"The Pipeline And Process Services Market was valued at $4.9 billion in 2025 and is projected to reach $9.2 billion by 2034, growing at a CAGR of 7.3%."

Pipeline and Process Services Market Overview

The pipeline and process services market is witnessing significant growth, driven by increasing energy demand, rising investments in oil and gas infrastructure, and the need for efficient pipeline maintenance and integrity management. Pipeline and process services encompass a wide range of activities, including pre-commissioning, decommissioning, cleaning, pigging, integrity testing, and maintenance operations to ensure safe and efficient pipeline transportation. As governments and energy companies focus on minimizing environmental risks and maximizing operational efficiency, the demand for advanced pipeline services is increasing. The adoption of digital technologies, automation, and real-time monitoring systems is transforming the industry, allowing for predictive maintenance and reducing unplanned downtime. Additionally, as the global energy transition gains momentum, pipeline service providers are diversifying into hydrogen, carbon capture, and renewable energy transport infrastructure, creating new opportunities for market expansion. Despite fluctuating oil prices and regulatory pressures, the long-term demand for pipeline services remains strong, driven by the need to extend the lifespan and reliability of pipeline networks across multiple industries.

In 2024, the pipeline and process services market is experiencing rapid technological advancements, with companies increasingly investing in smart pipeline inspection and monitoring solutions. The integration of artificial intelligence (AI) and machine learning into pipeline maintenance is enhancing predictive analytics, allowing operators to detect potential failures before they occur. The adoption of robotics and autonomous inspection tools is also revolutionizing pipeline maintenance, enabling safer and more efficient operations in hazardous and remote environments. Additionally, the oil and gas sector is witnessing a surge in pipeline expansions, particularly in North America, the Middle East, and Asia-Pacific, where new transportation networks are being developed to meet growing energy needs. The market is also seeing increased adoption of inline inspection (ILI) tools, advanced leak detection technologies, and automated pigging systems to enhance pipeline efficiency and regulatory compliance. Furthermore, sustainability initiatives are gaining traction, with service providers focusing on reducing methane emissions, improving energy efficiency, and ensuring the safe transport of hydrogen and other alternative fuels. The heightened focus on ESG (Environmental, Social, and Governance) compliance is pushing companies to adopt greener solutions, leading to the development of more environmentally friendly cleaning and maintenance techniques.

Looking ahead to 2025 and beyond, the pipeline and process services market is expected to expand further with increased investments in digitalization, sustainability, and alternative energy infrastructure. AI-driven automation will continue to enhance pipeline monitoring, with cloud-based platforms enabling real-time data sharing, predictive maintenance, and remote troubleshooting. The growing shift towards hydrogen transportation and carbon capture pipelines will drive demand for specialized pipeline services designed to handle new energy carriers safely and efficiently. Additionally, regulatory frameworks will become more stringent, requiring companies to adopt best practices in leak detection, corrosion prevention, and emissions reduction. The use of blockchain technology in pipeline asset management will enhance transparency and traceability, ensuring regulatory compliance and improving supply chain efficiency. Moreover, the continued development of offshore and subsea pipeline projects will present new challenges and opportunities for service providers, particularly in deepwater energy transportation. As the industry moves toward a more resilient and environmentally conscious future, innovation and strategic partnerships will play a critical role in shaping the next phase of the pipeline and process services market.

Key Insights_ Pipeline And Process Services Market

- AI-Powered Predictive Maintenance : The integration of AI and machine learning is enabling predictive analytics for pipeline health monitoring, reducing failures, optimizing maintenance schedules, and minimizing operational risks.

- Rise of Hydrogen and Carbon Capture Pipelines : The growing focus on renewable energy and carbon reduction is driving the development of hydrogen transportation and carbon capture infrastructure, requiring specialized pipeline services.

- Increased Use of Autonomous Inspection Robotics : Robotic inspection and maintenance tools are enhancing pipeline safety, reducing human exposure to hazardous environments, and improving operational efficiency.

- Advancements in Leak Detection and Corrosion Monitoring : The adoption of fiber-optic sensors, satellite-based monitoring, and advanced coatings is improving early leak detection and preventing pipeline corrosion-related failures.

- Expansion of Digital Twin and Blockchain Technologies : Digital twin models and blockchain-based asset tracking are enhancing pipeline asset management, improving transparency, efficiency, and regulatory compliance.

- Growing Investments in Pipeline Infrastructure : Increasing global energy demand and infrastructure expansion projects are fueling investments in new pipelines and upgrades to existing networks.

- Stricter Regulatory and Environmental Compliance Requirements : Governments and regulatory bodies are enforcing stringent safety, emissions reduction, and leak prevention standards, boosting demand for advanced pipeline services.

- Adoption of Smart Monitoring and Automation : The push toward digital transformation is driving the adoption of IoT, AI, and cloud-based monitoring solutions for pipeline efficiency and risk management.

- Rising Demand for Efficient and Cost-Effective Pipeline Maintenance : Operators are investing in innovative pipeline maintenance solutions to reduce downtime, extend asset lifespan, and improve overall cost efficiency.

- High Operational Costs and Technical Complexity : Advanced pipeline maintenance and monitoring solutions require significant capital investment and technical expertise, posing challenges for small and mid-sized service providers.

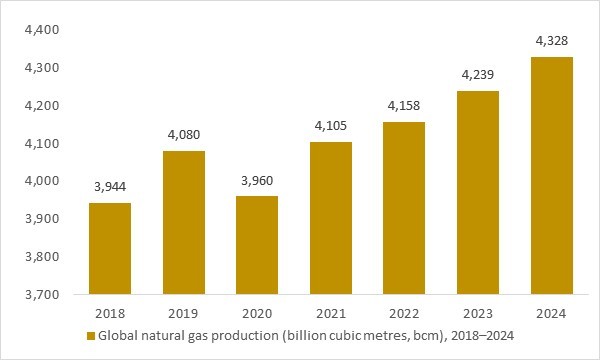

Global natural gas production (billion cubic metres, bcm), 2018–2024

Figure:Global natural gas production (bcm), 2018–2024. Rising gas output underpins long-term demand for pipeline pre-commissioning and process services across major regions.

- The steady rise in global natural gas production from 2018 to 2024 underscores the expanding need for advanced pipeline and process services across transmission, gathering and processing networks. Increasing throughput volumes drive demand for pre-commissioning, cleaning, drying, integrity verification and maintenance solutions, highlighting the critical role of specialized service providers in ensuring safe, efficient and reliable pipeline operations worldwide.

Regional Insights

North America Pipeline And Process Services Market

In North America, the pipeline and process services market is supported by a large, mature network of transmission and gathering pipelines, active offshore and onshore developments, and stringent integrity regulations. Strong upstream and midstream investment in the U.S. and Canada continues to generate demand for pre-commissioning, cleaning, drying, hydrotesting, nitrogen services, and in-line inspection, with particular focus on deepwater Gulf of Mexico projects and shale-related infrastructure. Service providers are differentiating through integrated offerings that combine engineering, pre-commissioning, maintenance and decommissioning under single project teams to manage complex, multi-asset campaigns efficiently. Digital pigging, leak detection, and data-driven integrity assessments are gaining ground as operators look to minimize downtime and comply with evolving safety standards.

Europe Pipeline And Process Services Market

Europe’s pipeline and process services market is shaped by a mix of North Sea and Mediterranean offshore assets, long-established gas transmission networks, and an accelerating transition toward lower-carbon energy. Offshore tie-backs, brownfield modifications, and life-extension projects sustain demand for pre-commissioning, flooding, cleaning, gauging, dewatering, and decommissioning services, often under stringent HSE and environmental requirements. European service providers and EPC contractors increasingly integrate pipeline services with subsea construction and topside process work, delivering bundled EPCI plus pre-commissioning scopes for major operators. Regulatory pressure on methane emissions and integrity management is encouraging wider use of intelligent pigging, advanced inspection analytics and automated leak detection, reinforcing the role of specialised PPS providers.

Asia-Pacific Pipeline And Process Services Market

Asia-Pacific is one of the fastest-growing regions for pipeline and process services, driven by rising energy demand, rapid industrialisation and heavy investment in gas pipelines and LNG-related infrastructure. Reports highlight APAC – particularly China, India, Southeast Asia and Australia – as a key growth engine, with new transmission lines, inter-regional gas links and offshore developments requiring extensive pre-commissioning, drying, nitrogen/helium leak testing and commissioning support. Local and international PPS companies are expanding presence in major hubs such as Malaysia, Singapore and the Middle East–Asia corridor, often supporting integrated EPCI projects and FPSO tie-backs. Recent contract awards for pre-commissioning campaigns offshore Malaysia and in regional deepwater projects illustrate growing reliance on specialised providers to manage complex subsea and export pipelines under tight schedules.

Rest of the World Pipeline And Process Services Market

In the rest of the world, including Latin America, the Middle East and Africa, the pipeline and process services market is closely linked to large-scale oil and gas developments and export infrastructure. National oil companies and IOCs are investing in offshore trunklines, onshore gathering systems and export pipelines that require integrated EPCI plus pre-commissioning, hook-up and commissioning services. The Middle East, in particular, combines extensive existing pipeline grids with new gas, petrochemical and carbon-capture projects, supporting ongoing demand for cleaning, hydrotesting, nitrogen purging and process plant commissioning. In Africa and Latin America, subsea tie-backs and new field developments are creating pockets of opportunity for PPS specialists as part of broader subsea and topside packages, with safety, local-content development and schedule certainty key success factors.

Market Scope

| Parameter | Pipeline And Process Services Market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Pipeline And Process Services Market Segmentation

By Operation

- Pre-Commissioning And Commissioning

- Maintenance

- Decommissioning

By Asset Type

- Pipeline

- Process

By Raw Material

- Plastic

- Carbon Steel

- Steel

By End-Users

- Oil And Gas Industry

- Chemical Industry

- Water Treatment Industry

- Construction And Manufacturing Industry

- Other By End-Users

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Major Companies Analysed

Halliburton Company, Baker Hughes Company, EnerMech Ltd., IKM Gruppen AS, Altus Intervention, Ideh Pouyan Energy Co, Trans Asia Pipeline Services, Techfem Spa, Enerpac Tool Group, STEP Energy Services, Chenergy Services Limited, CR Asia Group, Eunisell Limited, Alphaden Energy and Oilfield Limited, Cypress Pipeline & Process Services, Hydratight, Blue Fin Group, Tucker Energy Services, IPEC Ltd., Barnard Construction Company Inc., Sunland Construction Inc., Snelson Companies Inc., STATS Group, Intertek Group plc, Oil States Industries Inc., T.D. Williamson, MISTRAS Group Inc., Shawcor Ltd., Schlumberger Limited, Weatherford International

FAQ's

The Global Pipeline And Process Services Market is estimated to generate USD 4.9 billion in revenue in 2025.

The Global Pipeline And Process Services Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 7.25% during the forecast period from 2025 to 2034.

The Pipeline And Process Services Market is estimated to reach USD 9.2 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!