"The Pharmaceutical Logistics Market was valued at $ 121.99 billion in 2025 and is projected to reach USD 274.62 billion by 2034, growing at a CAGR of 9.44%."

The pharmaceutical logistics market underpins the safe, traceable, and timely movement of medicines, vaccines, biologics, and medical devices from API plants and fill-finish sites to hospitals, pharmacies, and patients. It spans temperature-controlled storage and transport across controlled room temperature (15–25 °C), cold chain (2–8 °C), frozen (−20 °C), and ultra-low (≤ −70 °C) ranges, with validated packaging, lane qualification, and real-time monitoring to protect product integrity. Providers integrate Good Distribution Practice (GDP) standards, serialization, and quality management systems with multimodal networks that combine air, road, and ocean, supported by GMP-compliant hubs, cross-docks, and value-added services such as kitting, late-stage customization, and clinical trial distribution. Growth is propelled by the rise of specialty therapies, cell-and-gene treatments with narrow stability windows, and direct-to-patient models that elevate last-mile reliability. Digital control towers fuse WMS/TMS data with IoT sensors for temperature, shock, and location, enabling exception management and release-to-market speed. As health systems emphasize access and resilience, logistics partners are expanding validated capacity, adopting reusable shippers and phase-change materials, and aligning with sustainability goals through route optimization, electric fleets, and sustainable aviation fuel allocations all while meeting stringent regulatory expectations and patient safety requirements.

Market dynamics reflect simultaneous needs for speed, certainty, and cost control: biologics and vaccines require high-assurance cold chains; generics and OTC portfolios demand scalable, efficient fulfillment; and clinical supplies call for blinded kitting, comparator sourcing, and rapid returns. Opportunities emerge in ready-to-use ultra-low infrastructure for advanced therapies, temperature-mapped home-care logistics, and integrated reverse flows for recalls, waste segregation, and refurbishment of reusable assets. Leading providers differentiate through GDP-trained workforces, standardized lane risk assessments, and data-driven continuous improvement that reduces excursions and write-offs. Trends include digitized proof of compliance, eCMR adoption, predictive ETA with lane-level risk scoring, and product passports that connect batch genealogy to packaging and transport metadata. Regionalization and nearshoring are reshaping networks to shorten lead times and mitigate disruption, while harmonized documentation and brokerage services compress border clearance. Looking ahead, steady growth is expected as aging populations, chronic disease management, and vaccination programs expand demand for reliable distribution. Recent priorities focus on automating pharma campuses, scaling ultra-cold cross-docks near gateway airports, deploying standardized packaging pools, and advancing circular logistics models positioning pharmaceutical logistics as a critical enabler of therapy availability, quality assurance, and health-system efficiency.

Key Market Insights

- The market’s core growth engine is the shift toward specialty medicines biologics, vaccines, and cell-and-gene therapies that demand validated temperature control and end-to-end visibility. Rising chronic disease burdens and aging populations lift baseline volumes across wholesalers, specialty pharmacies, and hospital systems. Direct-to-patient programs add high-touch last-mile needs and tighter delivery windows. Together, these dynamics elevate quality, speed, and traceability expectations. Providers that fuse compliance with agility capture share.

- Cold chain architecture is diversifying across CRT, 2–8 °C, frozen, and ultra-low segments, each with distinct packaging, lane, and handling rules. Phase-change systems and qualified passive shippers extend hold times while reducing dry-ice dependency. Pooled, reusable container programs lower waste and stabilize performance across seasons. Lane qualification and temperature mapping are now baseline, not differentiators. The edge lies in faster requalification and data-rich route design.

- Digital control towers integrate WMS/TMS feeds with IoT loggers for temperature, shock, and location, enabling real-time exception management. Predictive ETAs and lane risk scoring preempt excursions and missed appointments. Serialization and aggregation data improve pedigree, recall precision, and diversion defense. Automated release workflows compress dwell at hubs and border points. Dashboards that tie quality metrics to cost-to-serve drive continuous improvement.

- Clinical trial logistics require blinded kitting, comparator sourcing, and rapid resupply under Good Clinical Practice. Decentralized trials expand direct-to-patient shipments and nurse visit coordination with returns and accountability. For cell-and-gene therapies, chain-of-identity and chain-of-condition are mission-critical from collection to reinfusion. Flexible depots near study hotspots reduce cycle time and waste. Sponsors value partners who harmonize global SOPs with site-level nuance.

- Last-mile specialization is accelerating temperature-mapped totes, secure hand-offs, and white-glove services protect high-value therapies. Appointment scheduling, delivery verification, and patient engagement tools support adherence. For home care, validated coolers and short-route consolidation maintain stability without over-packaging. Urban micro-fulfillment nodes reduce lead times and re-delivery risk. Metrics now extend beyond OTIF to include clinical impact proxies and patient experience.

- Network strategies are shifting toward regionalization and multi-node designs that shorten lead times and diversify risk. Nearshoring of fill-finish and secondary packaging eases customs exposure and airfreight reliance. Cross-docks at gateway airports expand ULT and 2–8 °C throughput during peaks. Mode-mix optimization balances air speed with ocean and road cost efficiency. Partnerships with health systems and CDMOs tighten planning synchrony.

- Compliance remains a defining moat: GDP-aligned SOPs, audit readiness, and data integrity controls underpin trust. Standardized CAPA, deviation triage, and change control reduce variability across sites. eCMR and digitized proof-of-delivery cut paperwork lag and error rates. Documented training and lane requalification cycles withstand regulator scrutiny. Vendors that translate regulation into scalable playbooks become preferred partners.

- Sustainability levers are moving from pilots to procurement criteria reusable shippers, route optimization, and right-sized packaging reduce emissions and waste. EV fleets and idle-reduction programs decarbonize urban deliveries; SAF allocations temper long-haul air impacts. Supplier scorecards increasingly track refrigerant choice and end-of-life outcomes. Accurate emissions baselines unlock credible reduction targets. Circular asset pools improve both ESG and cost profiles.

- Resilience planning is now continuous, covering extreme weather, strikes, geopolitics, and port congestion. Dual-lane and dual-carrier designs provide failover across critical corridors. Buffer capacity in 2–8 °C and ULT mitigates shock during demand surges. Playbooks codify rapid mode switches and priority allocations for life-saving products. Scenario drills and digital twins pressure-test networks before disruptions hit.

- Economics hinge on matching service level to therapy value expedited air for critical biologics, optimized parcel-to-freight consolidation for routine replenishment. Dynamic order allocation reduces partials and accessorials. Packaging redesign trims volumetric weight while maintaining stability. Vendor-managed inventory at depots smooths peaks and cuts expedites. Transparency on cost-to-serve by SKU and lane informs contracting and formulary planning.

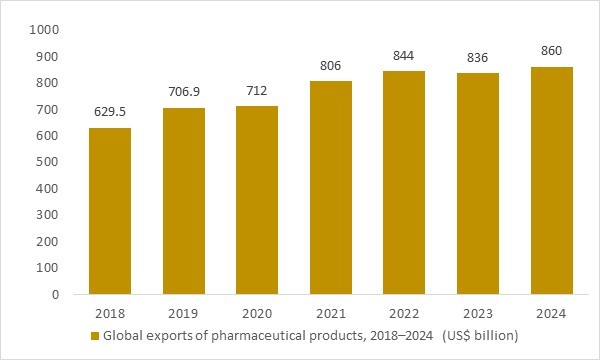

Global exports of pharmaceutical products, 2018–2024 (US$ billion)

Figure: Global exports of pharmaceutical products increased steadily between 2018 and 2024, reflecting rising cross-border trade in medicines, vaccines and biopharmaceuticals. As more high-value and temperature-sensitive drugs move through international supply chains, demand for specialized pharmaceutical logistics – including GDP-compliant warehousing, cold-chain transport and secure distribution – strengthens across major trade corridors. This OG Analysis chart illustrates how sustained growth in pharma exports underpins long-term opportunities in the pharmaceutical logistics market.

- Rising global exports of pharmaceutical products between 2018 and 2024 highlight how fast cross-border trade in medicines, vaccines and biopharmaceuticals is expanding. As more high-value, temperature-sensitive therapies move through international supply chains, shippers, 3PLs and carriers must invest in GDP-compliant warehousing, cold-chain capacity and time-critical transport solutions. This structural growth in pharma trade therefore underpins long-term demand for specialized pharmaceutical logistics services across air, sea, road and last-mile distribution.

Regional Insights

North America – Pharmaceutical Logistics Market

North America’s pharmaceutical logistics market is defined by stringent compliance, high specialty-drug penetration, and a dense network of GDP-aligned hubs that connect manufacturers, 3PLs, specialty pharmacies, and providers. Market dynamics favor temperature-controlled capacity across CRT, 2–8 °C, frozen, and ultra-low ranges, with validated lane design, real-time telemetry, and automated release workflows that compress dwell times. Lucrative opportunities include ready-to-use ultra-low cross-docks for cell-and-gene therapies, direct-to-patient last-mile with temperature-mapped totes, and standardized reusable shipper pools that cut waste and cost. Latest trends feature AI-assisted ETA and lane risk scoring, e-documentation for faster border and state transfers, digital product passports tied to serialization, and low-carbon operations using EV fleets and sustainable aviation fuel allocations. The forecast points to resilient growth as outpatient care expands, mail-order and home infusion scale, and nearshoring of fill-finish reduces lead-time volatility. Recent developments emphasize campus automation, parcel-to-freight consolidation for cost-to-serve control, and collaborative playbooks with health systems and CDMOs to synchronize planning and mitigate excursions.

Asia Pacific – Pharmaceutical Logistics Market

Asia Pacific combines rapid pharmaceutical manufacturing growth with expanding access to care, creating diverse, multi-temperature distribution needs from large metros to remote geographies. Market dynamics prioritize cost-to-quality optimization, localized packaging and qualification services, and flexible multimodal corridors linking pharma parks, free-trade zones, and export gateways. Lucrative opportunities arise in greenfield cold-chain nodes near production clusters, bonded gateways for clinical and commercial traffic, cross-border e-commerce health shipments, and drone-assisted last-mile where terrain and infrastructure challenge reliability. Latest trends include cloud dashboards for IoT loggers, RFID/UHF for kit-level visibility, digitized lane qualification tailored to tropical climates, and recyclable phase-change solutions that limit dry-ice dependence. The forecast indicates above-trend expansion as regulators tighten GDP requirements and domestic manufacturers upgrade for global supply. Recent developments focus on hybrid-powered depots, airport pharma corridors with fast-track handling, harmonized documentation flows that compress release times, and regional training programs that raise SOP consistency across multi-site networks.

Europe – Pharmaceutical Logistics Market

Europe is a mature, regulation-led market with high serialization coverage, deep specialization in controlled-temperature distribution, and strong circularity mandates influencing packaging and fleet choices. Market dynamics center on pan-regional control towers, intermodal cool-chain designs that balance speed and sustainability, and rigorous quality documentation and audits across complex, multilingual networks. Lucrative opportunities include certified low-carbon warehouse and transport solutions, reusable and pooled shipper programs, home-therapy last-mile with validated totes, and clinical trial logistics with rapid comparator sourcing and returns. Latest trends feature digital product passports, electronic consignment notes, predictive exception automation, standardized packaging pools that reduce waste, and modal shifts to rail where lanes allow. The forecast suggests steady growth supported by aging populations, specialty injectables, and hospital-to-home shifts, with capacity redeployments smoothing seasonal vaccine peaks. Recent developments highlight automated high-bay pharma campuses near major ports and airports, pilot deployments of electric and hydrogen urban fleets, expansion of ultra-low chambers for advanced therapies, and tighter cross-border data exchange that accelerates batch release and customs clearance.

Report Scope

| Parameter | Pharmaceutical Logistics Market Scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Pharmaceutical Logistics Market Segmentation

By Type

- Cold Chain Logistics

- Non-cold Chain Logistics

By Component

- Storage

- Transportation

- Monitoring components

- Software

By Procedure

- Picking

- Storage

- Retrieval Systems

- Handling Systems

By Application

- Bio Pharma

- Chemical Pharma

- Speciality Pharma

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

DHL Supply Chain, UPS Healthcare, FedEx Express, Kuehne+Nagel, DB Schenker, SF Express, CEVA Logistics, Nippon Express, Yusen Logistics, Bolloré Logistics, World Courier, Marken, Agility Logistics, United Parcel Service, DSV Panalpina

Recent Industry Developments

- July 2025 – FedEx expanded its CEIV Pharma certifications across additional global facilities, strengthening quality assurance for temperature-controlled healthcare shipments. The network upgrade enhances lane coverage for biologics and high-value therapies with standardized handling and monitoring.

- April 2025 – UPS announced a definitive agreement to acquire Andlauer Healthcare Group, adding Canadian specialty distribution and temperature-sensitive transport capabilities. The deal targets deeper cold-chain penetration and integrated services for pharma manufacturers and specialty pharmacies.

- April 2025 – DHL Group unveiled a multi-year, multi-billion-euro investment to expand Life Sciences & Healthcare logistics. The program focuses on GDP-certified sites, clinical trial support, and advanced cold-chain infrastructure for cell-and-gene and other specialty therapies.

- April 2025 – CEVA Logistics announced a new pharmaceutical logistics facility in the Strasbourg-Entzheim Airport Business Park. The site will provide GDP-compliant storage and value-added services, supporting both domestic and international healthcare flows.

- March 2025 – DHL agreed to acquire CryoPDP to deepen its time- and temperature-sensitive capabilities for biotech and pharma customers. The move broadens expertise in specialty packaging, storage, and last-mile solutions for clinical and commercial shipments.

- March 2025 – Kuehne+Nagel opened a new logistics facility in Laredo, Texas, enhancing cross-border connectivity for nearshored healthcare and medical device supply chains. The hub supports customs brokerage, cross-docking, and faster ground transit between Mexico and the U.S.

- February 2025 – UPS Healthcare launched new cross-docking facilities in Milan, Frankfurt, and Mexico City to accelerate cold-chain transits. The sites add capacity for CRT, 2–8 °C, frozen, and ULT flows with real-time visibility and rapid handoff processes.

- January 2025 – UPS completed the acquisitions of Frigo-Trans and Biotech & Pharma Logistics in Europe, expanding its specialty healthcare footprint. The integrations add GMP/GDP space, packaging services, and validated temperature-controlled transport across key corridors.

Available Customizations

The standard syndicate report is designed to serve the common interests of Pharmaceutical Logistics Market players across the value chain and include selective data and analysis from entire research findings as per the scope and price of the publication.

However, to precisely match the specific research requirements of individual clients, we offer several customization options to include the data and analysis of interest in the final deliverable.

Some of the customization requests are as mentioned below :

Segmentation of choice – Our clients can seek customization to modify/add a market division for types/applications/end-uses/processes of their choice.

Pharmaceutical Logistics Pricing and Margins Across the Supply Chain, Pharmaceutical Logistics Price Analysis / International Trade Data / Import-Export Analysis

Supply Chain Analysis, Supply–Demand Gap Analysis, PESTLE Analysis, Macro-Economic Analysis, and other Pharmaceutical Logistics market analytics

Processing and manufacturing requirements, Patent Analysis, Technology Trends, and Product Innovations

Further, the client can seek customization to break down geographies as per their requirements for specific countries/country groups such as South East Asia, Central Asia, Emerging and Developing Asia, Western Europe, Eastern Europe, Benelux, Emerging and Developing Europe, Nordic countries, North Africa, Sub-Saharan Africa, Caribbean, The Middle East and North Africa (MENA), Gulf Cooperation Council (GCC) or any other.

Capital Requirements, Income Projections, Profit Forecasts, and other parameters to prepare a detailed project report to present to Banks/Investment Agencies.

Customization of up to 10% of the content can be done without any additional charges.

Note: Latest developments will be updated in the report and delivered within 2 to 3 working days.

FAQ's

The Global Pharmaceutical Logistics Market is estimated to generate USD 121.99 billion in revenue in 2025.

The Global Pharmaceutical Logistics Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 9.44% during the forecast period from 2025 to 2034.

The Pharmaceutical Logistics Market is estimated to reach USD 274.62 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!