"Pet Food Extrusion Market is valued at $81.1 billion in 2025. Further, the market is expected to grow at a CAGR of 7.4% to reach $154 billion by 2034."

The pet food extrusion market is expanding rapidly, driven by the increasing demand for high-quality, nutritious, and processed pet food products. Extrusion is a widely used method in pet food manufacturing that involves cooking raw ingredients under high pressure and temperature to create kibble, treats, and other dry pet food forms. This process enhances digestibility, improves shelf life, and allows for the incorporation of vitamins, minerals, and functional ingredients that promote pet health. Pet owners are becoming more conscious about their pets' nutrition, leading to a shift toward premium and specialized pet food formulations, including grain-free, organic, and protein-rich diets. The growing humanization of pets and the demand for pet food with improved texture, flavor, and nutritional value have also driven market growth. Additionally, technological advancements in extrusion techniques have enabled manufacturers to produce pet food with better digestibility, palatability, and functional benefits. As pet food brands continue to innovate and develop extruded products that cater to specific dietary needs, the market is expected to experience steady growth, fueled by changing consumer preferences and advancements in food processing technology.

In 2024, the pet food extrusion market has witnessed key developments, particularly in ingredient innovation and processing efficiency. With a strong focus on sustainability and alternative protein sources, manufacturers are increasingly using plant-based proteins, insect-based proteins, and novel ingredients such as algae and mycoproteins in extruded pet food. These alternatives cater to the rising demand for eco-friendly and ethically sourced pet nutrition. Additionally, advancements in twin-screw extrusion technology have improved production efficiency, allowing manufacturers to create highly digestible and nutrient-dense pet food while maintaining cost-effectiveness. Another notable development is the increasing use of functional ingredients such as probiotics, omega fatty acids, and antioxidants in extruded pet food to support gut health, joint health, and overall pet well-being. Brands are also adopting cold extrusion techniques for the production of minimally processed pet food, which helps retain natural nutrients and flavors. The rise of premiumization in the pet food industry has further fueled the demand for customized and specialized extruded pet food formulas, targeting breed-specific, age-specific, and health-condition-specific dietary requirements. As a result, 2024 has marked a shift toward more science-driven, functional, and personalized pet nutrition.

Looking ahead to 2025 and beyond, the pet food extrusion market is expected to continue evolving with further innovations in ingredient sourcing, processing technology, and nutritional formulations. Artificial intelligence (AI) and machine learning are likely to play a larger role in optimizing extrusion processes, ensuring consistency in texture, nutritional value, and production efficiency. Sustainability will remain a key focus, with an increased emphasis on reducing carbon footprints, minimizing waste, and using biodegradable packaging for extruded pet food products. Additionally, personalized nutrition is expected to gain traction, with brands offering tailor-made extruded pet food solutions based on a pet’s breed, age, weight, and specific health conditions. The integration of blockchain technology in pet food production is also anticipated, enhancing transparency and traceability in ingredient sourcing and quality control. Moreover, the demand for grain-free, gluten-free, and hypoallergenic extruded pet food will continue to rise as pet owners become more aware of food sensitivities and dietary intolerances in their pets. With these advancements, the pet food extrusion market is set to experience sustained growth, driven by health-conscious pet owners, technological innovations, and increasing demand for premium and functional pet nutrition.

Key Insights

-

Historically, pet food extrusion developed from snack and breakfast cereal technologies, giving manufacturers a proven, scalable method to produce dry pet diets. This heritage established a strong engineering base and know-how around expansion, shaping, and drying, which remains central to current processing lines. Over time, dedicated pet food extruders have evolved with design tweaks specific to animal nutrition needs.

-

Dry extruded kibbles remain the dominant format in many markets, providing convenient, shelf-stable, and cost-effective diets for dogs and cats. Extrusion allows consistent sizing, density control, and surface structure that influence palatability and chewing behavior. The ability to tailor kibble shape and hardness for small, medium, and large breeds is a key value driver for brand differentiation.

- Product diversification has extended extrusion beyond basic kibbles into co-extruded treats, dental chews, filled pillows, and semi-moist snacks. These formats use combinations of single- and twin-screw extruders, co-extrusion dies, and specialized drying and coating systems. As treats and snacks grow faster than staple diets in many markets, this segment represents an important growth frontier for extrusion technology.

- Raw-material flexibility is a major advantage of extrusion, enabling the use of cereals, pulses, rendered meals, fresh and frozen meats, by-product streams, and emerging protein sources. Modern extruders are designed to handle high-protein, high-fat, and low-starch formulations associated with grain-free, high-meat, and limited-ingredient diets. This versatility helps manufacturers maintain agility in the face of volatile ingredient markets.

- Functional and health-focused pet nutrition is pushing processors to achieve more precise control over temperature, moisture, and residence time to protect sensitive ingredients. Probiotics, heat-labile vitamins, omega-rich oils, and specialty fibers often require gentle processing and carefully sequenced addition. Extrusion lines increasingly integrate pre-conditioning, vacuum coating, and post-addition technologies to safeguard nutrient integrity.

- Automation and digitalisation are transforming the pet food extrusion landscape, with advanced control systems managing recipe changes, process parameters, and real-time quality monitoring. Data logging, predictive maintenance, and remote diagnostics are becoming standard, helping operators reduce downtime, improve consistency, and respond quickly to formulation and demand changes. This also supports tighter traceability and audit requirements.

- Energy efficiency and sustainability considerations are influencing equipment design and plant layouts. Manufacturers focus on optimizing steam usage in pre-conditioners, reducing specific energy consumption of extruders, and improving heat recovery in dryers. The ability to process local ingredients, co-products, and novel proteins also supports broader sustainability narratives for pet food brands and retailers.

- The competitive landscape is characterized by a mix of global extrusion specialists and regional machinery suppliers offering standard and customized lines. Successful vendors combine mechanical engineering expertise with application laboratories, pilot plants, and formulation support, enabling customers to co-develop new recipes and rapidly scale from trials to commercial production. After-sales service and spare-part availability are critical purchasing criteria.

- Regulatory and safety expectations drive continuous refinement of hygienic design, allergen control, and cleaning protocols in extrusion plants. Equipment with accessible, easy-to-clean contact surfaces, reduced dead zones, and validated cleaning procedures helps minimize cross-contamination risks. As pet food recalls remain high-profile events, processors prioritize extruder and dryer designs that support robust food safety management systems.

- Looking ahead, the pet food extrusion market is expected to benefit from continued pet population growth, humanization, and premiumization, as well as the rise of emerging markets. Future opportunities include extruded formats for alternative species, greater integration with wet and fresh pet food portfolios, and hybrid lines capable of handling both conventional and novel ingredient sets. Suppliers that offer flexible, scalable, and digitally enabled extrusion solutions are well positioned to capture long-term demand.

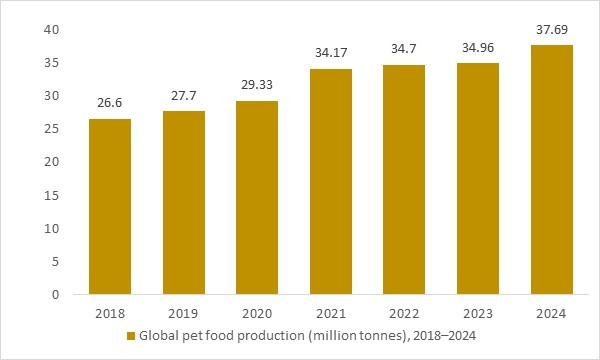

Global pet food production (million tonnes), 2018–2024

Figure: Global pet food production (million tonnes), 2018–2024, illustrating the strong, expanding throughput base driving demand for advanced pet food extrusion equipment and processing lines.

- Global pet food production rose from around 26.6 million tonnes in 2018 to nearly 38 million tonnes in 2024, reflecting sustained growth in dry kibble and extruded pet formulations. This steady expansion in raw material throughput directly supports rising investment in high-capacity, energy-efficient pet food extrusion lines, advanced process controls, and tailored after-sales services across key pet food manufacturing regions worldwide.

Regional Insights

North America Pet food extrusion market

In North America, the pet food extrusion market is underpinned by a large, premium-oriented pet food industry and high levels of plant automation. Major brand owners and private-label co-packers invest in advanced single- and twin-screw extruders to support a wide range of dry kibbles and treats, from economy lines to super-premium, high-meat recipes. The region’s strong focus on pet humanization drives demand for novel shapes, textures, and functional inclusions, requiring highly flexible extrusion setups and quick recipe changeovers. Labour constraints and rising operating costs are encouraging greater use of process automation, real-time monitoring, and data-driven optimization in extrusion plants. Strict food safety, traceability, and labelling expectations push processors toward hygienic designs, robust control systems, and tighter integration between extrusion, drying, coating, and packaging. Growth is further supported by the expansion of e-commerce and specialty retail, which continually create niches for differentiated, extruded pet food and snack formats.

Europe Pet food extrusion market

In Europe, the pet food extrusion market is shaped by mature pet ownership, strong regulatory frameworks, and a pronounced shift toward natural, sustainable, and specialty nutrition. Extruded dry diets and treats remain core formats, but recipe design is increasingly influenced by grain-free, limited-ingredient, and alternative-protein trends across key markets. European processors tend to emphasize energy-efficient, low-waste extrusion lines that align with environmental and corporate sustainability goals. The presence of several leading equipment manufacturers supports continuous innovation in extruder design, process control, and hygienic engineering. Regulatory scrutiny on ingredient sourcing, additives, and claims pushes manufacturers to tightly control thermal profiles, residence times, and post-extrusion coating steps to preserve sensitive nutrients. Cross-border trade within the region also encourages plants to operate with high uptime and consistent quality, keeping demand steady for reliable, upgradeable extrusion solutions.

Asia-Pacific Pet food extrusion market

Asia-Pacific is the fastest-growing region for pet food extrusion, driven by rising pet ownership, urbanization, and the shift from table scraps and home-prepared feeds to commercial diets. As local and regional brands scale up, investment in modern extrusion plants is increasing to meet demand for dry dog and cat foods as well as emerging snack and treat categories. International and domestic equipment suppliers are supplying both entry-level and high-spec lines, with many facilities designed to accommodate future capacity expansions. Formulations in the region often balance cost sensitivity with rising expectations for quality, leading to extruded products that blend regional ingredient bases with global nutrition concepts. Growing use of contract manufacturers and co-packers is also expanding the installed base of flexible extrusion lines capable of producing multiple brands and recipes. Over time, stricter regulatory standards and retailer expectations are expected to push more producers toward advanced automation, process control, and food safety features in extrusion systems.

Market Scope

| Parameter | Pet food extrusion Market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Extruder Type

- Single Screw

- Twin Screw

By Process

- Hot Extrusion

- Cold Extrusion

By Type

- Complete Diets

- Treats

- Other Types

By Ingredient

- Animal Derivatives

- Vegetables And Fruits

- Grains And Oilseeds

- Vitamins And Minerals

- Additives

- Other Ingredients

By Animal Type

- Dog

- Cat

- Fish

- Birds

- Other Animal Types

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- Nestlé S.A.

- Mars Petcare Inc.

- Andtriz AG

- The J.M. Smucker Company

- Ingredion Incorporated

- SunPring

- Buhler Industries Inc.

- Pavan Group

- Reading Bakery Systems Inc.

- Clextral SAS

- Brabender GmbH & Co. KG

- Baker Perkins Ltd.

- Lindquist Machine

- American Extrusion International

- Nanjing Haisi Extrusion Equipment Co. Ltd.

- Diamond America Corporation

- Doering Systems Inc

- Coperion Ideal Private Limited

- The Bonnot Company

- IDAH Company

- Shandong Loyal Industrial Co. Ltd.

- Kairong Group

- Kahl Group

- Wenger Manufacturing Inc.

- Triott Group.

Recent Industry Developments

-

Sep 2025 – ANDRITZ: Launched the ExMax S1021 high-performance extruder for pet food and aquafeed, emphasizing automated control of cooking/expansion for more consistent kibble quality. The design focus is on higher hygiene, faster recipe changeovers, and reduced cross-contamination risk.

-

May 2025 – Wenger + Extru-Tech: Jointly launched EXPRO AI, an AI-driven extrusion optimization software that predicts outcomes and tunes setpoints to reduce variability. It is positioned to improve throughput stability, product consistency, and operating efficiency for pet food lines.

-

Mar 2025 – CPM: Unveiled an expanded pet food processing equipment lineup at VIV Asia 2025, including twin-screw extrusion platforms and downstream systems (drying/coating/milling). The announcement reflects continued push toward integrated, turnkey extrusion lines for premium pet food.

-

Mar 2025 – VIV (Petfood & Aquafeed Extrusion Conference): Hosted a specialized extrusion conference centered on pet food/aquafeed extrusion equipment and process control. The event spotlighted the industry shift toward advanced automation, sanitation-by-design, and flexible lines for novel formulations.

-

2024 – Coperion (Baker Perkins): Promoted co-extrusion technology (e.g., filled pet treats) as a value-add route for premiumization, supporting more complex shapes and filled formats. This points to rising investment in higher-margin treat extrusion versus standard kibble.

-

Jun 2024 – Baker Perkins: Highlighted modular, sanitation-friendly baking systems used after extrusion to improve texture and throughput in pet food processing. The focus aligns with processors upgrading post-extrusion steps to increase line uptime and reduce cleaning time.

FAQ's

The Global Pet Food Extrusion Market is estimated to generate USD 81.1 billion in revenue in 2025.

The Global Pet Food Extrusion Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 7.4% during the forecast period from 2025 to 2034.

The Pet Food Extrusion Market is estimated to reach USD 154 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!