"The Pandan Leaf Extract Market was valued at $ 529.5 million in 2025 and is projected to reach $ 886.1 million by 2034, growing at a CAGR of 6.65%."

Pandan leaf extract, derived from the leaves of the tropical plant *Pandanus amaryllifolius*, is gaining recognition beyond its traditional Southeast Asian culinary uses. Renowned for its naturally sweet, floral aroma and vibrant green hue, it is now finding applications in the food, beverage, personal care, and fragrance industries. As the clean-label movement grows, manufacturers seek natural flavors and functional ingredients, making pandan extract an appealing alternative to artificial colorants and flavor enhancers. Its antioxidant and antibacterial properties also broaden its utility in natural skincare, oral care, and wellness food formulations. With rising interest in botanical ingredients that offer sensory appeal along with perceived health benefits, pandan leaf extract is poised to become a mainstream functional ingredient in global markets.

In 2024, the pandan leaf extract market saw an uptick in product experimentation and positioning within premium food and personal care categories. Artisan beverage makers introduced pandan-infused teas, syrups, and sparkling wellness drinks, emphasizing its unique aroma and natural coloration. Similarly, functional food brands featured pandan in baked goods, dairy alternatives, and confectionery for its clean-label credentials. Within skincare and hygiene lines, pandan was used for its soothing and antimicrobial qualities, often combined with other botanical extracts in creams, serums, and deodorants. Extraction technologies became more eco-conscious, with more suppliers transitioning to cold-press or solvent-free methods to preserve bioactive profiles and support sustainability credentials. Market narratives shifted toward highlighting traceability, harvest origin, and harvest-season variations, appealing to informed consumers and regional product developers seeking authentic ingredient storytelling.

Looking forward, pandan leaf extract is expected to further diversify across categories and form factors. Novel delivery formats such as powder-sachets, encapsulated flavor beads, and dairy-free dessert kits are likely to emerge, driven by consumer demand for convenience and sensory experiences. As botanical extract blends grow in popularity, pandan may be paired with adaptogens or prebiotic fibers in functional snack and beverage launches. Continued investment in standardization and quality control will encourage its adoption in regulated markets such as Europe and North America. Sustainability initiatives—including water-efficient cultivation, smallholder farmer partnerships, and certified organic sourcing—will become more visible in supplier branding. Educational campaigns targeting Western consumers may emphasize both its culinary heritage and functional benefits, potentially pioneering pandan’s role in holistic wellness and multi-sensory product innovation by mid-decade.

Key Market Trends, Drivers and Challenges

- Rising demand for natural food additives is propelling the use of pandan leaf extract in bakery and beverage formulations, especially in Southeast Asian cuisines gaining global popularity.

- The cosmetic industry's shift towards herbal ingredients has boosted the use of pandan extract in skincare and aromatherapy products due to its antioxidant and aromatic profile.

- Clean label trends and transparency in sourcing are driving product development using sustainably harvested pandan leaves, appealing to conscious consumers globally.

- Health-conscious consumers increasingly prefer natural flavors and plant-based ingredients, fueling demand for pandan extract as a healthier substitute to synthetic additives.

- Expansion of food & beverage manufacturers into Asian-inspired products has encouraged the incorporation of pandan for its unique taste and green coloring capabilities.

- Increased research into the medicinal benefits of pandan—such as anti-inflammatory and anti-diabetic properties—is supporting its integration into nutraceuticals and health supplements.

- Seasonal supply constraints and inconsistent quality from small-scale pandan farms can hinder large-scale procurement for global manufacturers.

- Lack of standardized extraction methods and regulations across markets presents a barrier to consistent product quality and labeling compliance.

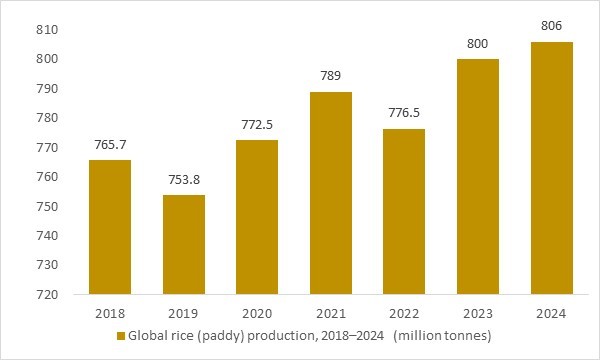

Global rice (paddy) production, 2018–2024(million tonnes)

Figure: Global rice production has remained robust, rising from around 766 million tonnes in 2018 to an estimated 806 million tonnes in 2024e, reflecting the steady resilience of rice-based food systems across Asia and other key consuming regions. This trend supports the continued use of pandan leaves as a natural flavour and aroma agent in traditional rice dishes, desserts, beverages and modern packaged foods. OG Analysis estimates, based on international rice production statistics, hi

Global rice production has remained consistently high, fluctuating between 754 and 806 million tonnes from 2018 to 2024, underscoring the stability of the core culinary ecosystem where pandan leaf is traditionally used. As rice-centric cuisines across Southeast Asia continue to expand through domestic consumption and global food exports, demand for natural flavorings like pandan leaf extract strengthens accordingly. The steady rise toward an estimated 806 million tonnes in 2024 reflects resilient agricultural systems that also support smallholder pandan cultivation. Overall, the sustained scale of global rice output provides a strong foundation for long-term growth in the pandan leaf extract market.

Report Scope

| Parameter | Pandan Leaf Extract Market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Pandan Leaf Extract Market Segmentation

By Product

- Liquid Extract

- Powder Extract

By Application

- Food and Beverages

- Cosmetics

- Pharmaceuticals

By End User

- Food Industry

- Personal Care Industry

- Healthcare Sector

By Technology

- Cold Extraction

- Hot Extraction

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Companies Analysed

- NATUREX

- Herbo Nutra

- Xi’an Sost Biotech Co., Ltd.

- Indena SpA

- Sabinsa Corporation

- Ambe Phytoextracts Pvt. Ltd.

- Bio Botanica Inc.

- Organic Herb Inc.

- Xi'an Greena Biotech Co., Ltd.

- Phyto Life Sciences

- Guangdong Guangye Yun Tian Industrial Investment Co., Ltd.

- Swanson Health Products

- Green Herb Bio-Technology Ltd.

- Jiaherb Inc.

- Shanxi Jinjin Chemical Co., Ltd.

Available Customizations

The standard syndicate report is designed to serve the common interests of Pandan Leaf Extract Market players across the value chain and include selective data and analysis from entire research findings as per the scope and price of the publication.

However, to precisely match the specific research requirements of individual clients, we offer several customization options to include the data and analysis of interest in the final deliverable.

Some of the customization requests are as mentioned below :

Segmentation of choice – Our clients can seek customization to modify/add a market division for types/applications/end-uses/processes of their choice.

Pandan Leaf Extract Pricing and Margins Across the Supply Chain, Pandan Leaf Extract Price Analysis / International Trade Data / Import-Export Analysis

Supply Chain Analysis, Supply–Demand Gap Analysis, PESTLE Analysis, Macro-Economic Analysis, and other Pandan Leaf Extract market analytics

Processing and manufacturing requirements, Patent Analysis, Technology Trends, and Product Innovations

Further, the client can seek customization to break down geographies as per their requirements for specific countries/country groups such as South East Asia, Central Asia, Emerging and Developing Asia, Western Europe, Eastern Europe, Benelux, Emerging and Developing Europe, Nordic countries, North Africa, Sub-Saharan Africa, Caribbean, The Middle East and North Africa (MENA), Gulf Cooperation Council (GCC) or any other.

Capital Requirements, Income Projections, Profit Forecasts, and other parameters to prepare a detailed project report to present to Banks/Investment Agencies.

Customization of up to 10% of the content can be done without any additional charges.

Note: Latest developments will be updated in the report and delivered within 2 to 3 working days.

FAQ's

The Global Pandan Leaf Extract Market is estimated to generate USD 529.5 million in revenue in 2025.

The Global Pandan Leaf Extract Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 6.65% during the forecast period from 2025 to 2034.

The Pandan Leaf Extract Market is estimated to reach USD 886.1 million by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!