"The PFA (Polyfluoroalkoxy) Welding Film Market Size is valued at $389.8 Million in 2025. Worldwide sales of PFA (Polyfluoroalkoxy) Welding Film Market are expected to grow at a significant CAGR of 4.6%, reaching $534 Million by the end of the forecast period in 2032."

The PFA (polyfluoroalkoxy) welding film market is experiencing steady growth driven by rising demand for high-performance thermoplastic films in chemical processing, semiconductor manufacturing, pharmaceutical, and industrial applications requiring excellent thermal stability, chemical resistance, and weldability. PFA welding films are fluoropolymer films made from copolymers of perfluoroalkyl vinyl ether and tetrafluoroethylene, offering a unique combination of mechanical strength, optical clarity, flexibility, and non-stick properties while maintaining performance at continuous temperatures up to 260°C. These films are widely used as welding liners, release films, and protective barriers for tanks, pipelines, lining systems, and cleanroom equipment where chemical inertness and contamination-free processing are critical. Growth in the semiconductor industry, increasing adoption in chemical tank linings, and expanding use in high-purity fluid handling systems are supporting market expansion globally.

Regionally, North America and Europe dominate the PFA welding film market due to established semiconductor and chemical manufacturing sectors, stringent quality standards, and early adoption of advanced fluoropolymer solutions for critical applications. Asia Pacific is the fastest-growing region, driven by rapid growth in semiconductor fabrication, electronics manufacturing, and chemical processing investments in countries such as China, South Korea, Taiwan, and Japan. However, challenges remain including high production costs, limited raw material availability, and specialized processing requirements that restrict market entry for smaller manufacturers. Leading companies are focusing on developing ultra-thin, precision-grade welding films, expanding production capacities, and integrating sustainable fluoropolymer manufacturing practices to enhance market competitiveness. As demand for high-purity, thermally stable, and chemically inert films increases across advanced manufacturing sectors, the PFA welding film market is poised for sustained growth in the coming years.

Standard PFA welding film is the largest product segment in the PFA polyfluoroalkoxy welding film market due to its widespread use in semiconductor manufacturing, chemical processing, and fluid handling systems that require high purity, chemical resistance, and thermal stability without the need for additional reinforcement. Reinforced PFA welding film is the fastest-growing segment as its enhanced mechanical strength and dimensional stability make it ideal for heavy-duty industrial applications, including aggressive chemical environments and high-pressure lining systems.

Chemical processing is the largest application segment in the market, driven by extensive use of PFA welding films as liners, tank linings, and protective barriers for pipes and equipment handling corrosive chemicals, ensuring safety, compliance, and extended equipment life. Electrical insulation is the fastest-growing application segment, supported by rising demand in semiconductor fabrication, electronics manufacturing, and high-voltage systems where PFA films provide superior dielectric properties, thermal resistance, and chemical inertness for reliable performance in critical environments.

Trade Intelligence PFA (polyfluoroalkoxy) welding film market

| Global Unworked non-cellular plastic sheets/films n.e.s (non-reinforced, non-backed) Trade, Imports, USD million, 2020-24 | |||||

|

| 2020 | 2021 | 2022 | 2023 | 2024 |

| World | 6,762 | 8,156 | 8,088 | 7,220 | 7,001 |

| China | 1,724 | 2,107 | 1,852 | 1,773 | 1,823 |

| India | 357 | 645 | 757 | 591 | 411 |

| Vietnam | 555 | 523 | 574 | 403 | 370 |

| Germany | 284 | 371 | 387 | 408 | 366 |

| South Korea | 492 | 573 | 450 | 366 | 352 |

| Source: OGAnalysis, International Trade Centre (ITC) | |||||

- China , India , Vietnam , Germany and South Korea are the top five countries importing 47.4% of global Unworked non-cellular plastic sheets/films n.e.s (non-reinforced, non-backed) in 2024

- Global Unworked non-cellular plastic sheets/films n.e.s (non-reinforced, non-backed) Imports increased by 3.5% between 2020 and 2024

- China accounts for 26% of global Unworked non-cellular plastic sheets/films n.e.s (non-reinforced, non-backed) trade in 2024

- India accounts for 5.9% of global Unworked non-cellular plastic sheets/films n.e.s (non-reinforced, non-backed) trade in 2024

- Vietnam accounts for 5.3% of global Unworked non-cellular plastic sheets/films n.e.s (non-reinforced, non-backed) trade in 2024

| Global Unworked non-cellular plastic sheets/films n.e.s (non-reinforced, non-backed) Export Prices, USD/Ton, 2020-24 |

| |

| Source: OGAnalysis, International Trade Centre (ITC) |

Key Insights PFA (polyfluoroalkoxy) welding film market

- The PFA polyfluoroalkoxy welding film market is driven by increasing demand for high-performance fluoropolymer films in semiconductor manufacturing, chemical processing, and pharmaceutical industries requiring exceptional chemical resistance and thermal stability for critical containment and lining applications.

- PFA welding films offer superior thermal stability up to 260°C, excellent mechanical strength, and high flexibility, making them ideal for welding liners, release films, and protective barriers in high-purity fluid handling systems and corrosion-resistant equipment.

- North America and Europe dominate the market due to mature semiconductor fabrication sectors, strong chemical manufacturing bases, and early adoption of advanced fluoropolymer solutions complying with stringent purity and safety standards in industrial operations.

- Asia Pacific is the fastest-growing region, driven by rapid growth in semiconductor and electronics manufacturing in China, Taiwan, South Korea, and Japan, where PFA films are used in wafer processing, chemical delivery lines, and cleanroom equipment protection.

- Increasing investments in the global semiconductor industry, supported by chip production capacity expansion and government subsidies, are fueling demand for PFA welding films used as liners and protective films in ultra-clean and corrosive environments.

- High production costs and specialized processing requirements remain market challenges, as PFA welding films require advanced extrusion, precision casting, and sintering techniques, limiting production capabilities to a few global fluoropolymer manufacturers.

- Technological advancements are focusing on developing ultra-thin, high-clarity, and precision-grade welding films to cater to microelectronics, advanced chemical containment systems, and pharmaceutical cleanroom barrier applications requiring optical clarity and contamination-free performance.

- Leading manufacturers are expanding their production capacities and investing in sustainable fluoropolymer manufacturing practices, including fluorine recovery systems and low-carbon production technologies, to strengthen market competitiveness and meet regulatory compliance.

- The market is witnessing rising demand for PFA welding films in high-purity chemical tank linings and dual laminate systems, where their chemical inertness and weldability extend equipment life and reduce maintenance downtime in aggressive processing environments.

- Strategic partnerships between film manufacturers, semiconductor chemical suppliers, and equipment fabricators are increasing, facilitating integrated solutions, process validation support, and tailored welding film grades for specialized high-purity industrial applications globally.

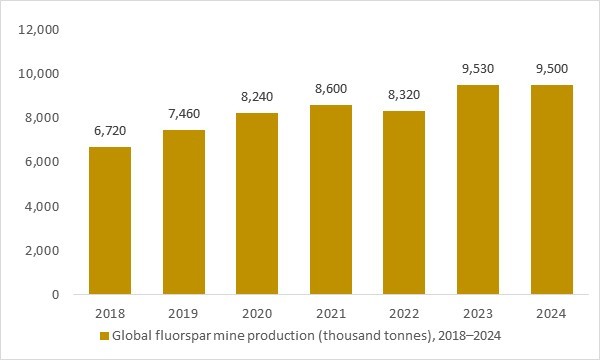

Global fluorspar mine production (thousand tonnes), 2018–2024

Figure: Global fluorspar mine production (thousand tonnes), 2018–2024e, highlighting the expanding raw-material base for high-performance fluoropolymers used in PFA (polyfluoroalkoxy) welding films and advanced chemical processing applications.

- Global fluorspar mine production has shown a steady upward trend from 2018 to 2024e, reinforcing the strength of the raw-material base required for high-performance fluoropolymers such as PFA. As fluorspar is the essential feedstock for hydrofluoric acid and fluoromonomers, its availability directly influences PFA welding film pricing, processing stability, and long-term supply security. This trend highlights a supportive environment for capacity expansion and technology adoption across advanced manufacturing, semiconductor, and chemical-processing applications.

Regional Insights

North America PFA (polyfluoroalkoxy) welding film market

In North America, the PFA (polyfluoroalkoxy) welding film market is supported by a strong installed base of high-performance process industries, including chemical processing, semiconductor, aerospace, and advanced composites. PFA welding films are used as hot-melt adhesive layers and bondable interlayers for PTFE-coated glass fabrics, corrosion-resistant linings, high-temperature insulation, and release films in composite lay-up. Equipment builders and fabricators value PFA welding films for their combination of high continuous-use temperature, chemical inertness, weldability, and transparency, enabling reliable bonding without liquid adhesives. Growth is further supported by ongoing investment in semiconductor capacity, battery and fuel-cell plants, and aerospace composite facilities, all of which use fluoropolymer films in critical components and tooling. At the same time, tightening state-level and federal scrutiny of PFAS (“forever chemicals”) is pushing users and suppliers to improve emissions control, documentation, and end-of-life strategies, rather than immediately abandoning fluoropolymer films that are considered mission-critical.

Europe PFA (polyfluoroalkoxy) welding film market

In Europe, demand for PFA welding films is closely linked to advanced manufacturing in chemicals, pharmaceuticals, automotive, aerospace, and renewable energy equipment. PFA films are used as weldable liners, release films, and bonding media in composite structures and corrosion-resistant components operating in harsh thermal and chemical environments. European producers and converters are among the leading global suppliers of fluoropolymer films, offering extruded and welding-grade PFA films tailored for bonding PTFE fabrics, process belts, and engineered parts. However, the region is also at the forefront of PFAS regulatory initiatives, including REACH-based universal PFAS restriction proposals and specific caps on PFAS emissions, which drive investment in cleaner manufacturing technologies, traceability, and potential long-term substitution strategies. For the foreseeable future, exemptions for critical uses in semiconductors, aerospace, and other strategic sectors are expected to sustain PFA welding film demand, but under much stricter environmental performance requirements.

Asia-Pacific PFA (polyfluoroalkoxy) welding film market

Asia-Pacific is the manufacturing growth engine for PFA welding films, underpinned by rapid expansion in electronics, semiconductors, chemical processing, solar energy, and high-end industrial equipment. Major fluoropolymer producers and converters in Japan, China, and other regional hubs offer PFA films for welding, thermoforming, and bonding, supplying local and export markets with a wide range of thicknesses and widths. PFA welding films are widely used in corrosion-resistant linings, composite release films for aerospace and wind blades, and high-purity fluid handling in chip fabs and battery plants, where their thermal stability and chemical resistance are essential. Regional governments’ focus on localizing advanced materials supply chains also supports investment in fluoropolymer film capacity. At the same time, emerging PFAS regulations in countries such as Japan, along with export-market requirements, are pushing Asian producers to enhance emissions control, product stewardship, and documentation, but overall demand for PFA welding films remains on an upward trajectory.

Reort Scope

| Parameter | PFA (Polyfluoroalkoxy) Welding Film Market Scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By Diagnostic Method, By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

PFA (Polyfluoroalkoxy) Welding Film Market Segmentation

By Product

- Standard PFA Welding Film

- Reinforced PFA Welding Film

By Application

- Electrical Insulation

- Chemical Processing

- Food Processing

By End User

- Aerospace

- Automotive

- Pharmaceuticals

- Electronics

By Technology

- Flame Welding

- Laser Welding

By Distribution Channel

- Direct Sales

- Distributors

- Online Sales

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Top 15 Companies Operating in the PFA (Polyfluoroalkoxy) Welding Film Market

- Daikin Industries Ltd.

- 3M Company

- The Chemours Company

- Arkema Group

- Saint-Gobain Performance Plastics

- Fluoroseals SpA

- Entegris Inc.

- Technetics Group

- Chukoh Chemical Industries, Ltd.

- Zeus Industrial Products, Inc.

- Dongyue Group Ltd.

- Shanghai 3F New Materials Company Limited

- Hubei Everflon Polymer Co., Ltd.

- RTP Company

- Hengli Corporation

Recent Industry Developments

-

Nov 2025 — Daikin: Showcased semiconductor-focused fluoropolymer materials where PFA films used for welding/lining support high-purity chemical handling and contamination control.

-

Aug 2025 — Chemours: Announced a major environmental-claims settlement update that is closely watched by fluoropolymer supply chains supporting PFA film and welding applications.

-

Feb 2025 — Chemours: Reported improved availability tied to expanded Teflon™ PFA capability, supporting downstream conversion into PFA films and welding film formats for high-purity systems.

-

Nov 2024 — GMM Pfaudler / Edlon: Highlighted PureFusion™ fluoropolymer welding technology for ultra-high-purity vessels, reinforcing demand for PFA welding films/sheets used in seam construction.

-

Aug 2024 — Chemours: Communicated progress toward expanding PFA production, supporting semiconductor-driven growth that lifts consumption of PFA films and welding materials in wet-process infrastructure.

-

Jun 2024 — AGC: Reiterated capacity expansion plans for high-performance fluorine resins aligned with semiconductor demand, supportive of upstream supply for PFA-class film applications.

-

Jan 2024 — GMM Pfaudler / Edlon: Announced a dedicated semiconductor equipment manufacturing site expansion, where welded fluoropolymer liners/films are integral for harsh chemical service.

-

Mar 2023 — AGC: Announced a major fluorochemical capacity investment to support rising semiconductor and high-purity applications that underpin downstream PFA film and welding film use.

What You Receive

• Global Pfa Polyfluoroalkoxy Welding Film market size and growth projections (CAGR), 2024- 2034

• Impact of recent changes in geopolitical, economic, and trade policies on the demand and supply chain of Pfa Polyfluoroalkoxy Welding Film.

• Pfa Polyfluoroalkoxy Welding Film market size, share, and outlook across 5 regions and 27 countries, 2025- 2034.

• Pfa Polyfluoroalkoxy Welding Film market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2025- 2034.

• Short and long-term Pfa Polyfluoroalkoxy Welding Film market trends, drivers, restraints, and opportunities.

• Porter’s Five Forces analysis, Technological developments in the Pfa Polyfluoroalkoxy Welding Film market, Pfa Polyfluoroalkoxy Welding Film supply chain analysis.

• Pfa Polyfluoroalkoxy Welding Film trade analysis, Pfa Polyfluoroalkoxy Welding Film market price analysis, Pfa Polyfluoroalkoxy Welding Film Value Chain Analysis.

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products.

• Latest Pfa Polyfluoroalkoxy Welding Film market news and developments.

The Pfa Polyfluoroalkoxy Welding Film Market international scenario is well established in the report with separate chapters on North America Pfa Polyfluoroalkoxy Welding Film Market, Europe Pfa Polyfluoroalkoxy Welding Film Market, Asia-Pacific Pfa Polyfluoroalkoxy Welding Film Market, Middle East and Africa Pfa Polyfluoroalkoxy Welding Film Market, and South and Central America Pfa Polyfluoroalkoxy Welding Film Markets. These sections further fragment the regional Pfa Polyfluoroalkoxy Welding Film market by type, application, end-user, and country.

FAQ's

The Global PFA (Polyfluoroalkoxy) Welding Film Market is estimated to generate USD 389.8 Million in revenue in 2025.

The Global PFA (Polyfluoroalkoxy) Welding Film Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 4.6% during the forecast period from 2025 to 2032.

The PFA (Polyfluoroalkoxy) Welding Film Market is estimated to reach USD 534 Million by 2032.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!