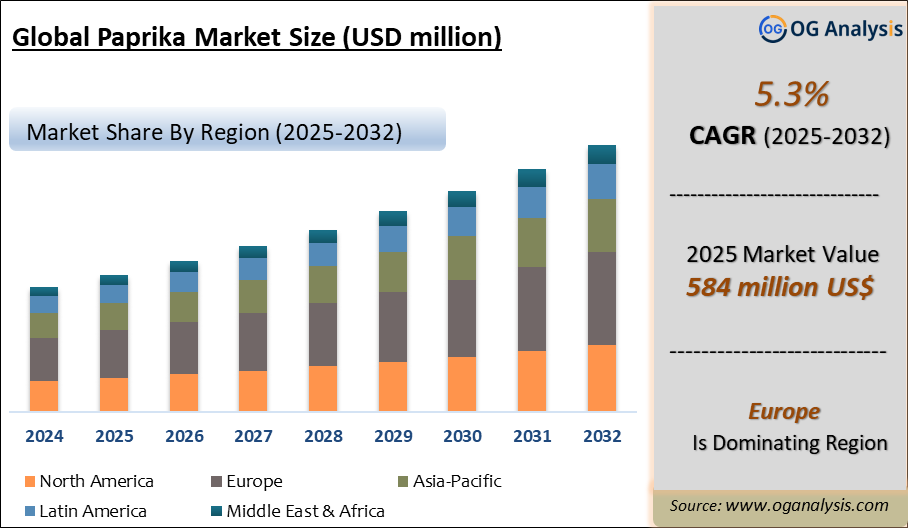

"The Paprika Market Size was valued at $ 615 million in 2026. Worldwide sales of Paprika are expected to grow at a significant CAGR of 5.3%, reaching $ 942 million by the end of the forecast period in 2034."

The Paprika Market is a well-established segment of the spices, seasonings, natural colorants, and food ingredients industry, driven by its broad use in food processing, culinary applications, flavor blends, meat products, snacks, sauces, ready meals, bakery products, soups, marinades, and ethnic food preparations. Paprika, derived from dried and ground capsicum peppers, is valued for its mild to pungent flavor profile, bright red color, aroma, and versatility across both household and industrial food applications. Demand is supported by the growth of packaged foods, spice mixes, clean-label seasonings, natural food coloring, premium culinary products, and expanding consumer interest in global cuisines. Food manufacturers use paprika to improve visual appeal, flavor depth, and product differentiation, while foodservice operators and retail consumers use it in traditional and fusion recipes. The market also benefits from rising preference for natural ingredients over synthetic colors, especially in processed meats, sauces, snacks, dairy products, and convenience foods.

The market is evolving as producers focus on quality consistency, oleoresin extraction, organic paprika, smoked paprika, high-color-value varieties, traceability, and food safety compliance. Key trends include increasing demand for natural colorants, growth in ethnic and gourmet seasoning products, rising use of paprika oleoresin in industrial food applications, and premiumization of spice categories through origin-specific and specialty variants. Demand drivers include growth in processed food consumption, expansion of quick-service restaurants, rising popularity of Mediterranean, Mexican, Spanish, Indian, and Middle Eastern cuisines, and increasing use of paprika in plant-based foods for color and flavor enhancement. However, climate sensitivity, crop quality variation, adulteration risks, pesticide residue concerns, price volatility, and supply concentration in key producing regions remain challenges. The competitive landscape includes spice processors, ingredient suppliers, paprika oleoresin manufacturers, seasoning companies, exporters, and private-label spice brands. Companies compete through quality grading, color strength, purity, origin traceability, certifications, customized blends, and supply reliability.

Regional Analysis

North America Paprika Market

The North America Paprika Market is driven by strong demand from processed foods, snacks, sauces, seasonings, meat products, ready meals, foodservice, and ethnic cuisine applications. Market dynamics are shaped by rising preference for natural colors, clean-label ingredients, premium spice blends, and globally inspired flavors across retail and industrial food channels. Lucrative opportunities exist for suppliers offering high-color paprika, paprika oleoresin, organic paprika, smoked paprika, and customized seasoning blends for snacks, marinades, plant-based foods, and convenience meals. Latest trends include wider use of paprika in reduced-artificial-color formulations, premium barbecue and Mexican-style seasonings, and plant-based meat alternatives. The forecast outlook remains positive as food manufacturers continue replacing synthetic colors and expanding savory flavor portfolios. Recent developments are centered on traceable sourcing, residue-controlled spice programs, food safety testing, private-label spice expansion, and growing use of paprika oleoresin in packaged food formulations.

Asia Pacific Paprika Market

The Asia Pacific Paprika Market is expanding with growth in food processing, seasoning blends, snacks, instant foods, sauces, quick-service restaurants, and spice-based culinary applications. Market dynamics are influenced by rising consumption of packaged foods, growing demand for natural food colors, expanding middle-class food preferences, and the region’s strong base of spice processing and ingredient manufacturing. Lucrative opportunities are emerging in paprika oleoresin, savory snacks, instant noodles, ready-to-cook meals, processed meats, bakery seasonings, and foodservice spice blends. Latest trends include use of paprika for color enhancement in snacks and sauces, demand for cost-effective natural colorants, and wider adoption of customized seasoning systems. The forecast outlook is strong as food manufacturers increase clean-label reformulation and expand flavor innovation. Recent developments include improved extraction capacity, stronger quality testing, export-oriented spice processing, and rising demand for certified paprika ingredients.

Europe Paprika Market

The Europe Paprika Market is shaped by mature culinary traditions, strong demand for natural ingredients, strict food safety expectations, and widespread use across processed meats, sauces, soups, snacks, ready meals, ethnic foods, and gourmet spice products. Market dynamics are supported by consumer preference for clean-label products, organic spices, smoked paprika, origin-specific varieties, and natural colorants. Lucrative opportunities exist for suppliers offering high-purity paprika, paprika oleoresin, organic grades, Spanish-style smoked paprika, Hungarian-style varieties, and residue-controlled products for industrial and retail buyers. Latest trends include premiumization of spices, reformulation away from synthetic additives, growing use in plant-based foods, and demand for verified traceability. The forecast outlook remains stable and quality-driven as buyers prioritize purity, authenticity, regulatory compliance, and consistent color strength. Recent developments are focused on food safety controls, sustainable sourcing, improved spice authentication, and expanded use of paprika oleoresin in clean-label processed foods.

Middle East & Africa Paprika Market

The Middle East & Africa Paprika Market is developing with demand from spice blends, sauces, marinades, meat products, snacks, foodservice, ready meals, and traditional culinary applications. Market dynamics are supported by growth in food processing, hospitality, quick-service restaurants, urban retail, and rising consumer interest in flavorful, colorful, and natural seasonings. Lucrative opportunities exist for paprika suppliers serving processed meat manufacturers, seasoning blenders, snack producers, restaurant chains, and packaged food companies. Latest trends include use of paprika in spice mixes, grilled meat seasonings, sauces, instant foods, and natural color applications for processed products. The forecast outlook is positive as regional food manufacturing expands and consumers shift toward packaged, convenient, and globally influenced foods. Recent developments include growth in spice blending facilities, rising imports of high-quality paprika, improved food ingredient distribution, and stronger demand for cost-effective natural colorants.

South & Central America Paprika Market

The South & Central America Paprika Market is supported by demand from sauces, seasonings, snacks, meat processing, ready meals, foodservice, retail spices, and natural colorant applications. Market dynamics are influenced by strong culinary use of peppers, growing packaged food consumption, expansion of seasoning manufacturers, and increasing preference for natural ingredients in processed foods. Lucrative opportunities are present in paprika oleoresin, savory snacks, barbecue seasonings, marinades, processed meats, plant-based foods, and export-oriented spice products. Latest trends include wider adoption of paprika for red-orange color enhancement, growth of premium and smoked spice variants, and increased use in regional and international food formulations. The forecast outlook is moderately positive as food manufacturers focus on taste differentiation, visual appeal, and cleaner ingredient labels. Recent developments include improved spice processing, stronger quality assurance practices, and rising demand from packaged food and foodservice channels.

Key Insights

- Natural colorant demand is a major growth driver for the Paprika Market, as food manufacturers seek alternatives to synthetic colors. Paprika and paprika oleoresin are widely used to deliver red-orange hues in snacks, sauces, processed meats, dressings, and ready meals.

- Processed food applications remain highly important because paprika supports both flavor and visual appeal. Seasonings, spice mixes, soups, marinades, instant foods, frozen meals, and savory snacks continue to create stable demand from industrial food manufacturers.

- Paprika oleoresin is gaining stronger relevance in large-scale food production due to its concentrated color, easier dosing, better consistency, and compatibility with automated processing. It is especially preferred where uniform color performance is required.

- Organic and clean-label paprika products are gaining traction among premium food brands and health-conscious consumers. Certified organic, non-GMO, residue-controlled, and minimally processed paprika grades are increasingly valued in retail and food manufacturing.

- Smoked paprika and specialty variants are benefiting from premiumization in culinary markets. Foodservice operators, gourmet brands, and home cooks are using these products to add depth, smoky character, and regional authenticity to recipes.

- Meat processing remains a significant end-use area, with paprika used in sausages, cured meats, marinades, seasoning coatings, and prepared meat products. Its color-enhancing and flavor-balancing properties make it important in traditional and modern formulations.

- Plant-based food development is creating new opportunities for paprika, particularly in meat alternatives, vegan sauces, ready meals, and savory snacks. Paprika helps improve product appearance while contributing mild heat, warmth, and natural flavor depth.

- Supply quality and traceability are critical market factors because paprika is vulnerable to color variation, contamination, adulteration, and pesticide residue concerns. Buyers increasingly prefer suppliers with strong testing systems and transparent sourcing practices.

- Climate and agricultural conditions influence paprika availability and quality, making crop management, irrigation, drying methods, and post-harvest handling important. Weather variability can affect color intensity, yield, flavor, and overall supply stability.

- Future market growth will be shaped by natural ingredient positioning, food safety assurance, high-color-value varieties, sustainable sourcing, and customized seasoning solutions. Suppliers with reliable quality, technical support, and certified supply chains are expected to remain competitive.

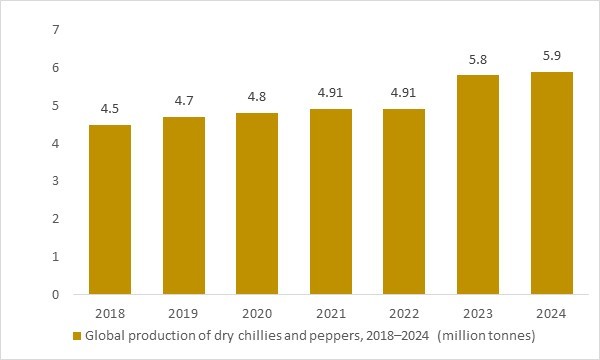

Global production of dry chillies and peppers, 2018–2024 (million tonnes)

Figure: Global production of dry chillies and peppers – the core Capsicum raw material for paprika – increased from an estimated 4.5 million tonnes in 2018 to almost 6 million tonnes by 2024. This expanding supply base underpins long-term growth in the paprika market, ensuring consistent availability of pods for powders, flakes and oleoresins used across snacks, meat products, sauces, ready meals and foodservice. OG Analysis estimates, aligned with FAO statistics and recent chilli production studies, highlight how rising Capsicum output supports demand for paprika ingredients worldwide.

Global production of dry chillies and peppers – the core raw material for paprika powders, flakes and oleoresins – expanded from an estimated 4.5 million tonnes in 2018 to almost 6 million tonnes by 2024. FAO-based statistics show world output of “chillies and peppers, dry” around 4.9 million tonnes in 2021–2022, while more recent research indicates production surged to roughly 5.8 million tonnes in 2023 as India and other Asian and African suppliers ramped up acreage and yields. This expanding supply base of dried Capsicum peppers underpins long-term growth in the paprika market, ensuring consistent availability of raw pods for colour and flavour extraction, stabilising input costs, and enabling paprika processors to serve rising demand from snack, meat, sauce, ready-meal and foodservice applications worldwide.

Report Scope

| Parameter | Paprika Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Product

- Vegetable

- Spice Powder

- Paprika Oleoresin

- Colorant paprika

- Others

By Form

- Powder

- Flakes

- Other Forms

By Application

- Food

- Pharmaceuticals

- Cosmetics

- Others

By Nature

- Organic

- Conventional

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Market Players

- Adani Pharmachem Private Limited

- Chr. Hansen

- EVESA

- Frutarom Industries Ltd

- Givaudan

- Ingredients Naturales Seleccionados

- Kalsec Natural Ingredients

- Kancor Ingredients Limited

- Naturex

- Ozone Naturals

- Plant Lipids

- Synthite Industries Ltd

- Ungerer & Company Unilever Food Solutions

- Unilever Food Solutions.

- Universal Oleoresi

Recent Industry Developments

April 2026 - The U.S. International Trade Commission scheduled the final phase of antidumping and countervailing duty investigations on oleoresin paprika from India, following preliminary affirmative determinations by the U.S. Department of Commerce.

February 2026 - Oterra launched its 2030 Sustainability Strategy, focusing on nature, climate, responsible sourcing, water stewardship, waste reduction, and farmer partnerships to strengthen natural color supply chains.

January 2026 - Döhler highlighted its natural color solutions portfolio, including amber-orange shades made using raw materials such as paprika, orange carrot, and carotene variants for food and beverage applications.

November 2025 - McCormick redesigned its Gourmet Collection of premium herbs and spices, rolling out refreshed packaging across its broad portfolio of distinctive and certified organic spice varieties.

October 2025 - Kalsec unveiled a refreshed corporate identity and “Discover What’s Naturally Possible” positioning, reinforcing its focus on natural food color, taste, sensory, and food protection solutions.

August 2025 - Oterra reported that naturally colored limited-time confectionery products can help brands create urgency, drive trial, and improve purchase appeal among consumers.

July 2025 - Oterra announced U.S. consumer research showing strong concern over artificial dyes and increased interest in natural colors sourced from vegetables, fruits, spices, algae, and other edible natural sources.

June 2025 - Rezolex filed antidumping and countervailing duty petitions against imports of oleoresin paprika from India, alleging unfair pricing and subsidy practices affecting the U.S. market.

May 2025 - Givaudan highlighted Endure Paprika and Amaize Orange-Red for Seasonings as natural color innovations designed to provide vibrant shades that closely match synthetic color alternatives in snack applications.

February 2025 - Oterra inaugurated a color blending and application center in Kerala, India, using raw materials such as turmeric, paprika, annatto, and red beet to serve India, Asia Pacific, and Middle East customers.

FAQ's

The Global Paprika Market is estimated to generate USD 559 million in revenue in 2024.

The Global Paprika Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 5.3% during the forecast period from 2025 to 2032.

The Paprika Market is estimated to reach USD 845 million by 2032.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!