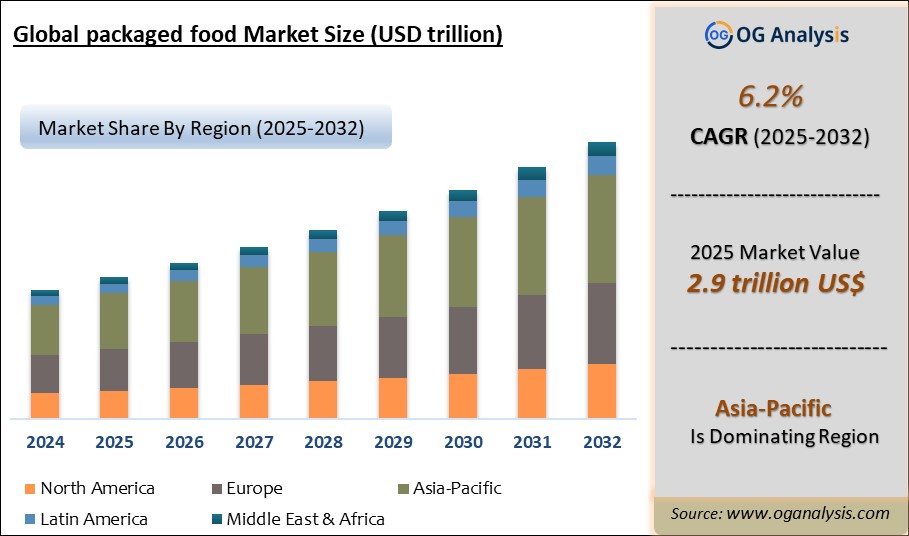

"Global Packaged Food Market is valued at USD 2.9 trillion in 2025. Further, the market is expected to grow at a CAGR of 6.2% to reach USD 4.9 trillion by 2034."

The Packaged Food Market has grown rapidly in recent years, driven by shifting consumer lifestyles, urbanization, and a heightened demand for convenience. Packaged foods—ranging from snacks and ready-to-eat meals to dairy, bakery, frozen, and canned products—offer long shelf life, portability, and consistent quality. The expansion of retail infrastructure, the rise of e-commerce, and busy work schedules have encouraged more consumers to choose packaged options for both everyday meals and on-the-go consumption. Innovation in packaging technology, ingredient transparency, and product safety standards has made packaged foods more appealing and accessible across diverse demographics. Manufacturers are responding to evolving health and sustainability concerns by launching products with clean labels, organic certifications, and eco-friendly packaging.

The global packaged food industry is characterized by intense competition, frequent product launches, and strategic collaborations among major brands and regional players. As consumer preferences evolve, companies are investing in research and development to enhance taste, nutrition, and convenience while minimizing preservatives and additives. Growth opportunities abound in emerging markets where rising incomes and Western eating habits are influencing purchasing decisions. However, the sector faces challenges such as regulatory compliance, fluctuating input costs, and supply chain disruptions. The ongoing shift toward plant-based, fortified, and functional foods is expected to reshape the market landscape, with digital engagement and direct-to-consumer models gaining importance for future growth.

Ready meals are the fastest-growing segment in the packaged food market, propelled by consumers’ increasing demand for convenience, time-saving solutions, and urban lifestyles. The appeal of quick preparation, a wide variety of cuisines, and enhanced product quality is driving rapid adoption among both young professionals and busy families in developed and emerging markets.

Glass is the largest segment by material in the fortified wine market because it preserves the flavor and quality of wine, offers a premium image, and ensures chemical inertness and long shelf life. Glass bottles remain the preferred packaging choice for fortified wine producers and consumers alike, supporting its dominant market share.

Packaged Food Market- Key Insights

-

Convenience remains the primary driver for packaged food demand, as consumers seek time-saving meal solutions that require minimal preparation, leading to steady growth in ready-to-eat, frozen, and snack product segments across global markets.

-

Health and wellness trends are encouraging manufacturers to offer fortified, low-sugar, low-sodium, and organic packaged foods, responding to a rising consumer focus on nutrition, ingredient transparency, and clean-label claims.

-

The expansion of online grocery platforms and digital retail channels has significantly increased the accessibility and reach of packaged food brands, allowing companies to engage consumers directly and tailor offerings based on purchase behavior and feedback.

-

Innovative packaging technologies—such as resealable, portion-controlled, and biodegradable materials—are enhancing food safety, freshness, and environmental sustainability, attracting environmentally conscious buyers.

-

Emerging markets in Asia-Pacific, Latin America, and Africa are witnessing rapid growth in packaged food sales, driven by urbanization, rising disposable incomes, and increased exposure to Western diets and convenience foods.

-

The plant-based and vegan packaged food segment is growing at a remarkable pace, fueled by shifting dietary preferences, ethical concerns, and expanding product choices that cater to flexitarian and vegetarian consumers.

-

Fluctuating raw material prices and supply chain disruptions—exacerbated by global events and geopolitical tensions—pose challenges for packaged food manufacturers in terms of pricing, sourcing, and maintaining consistent quality.

-

Strategic partnerships, acquisitions, and collaborations among global and regional players are reshaping the competitive landscape, enabling companies to diversify product portfolios and expand into new markets more efficiently.

-

Regulatory compliance regarding food safety, labeling, and additive usage is becoming more stringent, requiring ongoing investments in quality control and transparency to meet evolving standards across different countries.

-

Personalization and direct-to-consumer models are gaining traction, with brands leveraging digital platforms to offer customized nutrition, subscription boxes, and interactive marketing, strengthening brand loyalty and consumer engagement.

Report Scope

| Parameter | Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Type, By Material, By Packaging and By Sales |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Type

- Dairy Products

- Confectionery

- Packaged Products

- Bakery And Snack

- Meat

- Poultry And Seafood

- Ready Meals

- Other Types

By Material

- Glass

- Metal

- Paper

- Plastics

- Other Materials

By Packaging

- Jugs

- Packets

- Bottles

- Bags

- Bowls

- Boxes

- Cans

- Cartons

- Crates

By Sales Channel

- Supermarkets Or Hypermarkets

- Specialty Stores

- Grocery Stores

- Online Stores

- Other Sales Channels

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- General Mills Inc.

- Tyson Foods Inc.

- Conagra Brands Inc.

- JBS SA

- Nestle SA

- Hormel Foods Corporation

- Maple Leaf Foods Inc.

- The Kraft Heinz Company

- Smithfield Foods Inc.

- Kellogg Company

- PepsiCo Inc.

- Mars Incorporated

- WH Group Limited

- The Hershey Company

- Andros Group

- Histon Sweets Spreads Ltd

- The Coca-Cola Company

- Danone SA

- Mondelz Global LLC

- Unilever plc

- Gehl Foods LLC

- B & G Foods Inc.

- Frito-Lay Inc.

- Mann Packing Co. Inc.

- Bonduelle Group

- The Keebler Company

- McCain Foods Limited

- Grupo Bimbo S.A.B. de C.V.

- Campbell Soup Company

- Nomad Foods Limited

- Monde Nissin Corporation .

Dominating segmentation

Last month, SES signed a multi-launch agreement with Impulse Space to deploy satellites using Impulse’s Helios kick stage, reducing transit time and cutting mission costs.

During the same period, SES highlighted its advance toward fully digital payload GEO satellites equipped for electric propulsion and in-orbit servicing.

Five months ago, MDA secured a US$1.1 billion contract with Globalstar to build over 50 AURORA software-defined LEO satellites, boosting next-gen constellation deployment.

Additionally five months ago, K2 Space closed a US$110 million Series B round to support mass production of its multi-orbit, high-power satellite platforms after a successful in-space demo.

Last month, China’s LandSpace successfully launched the methane-powered Zhuque-2E Y2 rocket, placing multiple satellites into orbit and progressing reusable, clean-propulsion technology.

These announcements reflect major strides in propulsion innovation, constellation scaling, launch efficiency, and satellite manufacturing capabilities.

FAQ's

The Packaged Food Market is estimated to reach USD 4.9 trillion by 2034.

The Global Packaged Food Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% during the forecast period from 2025 to 2034.

The Global Packaged Food Market is estimated to generate USD 2.9 trillion in revenue in 2025.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!