, media, education, healthcare, and manufacturing. Market dynamics emphasize user engagement, monetization models for virtual goods and services, and interoperability across engines, identity, and payments. Lucrative opportunities include immersive commerce pilots, virtual workforce training, live events with multi-platform distribution, and digital twin programs that connect operational data to 3D experiences. Latest trends feature mixed reality devices integrated with AI copilots, low-latency streaming over 5G/edge, creator economy toolchains, and privacy-preserving identity frameworks. The forecast points to steady adoption as hardware becomes lighter, platforms consolidate around open standards, and enterprises shift from pilots to scaled deployments. Recent developments highlight SDK unification across devices, enterprise-grade avatar and asset pipelines, and partnerships linking metaverse platforms with digital twins, product lifecycle systems, and marketing stacks.

Asia Pacific Metaverse Market

Asia Pacific exhibits the fastest-evolving metaverse landscape, propelled by mobile-first consumers, dense 5G rollouts, gaming leadership, and public-sector smart city initiatives. Market dynamics focus on scalable content distribution, localized creator ecosystems, and super-app integration of virtual experiences. Companies see high-value opportunities in virtual storefronts for cross-border commerce, education and language learning, entertainment IP extensions, and industrial training tied to advanced manufacturing hubs. Latest trends include lightweight XR hardware tuned for mobile chipsets, real-time translation in social worlds, telco-led edge marketplaces, and micro-payment rails embedded in metaverse apps. The outlook signals broad-based growth as SMEs adopt turnkey world-building tools and brands use virtual events to reach regional audiences. Recent developments center on co-creation programs between game studios and consumer brands, university-industry labs for spatial computing, and device-certification tracks that speed content to market.

Europe Metaverse Market

Europe’s metaverse market is shaped by stringent data protection rules, digital sovereignty priorities, and strong industrial design and engineering capabilities. Market dynamics prioritize standards-based interoperability, accessibility, safety-by-design, and trusted identity across consumer and enterprise use cases. Lucrative opportunities arise in immersive retail and tourism, cultural heritage digitization, remote healthcare support, and industrial digital twins for sustainability and productivity gains. Latest trends feature open-source engines, spatial computing aligned with EU guidelines, carbon-aware rendering workflows, and secure wallets supporting verifiable credentials. The forecast indicates resilient expansion as organizations adopt federated data spaces and integrate metaverse layers into existing ERP, PLM, and training systems. Recent developments include cross-border consortia for cultural and industrial use cases, public funding for XR skills pipelines, and vendor roadmaps that harden compliance, auditability, and accessibility features for regulated environments.

Report Scope

| Parameter | Metaverse Market Scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Metaverse Market Segmentation

By Product

- Hardware & Infrastructure

- Software

- Services

By Platform

- Desktop

- Mobile

- Headsets

- Consoles

By Application

- Gaming

- Online Shopping & E-commerce

- Content Creation & Social Media

- Virtual Events & Conferences

- Digital Marketing & Advertising

- Testing, Inspection & Simulation

- Education & Training

- Healthcare Applications

- Real Estate & Virtual Workspaces

- Others

By End Use

- Aerospace & Defense

- Education

- Tourism & Hospitality

- BFSI

- Retail

- Media & Entertainment

- Automotive

- Healthcare

- Telecom & IT

- Manufacturing & Industrial

- Government & Public Sector

- Others

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

Meta Platforms, Microsoft, NVIDIA, Roblox Corporation, Unity Technologies, Epic Games, Tencent, Sony Group, Apple, HTC Corporation, Niantic, Amazon Web Services, Autodesk, Decentraland, Magic Leap

Recent Industry Developments

- July 2025 – Hitachi develops metaverse platform for nuclear power plants: Hitachi created a virtual environment that reconstructs nuclear facilities using point-cloud and 3D CAD data, enabling enhanced safety planning, maintenance scheduling, and decommissioning support.

- April 2025 – Futureverse acquires Candy Digital: Futureverse completed the acquisition of NFT startup Candy Digital to integrate its digital collectibles into the Root Network, expanding fan engagement opportunities in its metaverse offerings.

- May 2025 – Meta’s Reality Labs reports heavy quarterly losses: Meta’s Reality Labs division reported a $4.2 billion quarterly loss while maintaining its focus on scaling metaverse platforms, hardware development, and immersive content creation.

- December 2024 – Meta releases Meta Motivo AI model: Meta launched the Meta Motivo AI model to enhance realism in digital avatars and NPCs, introducing advanced motion animation features and conceptual reasoning capabilities.

What You Receive

• Global Metaverse market size and growth projections (CAGR), 2024- 2034

• Impact of recent changes in geopolitical, economic, and trade policies on the demand and supply chain of Metaverse.

• Metaverse market size, share, and outlook across 5 regions and 27 countries, 2025- 2034.

• Metaverse market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2025- 2034.

• Short and long-term Metaverse market trends, drivers, restraints, and opportunities.

• Porter’s Five Forces analysis, Technological developments in the Metaverse market, Metaverse supply chain analysis.

• Metaverse trade analysis, Metaverse market price analysis, Metaverse Value Chain Analysis.

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products.

• Latest Metaverse market news and developments.

The Metaverse Market international scenario is well established in the report with separate chapters on North America Metaverse Market, Europe Metaverse Market, Asia-Pacific Metaverse Market, Middle East and Africa Metaverse Market, and South and Central America Metaverse Markets. These sections further fragment the regional Metaverse market by type, application, end-user, and country.

FAQ's

The Global Metaverse Market is estimated to generate USD 152.22 billion in revenue in 2025.

The Global Metaverse Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 33.9% during the forecast period from 2025 to 2034.

The Metaverse Market is estimated to reach USD 2106 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!