"The Oleander Extract Market was valued at $203.4 million in 2025 and is projected to reach $411.4 million by 2034, growing at a CAGR of 9.2%."

Oleander extract, derived from the leaves and flowers of the Nerium oleander plant, is known for its strong bioactive compounds, primarily used in traditional medicine and increasingly explored in modern applications. Despite its natural toxicity, carefully processed oleander extract has shown potential in immune support, skin care, and anti-cancer research. It contains cardiac glycosides, which require precise formulation and regulation, making it more suitable for research-grade supplements and pharmaceutical innovations than general wellness products. Growing interest in plant-based therapeutic ingredients and natural compounds with potent biological activity is placing oleander extract into a specialized niche. Its usage is highly regulated, and its commercial growth is carefully managed to balance efficacy and safety concerns.

In 2024, the oleander extract market gained attention through increased investment in clinical studies examining its use in cancer treatment and immune modulation. While not widely adopted for mainstream use due to safety considerations, pharmaceutical and biotech firms showed growing interest in its active compounds for targeted therapies. Botanical research organizations worked on isolating specific glycosides from oleander to explore their mechanisms in controlled environments. There was also a rise in the use of oleander in high-end cosmeceuticals, where its antioxidant and anti-inflammatory properties were harnessed in diluted and safe topical formulations. This cautious but promising exploration signaled renewed scientific and commercial interest, albeit within tightly monitored and expert-led domains.

Looking ahead, the oleander extract market is likely to advance through pharmaceutical and biotech collaborations aimed at unlocking its therapeutic potential under strict safety and dosage frameworks. Expect more focus on refined extraction techniques that isolate beneficial compounds while minimizing toxicity. Regulatory bodies may outline clearer pathways for oleander-derived formulations, particularly in oncology and immune research. If scientific validation progresses, controlled applications in dermatology and immune health could expand, supported by targeted delivery methods like encapsulation. However, due to its potent chemical nature, oleander extract will likely remain a specialty botanical reserved for advanced formulations, making its growth reliant on innovation, compliance, and continued clinical evidence.

Key Insights

- Oleander extract has historically been associated with potent biological activity and a narrow safety margin, which continues to shape how the market is structured and regulated. Unlike many botanicals positioned for broad consumer use, oleander-derived products typically remain confined to controlled, professionally supervised environments. This legacy underscores the importance of pharmaceutical-grade standards and responsible communication.

- Source material and extraction control are critical, as variability in plant species, growing conditions, and processing can significantly influence the active compound profile. Manufacturers that can ensure consistent raw material sourcing, standardized extraction parameters, and rigorous analytical testing hold a competitive edge. These capabilities are essential for meeting the expectations of clinical researchers and regulatory authorities.

- Regulatory oversight is one of the most powerful determinants of market development, with agencies closely monitoring any products containing oleander-derived compounds. Approvals, restrictions, and guidance documents heavily influence what product formats are permissible, how they are labeled, and in which geographies they can be marketed. This environment favors players experienced in dossier preparation, risk assessment, and compliance.

- The primary demand base lies in pharmaceutical and clinical research applications, where oleander extract is investigated under controlled protocols rather than promoted for general wellness. Contract research organizations and academic partnerships play an outsized role in shaping future directions. Commercialization opportunities are closely tied to trial outcomes, safety data, and the ability to secure appropriate regulatory pathways.

- In personal care and cosmetics, oleander-derived components may appear in strictly formulated topical products, often in complex blends with other actives. Here, positioning emphasizes advanced science and targeted benefits, with brands carefully managing safety narratives and concentration levels. Such usage remains niche compared with more widely accepted botanical actives but offers differentiation in high-end segments.

- Growing global concern around toxic plant materials and self-medication has increased scrutiny on how oleander-related ingredients are marketed and distributed. Responsible participants in the market avoid unverified claims and focus on controlled, evidence-based uses. This trend limits opportunistic entrants and reinforces the importance of professional oversight and clear risk–benefit communication.

- Technological advances in extraction, purification, and analytical characterization support more precise control over specific oleander-derived constituents. These innovations enable the development of standardized fractions and potentially isolated compounds with defined potency profiles. Such refinement can improve the feasibility of structured clinical evaluation and targeted therapeutic development.

- Intellectual property and proprietary formulations represent important strategic assets, as companies seek to protect specialized extraction processes, compositions, and application methods. Patents, data exclusivity, and licensing agreements can help secure returns on high-risk R&D investments. This IP-centric approach aligns the oleander extract market more closely with pharmaceutical and biotech models than with generic botanical supply.

- From a risk management perspective, education and training for healthcare professionals, formulators, and regulatory reviewers remain crucial. Clear understanding of dose thresholds, contraindications, and interaction risks influences both product design and market acceptance. Companies that invest in robust safety files and professional engagement are better positioned to participate in long-term, ethically grounded market growth.

- Looking forward, the oleander extract market is likely to evolve slowly and cautiously, with growth contingent on credible scientific advances, well-designed clinical trials, and transparent regulatory processes. Opportunities will be concentrated in specialized therapeutic niches, tightly controlled product categories, and research collaborations, rather than broad consumer-facing expansion. This trajectory underscores the need for disciplined, science-first strategies in any oleander-related commercial activity.

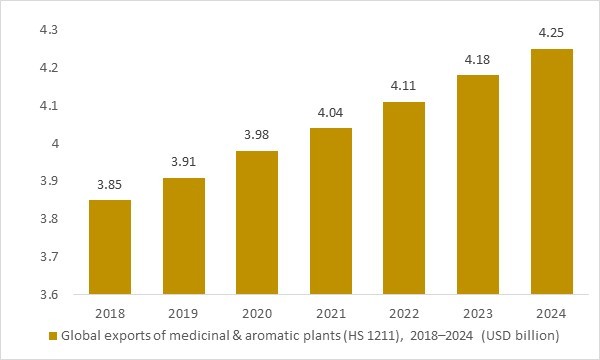

Global exports of medicinal & aromatic plants (HS 1211), 2018–2024 (USD billion)

Figure: Global exports of medicinal and aromatic plants (HS 1211) increased steadily between 2018 and 2024, reflecting the expansion of the traded medicinal-plant raw material base. As specialized botanical ingredients are increasingly used in high-value pharmaceutical, nutraceutical and security-related applications, this growing supply foundation underpins long-term opportunities in the oleander extract market. OG Analysis estimates, aligned with international trade statistics, illustrate how rising demand for medicinal plants supports the outlook for oleander-derived products.

- Global exports of medicinal and aromatic plants (HS 1211) increased steadily from 2018 to 2024, reflecting the expansion of the traded medicinal-plant raw material base. As toxic and pharmacologically active botanicals become more commercially significant in high-value pharmaceutical and security applications, this growing supply foundation supports long-term opportunities in the oleander extract market. OG Analysis estimates, aligned with international trade statistics, highlight how rising investment in advanced botanical ingredients underpins the future outlook for oleander-derived products.

Regional Insights

North America oleander extract market

In North America, the oleander extract market is shaped primarily by pharmaceutical and clinical research activity rather than by broad commercial supplement use. Strict regulatory scrutiny around toxicity and narrow safety margins means most demand is concentrated in pre-clinical and early-stage clinical programs handled through specialized research institutions and contract development organizations. Companies focus on highly standardized extracts or purified fractions produced under GMP conditions with extensive analytical characterization. Ethical and regulatory committees are increasingly cautious about high-risk botanicals, which pushes developers toward more robust toxicology, pharmacokinetic, and dose-escalation studies before any wider deployment. As a result, the market remains small but technically sophisticated, centered on long lead-time R&D partnerships and carefully controlled therapeutic concepts.

Europe oleander extract market

In Europe, the oleander extract market is constrained by precautionary regulatory frameworks and strong pharmacovigilance cultures. Oleander and its derivatives are typically handled within strictly defined medicinal, investigational, or homeopathic contexts, with limited scope for over-the-counter or wellness positioning. Regulatory agencies and scientific committees emphasize comprehensive safety assessments, standardization, and clear benefit–risk justification, which narrows the field to a few specialized players. Cosmetic and personal care use, where present, tends to be in highly controlled, low-level topical applications with careful labelling and documentation. Academic–industrial collaborations and EU-funded research projects occasionally explore novel applications, but commercial roll-out remains conservative and evidence-driven.

Asia-Pacific oleander extract market

In Asia-Pacific, the oleander extract market intersects with deep traditions of herbal medicine and plant-based remedies, yet modern regulators increasingly distinguish between traditional use and high-potency, standardized extracts. Some markets show interest in oleander-derived actives within integrative oncology or cardiology research frameworks, but authorities generally insist on rigorous scientific validation and controlled clinical protocols. A growing base of botanical extract manufacturers and contract research organizations provides technical capabilities for advanced extraction, purification, and analytical testing. At the same time, public health campaigns warning against unsafe self-medication with toxic plants encourage tighter channel control and professional supervision. This combination of historical familiarity and modern safety requirements creates a cautious but active environment for research-oriented oleander applications.

Report Scope

| Parameter | Oleander extract Market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Oleander Extract Market Segmentation

By Product

- Liquid Extract

- Powder Extract

By Application

- Pharmaceuticals

- Cosmetics

- Food & Beverages

By End User

- Healthcare

- Personal Care

- Food Industry

By Technology

- Cold Press Extraction

- Hot Water Extraction

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Companies Covered

- Alchem International

- Herb Pharm

- Organic Herb Inc

- Nutra Green Biotechnology Co

- Bioprex Labs

- Nature’s Answer

- Mountain Rose Herbs

- Xi’an Greena Biotech Co

- Star Hi Herbs

- Himalaya Herbal Healthcare

- Indena SpA

- Sabinsa Corporation

- Glanbia Nutritionals

- Botanica BioScience Corp

- Naturalin Bio-Resources Co Ltd

Recent Industry Developments

-

Nov 2025 – SiluetaYa: Issued a recall for its “Tejocote Root” dietary supplement after product testing indicated it was yellow oleander rather than the labeled ingredient. The action reinforced heightened industry scrutiny around botanical identity testing and supply-chain controls.

-

Nov 2025 – Multiple supplement sellers/distributors: Several brands and distributors initiated market withdrawals/recalls of “Tejocote root” and similar products following findings of oleander-related adulteration. The wave of actions triggered tighter retailer gating and greater demand for third-party authentication (DNA/chemical fingerprinting).

-

Oct 2024 – Phoenix Biotechnology: Reported new research outputs around standardized oleander extract / oleandrin and immune-modulation activity under inflamed conditions, supporting continued positioning of controlled, pharmaceutical-grade extracts versus consumer-supplement use.

-

2024–2025 – Botanical extract manufacturers (industry-wide): Increased emphasis on standardization, controlled extraction methods (e.g., supercritical CO₂), and tighter QC specifications for oleander-derived actives. The shift is driven by safety sensitivities and the need to demonstrate batch-to-batch consistency for regulated applications.

What You Receive

• Global Oleander Extract market size and growth projections (CAGR), 2024- 2034

• Impact of recent changes in geopolitical, economic, and trade policies on the demand and supply chain of Oleander Extract.

• Oleander Extract market size, share, and outlook across 5 regions and 27 countries, 2025- 2034.

• Oleander Extract market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2025- 2034.

• Short and long-term Oleander Extract market trends, drivers, restraints, and opportunities.

• Porter’s Five Forces analysis, Technological developments in the Oleander Extract market, Oleander Extract supply chain analysis.

• Oleander Extract trade analysis, Oleander Extract market price analysis, Oleander Extract Value Chain Analysis.

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products.

• Latest Oleander Extract market news and developments.

The Oleander Extract Market international scenario is well established in the report with separate chapters on North America Oleander Extract Market, Europe Oleander Extract Market, Asia-Pacific Oleander Extract Market, Middle East and Africa Oleander Extract Market, and South and Central America Oleander Extract Markets. These sections further fragment the regional Oleander Extract market by type, application, end-user, and country.

Who can benefit from this research

The research would help top management/strategy formulators/business/product development/sales managers and investors in this market in the following ways

1. The report provides 2024 Oleander Extract market sales data at the global, regional, and key country levels with a detailed outlook to 2034, allowing companies to calculate their market share and analyze prospects, uncover new markets, and plan market entry strategy.

2. The research includes the Oleander Extract market split into different types and applications. This segmentation helps managers plan their products and budgets based on the future growth rates of each segment

3. The Oleander Extract market study helps stakeholders understand the breadth and stance of the market giving them information on key drivers, restraints, challenges, and growth opportunities of the market and mitigating risks

4. This report would help top management understand competition better with a detailed SWOT analysis and key strategies of their competitors, and plan their position in the business

5. The study assists investors in analyzing Oleander Extract business prospects by region, key countries, and top companies' information to channel their investments.

Available Customizations

The standard syndicate report is designed to serve the common interests of Oleander Extract Market players across the value chain and include selective data and analysis from entire research findings as per the scope and price of the publication.

However, to precisely match the specific research requirements of individual clients, we offer several customization options to include the data and analysis of interest in the final deliverable.

Some of the customization requests are as mentioned below :

Segmentation of choice – Our clients can seek customization to modify/add a market division for types/applications/end-uses/processes of their choice.

Oleander Extract Pricing and Margins Across the Supply Chain, Oleander Extract Price Analysis / International Trade Data / Import-Export Analysis

Supply Chain Analysis, Supply–Demand Gap Analysis, PESTLE Analysis, Macro-Economic Analysis, and other Oleander Extract market analytics

Processing and manufacturing requirements, Patent Analysis, Technology Trends, and Product Innovations

Further, the client can seek customization to break down geographies as per their requirements for specific countries/country groups such as South East Asia, Central Asia, Emerging and Developing Asia, Western Europe, Eastern Europe, Benelux, Emerging and Developing Europe, Nordic countries, North Africa, Sub-Saharan Africa, Caribbean, The Middle East and North Africa (MENA), Gulf Cooperation Council (GCC) or any other.

Capital Requirements, Income Projections, Profit Forecasts, and other parameters to prepare a detailed project report to present to Banks/Investment Agencies.

Customization of up to 10% of the content can be done without any additional charges.

Note: Latest developments will be updated in the report and delivered within 2 to 3 working days.

FAQ's

The Global Oleander Extract Market is estimated to generate USD 203.4 million in revenue in 2025.

The Global Oleander Extract Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 9.2% during the forecast period from 2025 to 2034.

The Oleander Extract Market is estimated to reach USD 411.4 million by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!