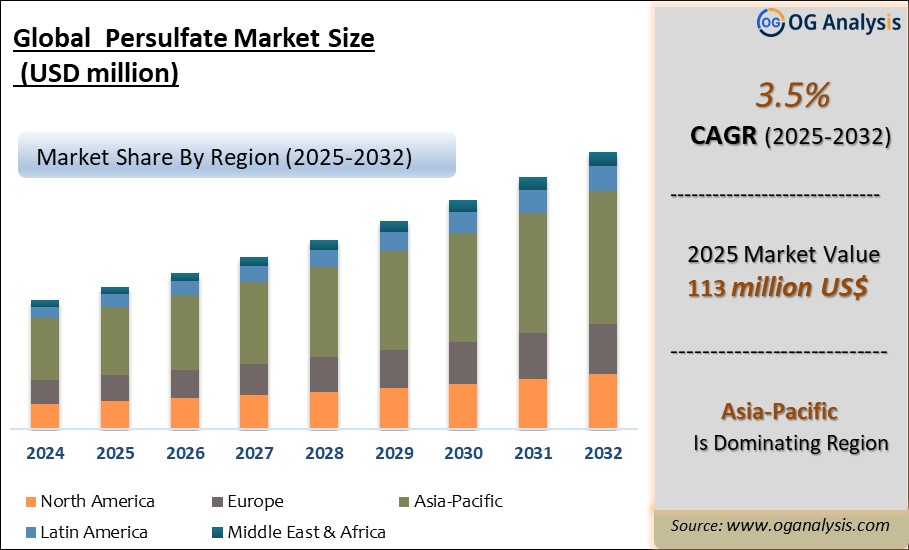

"The Persulfate Market is valued at $ 117.0 Million in 2026. and expected to grow at a significant CAGR of 3.5%, reaching $154.0 Million by the end of the forecast period in 2034."

The persulfate market is an important segment of the specialty oxidants and industrial chemicals industry, focused on ammonium persulfate, sodium persulfate, and potassium persulfate used as strong oxidizing agents across polymerization, electronics, cosmetics, water treatment, textiles, paper, oil and gas, and chemical synthesis applications. Persulfates are widely used as initiators in emulsion polymerization for plastics, rubbers, latex, coatings, adhesives, and resins, while also serving as etchants and cleaners in printed circuit board and semiconductor processes. Additional applications include hair bleaching formulations, soil and groundwater remediation, textile desizing, pulp and paper processing, and enhanced oxidation processes. Demand is being driven by growth in polymers, electronics manufacturing, personal care products, environmental remediation, and industrial cleaning applications requiring reliable oxidation performance.

Recent trends in the persulfate market include increasing demand for high-purity grades, stronger use in advanced oxidation processes, wider application in environmental cleanup, and growing focus on safer handling and compliant packaging. Manufacturers are emphasizing product consistency, purity, solubility, storage stability, and supply reliability to serve both bulk industrial and specialty applications. Growth is further supported by expansion in water treatment, electronics fabrication, acrylics, latex products, and specialty chemical production. Competitive dynamics are shaped by chemical producers, oxidant manufacturers, specialty chemical distributors, and regional suppliers competing on product grade range, technical support, raw material access, logistics, and regulatory compliance. At the same time, handling hazards, storage sensitivity, raw material cost changes, transportation controls, and competition from alternative oxidants continue to influence market development and procurement strategies.

Key Insights

- Polymerization remains the largest application area for persulfates, particularly in emulsion polymerization processes used to produce latex, acrylics, styrene-butadiene rubber, coatings, adhesives, and specialty resins. Persulfates act as efficient free-radical initiators, supporting controlled reaction performance. Demand is closely linked to downstream growth in plastics, paints, construction materials, packaging, and industrial coatings.

- Electronics and printed circuit board manufacturing provide important demand for high-purity persulfates used in etching, cleaning, and surface preparation processes. These applications require consistent quality and low impurity levels to protect process reliability. As electronics become more advanced and miniaturized, demand for carefully controlled specialty chemical grades continues to strengthen.

- Environmental remediation is an expanding opportunity, with persulfates increasingly used in advanced oxidation processes for soil and groundwater cleanup. Activated persulfate systems can help degrade organic contaminants and support remediation of industrial pollution sites. Regulatory pressure for cleaner water and land resources is strengthening interest in persulfate-based treatment technologies.

- Personal care applications remain relevant, especially in hair bleaching and cosmetic formulations where persulfates provide strong oxidative performance. Product demand is supported by salon services, home hair coloring, and beauty product innovation. However, manufacturers must address safety, labeling, and sensitivity concerns through careful formulation, packaging, and user guidance.

- Sodium persulfate, ammonium persulfate, and potassium persulfate each serve distinct application requirements based on solubility, reactivity, compatibility, and formulation needs. Sodium persulfate is often favored in environmental and industrial uses, ammonium persulfate in polymer and electronics applications, and potassium persulfate in cosmetics and specialty uses. Product selection remains highly application-specific.

- High-purity and specialty grades are gaining importance as end users in electronics, pharmaceuticals, and advanced chemical processing require tighter specifications and reliable performance. Suppliers that provide consistent quality, low contamination levels, and strong documentation are better positioned in premium applications. Quality assurance is becoming a central competitive differentiator.

- Handling, storage, and transportation requirements influence market practices because persulfates are strong oxidizers that require careful management to prevent contamination, decomposition, and safety incidents. Buyers increasingly value compliant packaging, technical guidance, and reliable logistics support. Strong safety management capability is essential for supplier credibility and customer retention.

- Future market growth will be driven by polymer demand, electronics manufacturing, environmental remediation, water treatment, and specialty chemical applications. Opportunities will expand where persulfates deliver controlled oxidation, high purity, and reliable process performance. Long-term competitiveness will depend on safety compliance, grade customization, supply stability, and application-specific technical support.

Trade Intelligence for persulfate market

| Global Peroxosulphates persulphates Trade, Imports, USD million, 2020-24 | |||||

|

| 2020 | 2021 | 2022 | 2023 | 2024 |

| World | 187 | 233 | 251 | 185 | 168 |

| Italy | 20 | 24 | 21 | 16 | 18 |

| Korea, Republic of | 26.0 | 23.4 | 20.1 | 13.8 | 13 |

| Taipei, Chinese | 14 | 16.5 | 18.6 | 10.2 | 12.3 |

| United States of America | 8.0 | 15.0 | 15.8 | 9.6 | 10.7 |

| Canada | 5.5 | 10.1 | 10.6 | 10.2 | 10.6 |

| Source: OGAnalysis, International Trade Centre (ITC) | |||||

- Italy, Korea, Republic of, Taipei, Chinese, United States of America and Canada are the top five countries importing 38.2% of global Peroxosulphates persulphates in 2024

- Global Peroxosulphates persulphates Imports decreased by 10.2% between 2020 and 2024

- Italy accounts for 10.6% of global Peroxosulphates persulphates trade in 2024

- Korea, Republic of accounts for 7.6% of global Peroxosulphates persulphates trade in 2024

- Taipei, Chinese accounts for 7.3% of global Peroxosulphates persulphates trade in 2024

| Global Peroxosulphates persulphates Export Prices, USD/Ton, 2020-24 |

|

|

| Source: OGAnalysis |

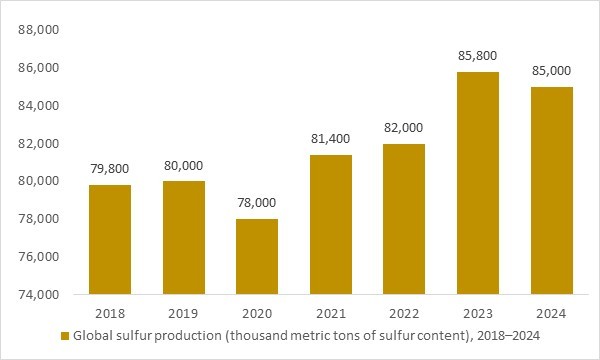

Global sulfur production (thousand metric tons of sulfur content), 2018–2024

Figure: Global sulfur production (thousand metric tons, sulfur content), 2018–2024, illustrating the stable feedstock base supporting growth in the Persulfate market.

- Global sulfur production from 2018 to 2024 provides a strong upstream indicator for the Persulfate market, as persulfates are synthesized from sulfur-based chemistries. The steady and resilient sulfur output over these years reflects a stable raw material base, supporting expanding demand from electronics, polymer processing, water treatment, and environmental remediation applications. This trend reinforces the market’s long-term supply security and highlights the depth of analysis behind OG Analysis’ Persulfate market insights.

Regional Analysis

North America Persulfate Market

North America remains a mature persulfate market, supported by strong demand from polymer manufacturing, electronics processing, personal care, water treatment, and environmental remediation applications. Market dynamics are shaped by industrial chemical consumption, strict environmental cleanup requirements, and demand for high-purity oxidants in specialty processes. Lucrative opportunities are strong in soil and groundwater remediation, high-purity electronics grades, polymerization initiators, and advanced oxidation systems. The forecast remains favorable as industries prioritize reliable oxidation chemistry, while latest developments focus on safer handling, compliant packaging, and specialty-grade product availability.

Asia Pacific Persulfate Market

Asia Pacific is the fastest-growing persulfate market, driven by expanding polymer production, electronics manufacturing, textile processing, cosmetics demand, and industrial chemical activity. Market dynamics are influenced by strong demand from printed circuit boards, synthetic latex, coatings, plastics, and beauty care formulations across major manufacturing economies. Lucrative opportunities are visible in ammonium persulfate, sodium persulfate, potassium persulfate, electronics cleaning, polymerization, and textile treatment applications. The forecast remains robust as regional industrial output expands, while latest developments focus on local production capacity, high-purity grades, and cost-efficient supply networks.

Europe Persulfate Market

Europe represents a regulation-driven persulfate market, supported by demand from specialty chemicals, environmental remediation, cosmetics, electronics, and polymer applications. Market dynamics are shaped by strict safety standards, sustainability expectations, and increasing use of advanced oxidation processes for water and soil treatment. Lucrative opportunities are concentrated in high-purity persulfates, environmental treatment, specialty polymer production, and compliant personal care formulations. The forecast remains constructive as industries focus on cleaner processing and controlled oxidation technologies, while latest developments center on safety documentation, low-impurity grades, and responsible chemical handling practices.

Middle East & Africa Persulfate Market

The Middle East & Africa persulfate market is developing steadily, supported by growth in water treatment, oil and gas chemicals, construction materials, textiles, and industrial processing. Market dynamics are influenced by the need for reliable oxidizing agents in remediation, cleaning, polymerization, and specialty chemical applications. Lucrative opportunities are emerging in sodium persulfate for environmental and water treatment uses, polymerization initiators, and industrial cleaning formulations. The forecast remains positive as industrial diversification and infrastructure development continue, while latest developments focus on distributor expansion, safer storage practices, and improved access to specialty oxidants.

South & Central America Persulfate Market

South & Central America presents promising opportunities in the persulfate market, supported by demand from polymers, textiles, cosmetics, water treatment, mining-related remediation, and industrial cleaning applications. Market dynamics are shaped by growing chemical processing activity, environmental management needs, and demand for oxidation solutions in manufacturing and treatment processes. Lucrative opportunities are visible in polymer initiators, hair bleaching ingredients, groundwater remediation, and textile processing. The forecast remains encouraging as regional industries modernize, while latest developments focus on supply reliability, technical support, and wider distribution of sodium, ammonium, and potassium persulfate grades.

Market Scope

| Parameter | Persulfate Market Scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Type

- Ammonium

- Potassium

- Sodium

By End Use

- Polymers

- Electronics

- Cosmetics & Personal Care

- Pulp, Paper & Textiles

- Oil & Gas

- Water Treatment

- Soil Remediation

- Others

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Companies

- Evonik Active Oxygens

- RheinPerChemie

- UI VR Persulfates (United Initiators)

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- Fujian ZhanHua Chemical Co., Ltd.

- Ak-Kim

- Yatai Electrochemistry Co. Ltd.

- Hebei Jiheng Group

- Fujian Jianou Yongsheng Industry

- San Yuan Chemical Co., Ltd.

Recent Developments

- November 2025 – Evonik Active Oxygens showcased KLOZUR persulfate solutions for in-situ soil and groundwater remediation, emphasizing practical guidance for contaminant removal and advanced oxidation applications.

- October 2025 – United Initiators updated sodium persulfate safety documentation, reinforcing handling, storage, transportation, and oxidizer safety guidance for industrial users.

- March 2025 – Evonik presented field data on potassium persulfate use in a permeable reactive barrier system for groundwater remediation, highlighting contaminant reduction and persistence under field conditions.

- 2025 – Evonik expanded technical communication around persulfates as sustainable oxidants for soil remediation, wastewater treatment, chemical synthesis, cosmetics, and electronics applications.

- 2025 – Evonik highlighted ammonium and sodium persulfate use in lithium iron phosphate battery recycling, supporting oxidative leaching routes for lithium recovery from battery cathode materials.

- 2025 – Evonik strengthened its persulfate application portfolio for hair bleaching and coloring formulations, positioning persulfates as key oxidizers for pigment removal and high-lift blonding products.

- 2025 – Mitsubishi Gas Chemical continued promoting its ammonium, potassium, and sodium persulfate portfolio for polymerization, etching, desizing, and printed circuit board soft-etching applications.

- 2025 – Persulfate suppliers increased emphasis on high-purity grades for electronics, polymerization, environmental remediation, and specialty oxidation processes requiring consistent quality and safe handling.

FAQ's

By 2034, the Persulfate Market is estimated to account for $ 154.0 million

The Global Persulfate Market is estimated to generate $ 117.0 million in revenue in 2026

The Persulfate Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 3.5% during the forecast period from 2026 to 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!