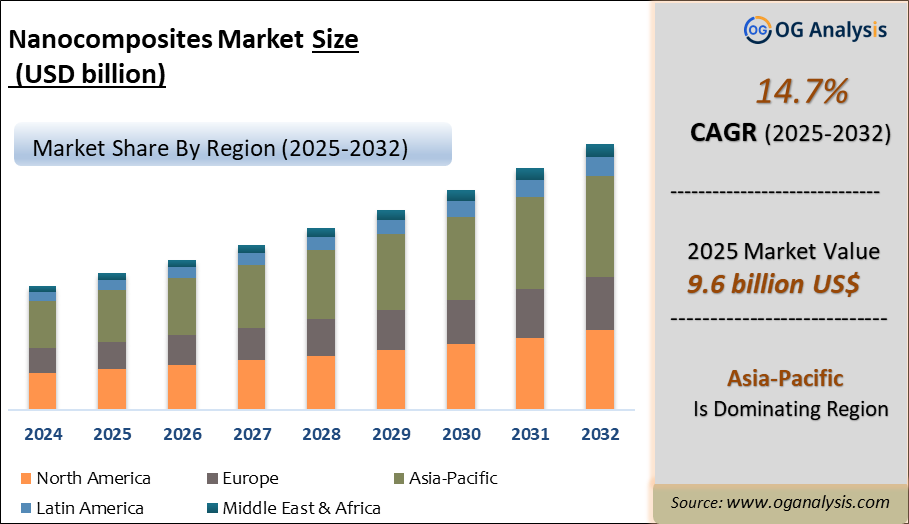

"The Global Nanocomposites Market Size was valued at USD 8.5 billion in 2024 and is projected to reach USD 9.6 billion in 2025. Worldwide sales of Nanocomposites are expected to grow at a significant CAGR of 14.7%, reaching USD 34.0 billion by the end of the forecast period in 2034."

Introduction and Overview

The nanocomposites market represents a dynamic and rapidly evolving sector within materials science. These advanced materials are composed of a matrix embedded with nanoparticles, which enhance their mechanical, thermal, and electrical properties compared to conventional composites. The market has seen significant growth driven by the increasing demand for high-performance materials across various industries, including automotive, aerospace, electronics, and healthcare. Innovations in nanotechnology have enabled the development of nanocomposites with tailored properties, making them highly desirable for applications requiring superior performance and efficiency. As industries continue to seek lightweight, durable, and multifunctional materials, nanocomposites are positioned to play a crucial role in meeting these demands.

In recent years, the nanocomposites market has been characterized by a surge in research and development activities, aimed at expanding the applications and improving the performance of these materials. The market is influenced by the growing emphasis on sustainability and environmental impact, leading to the development of eco-friendly nanocomposites. The integration of nanocomposites into various manufacturing processes has led to significant advancements in product quality and performance. Furthermore, the increasing adoption of nanocomposites in emerging technologies, such as renewable energy and smart materials, is driving market growth. Overall, the nanocomposites market is poised for substantial expansion, supported by technological advancements and the expanding scope of applications.

Trade Intelligence for nanocomposites market

| Global Non-cellular polyethylene plates, sheets, film, foil and strip (unworked, not reinforced or backed) Trade, Imports, USD million, 2020-24 | |||||

|

| 2020 | 2021 | 2022 | 2023 | 2024 |

| World | 15,733 | 19,730 | 21,105 | 18,778 | 19,022 |

| United States of America | 1,705 | 2,173 | 2,444 | 2,168 | 2,356 |

| Germany | 940 | 1,279 | 1,373 | 1,137 | 1,142 |

| France | 793 | 1,058 | 1,182 | 994 | 987 |

| Mexico | 585 | 698 | 767 | 697 | 766 |

| United Kingdom | 549 | 566 | 778 | 735 | 748 |

| Source: OGAnalysis, International Trade Centre (ITC) | |||||

- United States of America, Germany, France, Mexico and United Kingdom are the top five countries importing 31.5% of global Non-cellular polyethylene plates, sheets, film, foil and strip (unworked, not reinforced or backed) in 2024

- Global Non-cellular polyethylene plates, sheets, film, foil and strip (unworked, not reinforced or backed) Imports increased by 20.9% between 2020 and 2024

- United States of America accounts for 12.4% of global Non-cellular polyethylene plates, sheets, film, foil and strip (unworked, not reinforced or backed) trade in 2024

- Germany accounts for 6% of global Non-cellular polyethylene plates, sheets, film, foil and strip (unworked, not reinforced or backed) trade in 2024

- France accounts for 5.2% of global Non-cellular polyethylene plates, sheets, film, foil and strip (unworked, not reinforced or backed) trade in 2024

| Global Non-cellular polyethylene plates, sheets, film, foil and strip (unworked, not reinforced or backed) Export Prices, USD/Ton, 2020-24 |

|

|

| Source: OGAnalysis |

Latest Trends

One of the most notable trends in the nanocomposites market is the rise of sustainable and eco-friendly materials. As industries and consumers become more environmentally conscious, there is a growing demand for nanocomposites that minimize environmental impact. Researchers are focusing on developing nanocomposites from renewable resources and improving their recyclability. For instance, bio-based nanocomposites are gaining traction due to their potential to reduce the reliance on fossil fuels and lower carbon emissions. This trend reflects a broader shift towards sustainability in materials science, aligning with global environmental goals and regulations.

Another key trend is the increasing integration of nanocomposites into electronics and smart technologies. The advancement of nanotechnology has led to the development of nanocomposites with exceptional electrical and thermal conductivity, making them ideal for applications in electronic devices, sensors, and energy storage systems. This includes the use of nanocomposites in flexible electronics and advanced battery technologies, which are pivotal for the growth of wearable electronics and electric vehicles. The continuous innovation in this area is driving the market forward and opening up new opportunities for nanocomposites in high-tech applications.

The expansion of nanocomposites in the healthcare sector is also a significant trend. Nanocomposites are being utilized in various medical applications, including drug delivery systems, tissue engineering, and diagnostic tools. Their unique properties, such as enhanced biocompatibility and targeted delivery capabilities, are making them increasingly valuable in improving patient outcomes and advancing medical technologies. This trend is supported by ongoing research and clinical trials demonstrating the potential of nanocomposites to revolutionize healthcare practices. As the demand for advanced medical solutions grows, the adoption of nanocomposites in this sector is expected to rise accordingly.

Drivers

The primary driver of the nanocomposites market is the demand for high-performance materials with enhanced properties. Nanocomposites offer superior mechanical strength, thermal stability, and electrical conductivity compared to traditional composites, making them highly sought after in various industries. The automotive and aerospace sectors, in particular, are leveraging these advanced materials to achieve lighter, stronger, and more efficient components, which contribute to improved fuel efficiency and overall performance. As these industries continue to push for technological advancements, the demand for nanocomposites is expected to grow accordingly.

Technological advancements in nanotechnology are another major driver of the market. The continuous development of new nanomaterials and manufacturing techniques has expanded the potential applications of nanocomposites. Innovations such as improved synthesis methods and the ability to tailor nanocomposite properties to specific needs are driving market growth. Additionally, advancements in characterization techniques allow for better understanding and optimization of nanocomposites, further enhancing their performance and applicability. These technological advancements are crucial in meeting the evolving demands of various industries and fostering market expansion.

The growing emphasis on sustainability and environmental impact is also driving the nanocomposites market. Industries are increasingly seeking materials that offer environmental benefits, such as reduced carbon footprint and improved recyclability. Nanocomposites that are derived from renewable resources or contribute to energy efficiency are gaining traction. For example, nanocomposites used in energy storage and conversion technologies can enhance the efficiency of renewable energy systems. As regulatory pressures and consumer preferences shift towards more sustainable solutions, the demand for eco-friendly nanocomposites is expected to rise, driving market growth.

Market Challenges

Despite its growth prospects, the nanocomposites market faces several challenges. One of the primary challenges is the high cost of production. The manufacturing processes involved in producing nanocomposites can be complex and expensive, which can limit their accessibility and adoption in some industries. Additionally, there are concerns regarding the scalability of nanocomposite production, as transitioning from laboratory-scale to industrial-scale production can be challenging. Moreover, regulatory and safety issues related to the use of nanomaterials pose significant hurdles. Ensuring the safe handling, use, and disposal of nanocomposites is crucial to address potential health and environmental risks. Overcoming these challenges is essential for the continued growth and widespread adoption of nanocomposites across various sectors.

Market Players

1. Sigma-Aldrich Co. LLC.

2. InMat Inc.

3. Inframat Corporation

4. Hybrid Plastics Inc.

5. Nanocor Incorporated

6. Foster Corporation

7. BYK-Gardner GmbH

8. Industrial Nanotech, Inc.

Report Scope

| Parameter | nanocomposites market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD Billion |

| Market Splits Covered | By Type, By Dimension, By Application |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

- By Type

- Clay-based Nanocomposites

- Carbon Nanotube

- Metal Oxide

- Nanofiber

- Graphene

- Others

- By Dimension

- 01-10 nm

- 11-20 nm

- 21-30 nm

- 31-40 nm

- 41-50 nm

- By Application

- Building and Construction

- Electronics and Semiconductor

- Automotive

- Aviation

- Medical and Healthcare

- Plastics and Packaging

- Energy

- Military and Defense

- Others (such as consumer goods)

- By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Recent Developments

- Toray Industries introduced a new nanocomposite combining carbon fiber with nano-silica to enhance durability for next-generation aircraft components.

- DuPont launched a series of nanocomposite polymers designed for lightweighting in electric vehicles and aerospace applications.

- Mitsubishi Chemical developed advanced nanocomposite packaging films aimed at extending shelf life for food and pharmaceutical products.

- MCAP completed the acquisition of J-Film from Mitsubishi Chemical to expand its portfolio in advanced plastic and barrier film nanocomposites.

- BASF unveiled a new nanoclay-based polymer composite targeting improved flame resistance and thermal stability for electronics housings.

- LG Chem introduced graphene-reinforced nanocomposites to improve mechanical strength and conductivity for energy storage systems.

- Arkema announced the commercialization of bio-based nanocomposites for use in sustainable automotive interior parts.

FAQ's

The Global Nanocomposites Market is estimated to generate USD 8.5 billion in revenue in 2024.

The Global Nanocomposites Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 14.7% during the forecast period from 2025 to 2032.

The Nanocomposites Market is estimated to reach USD 25.5 billion by 2032.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!