"The Point of Sale Terminal Market was valued at $ 98.18 billion in 2026 and is projected to reach $ 199.11 billion by 2034, growing at a CAGR of 9.24%."

The Point of Sale (POS) terminal market encompasses the hardware, software, and payment services that enable merchants to accept and reconcile transactions across brick-and-mortar and omnichannel environments. Modern POS has evolved from fixed countertop systems to a spectrum that includes Android all-in-ones, handheld and mobile POS, self-checkout, kiosks, and softPOS on commercial smartphones. Demand is propelled by rapid migration to digital and contactless payments, integration of wallets and QR, and the need to unify in-store and online journeys with a single commerce platform. Retail, hospitality, quick-service restaurants, healthcare, fuel, transportation, and entertainment are core adopters, with small merchants onboarding via app-first, subscription models while large enterprises standardize globally on cloud POS stacks. Regulatory pushes around EMV, fiscalization, and e-invoicing, along with tax compliance and auditability, accelerate refresh cycles. Vendors differentiate through inventory, CRM, loyalty, and analytics add-ons, while acquirers and fintechs bundle terminals with payments to reduce total cost of ownership. Post-pandemic shifts to curbside, order-ahead, and pay-at-table remain durable, anchoring investment in resilient, offline-capable systems and secure, tokenized payment flows.

The market’s technology agenda centers on cloud orchestration, edge processing for speed and resilience, and tighter integration with ERP, OMS, and ecommerce. Android POS, modular peripherals, and developer-friendly APIs shorten rollout times and enable rapid creation of vertical features such as table management, kitchen display systems, menu engineering, patient billing, and ticketing. Connectivity advances (NFC, Bluetooth, Wi-Fi 6, 4G/5G) and battery efficiency extend mobility for line-busting and delivery use cases. Security is prioritized via PCI DSS, P2PE, tokenization, encryption at rest, and device attestation, while AI augments fraud detection, forecasting, and personalized offers at checkout. Emerging markets expand through micro-merchant onboarding, government digitization programs, and support for local real-time payment rails. Sustainability considerations influence hardware lifecycles, repairability, and energy use. Competitive dynamics span terminal OEMs, payment processors, ISVs, and cloud POS providers, with “payments-as-a-service” bundles reshaping procurement. Key challenges include fragmented regulations, multi-country certification, latency and uptime for omnichannel sync, and continuous patching. Overall, POS terminals are becoming commerce hubs that converge payments, operations, and customer engagement into a single, data-rich platform.

Trade Intelligence Of Point of Sale (POS) Terminal Market

| Global Parts and accessories equally suitable for use with machines, Imports, USD million, 2020-24 | |||||

|

| 2020 | 2021 | 2022 | 2023 | 2024 |

| World | 10,299 | 11,615 | 12,283 | 11,397 | 11,082 |

| United States of America | 1,729 | 2,174 | 2,634 | 2,105 | 2,088 |

| Germany | 961 | 991 | 1,043 | 1,053 | 1,025 |

| Netherlands | 1,032 | 1,030 | 981 | 837 | 863 |

| China | 779 | 838 | 680 | 520 | 484 |

| Japan | 503 | 470 | 544 | 502 | 480 |

| Source: OGAnalysis, (ITC) | |||||

- United States of America, Germany, Netherlands, China and Japan are the top five countries importing 44.6% of global Parts and accessories equally suitable for use with machines in 2024

- Global Parts and accessories equally suitable for use with machines Imports increased by 7.6% between 2020 and 2024

- United States of America accounts for 18.8% of global Parts and accessories equally suitable for use with machines trade in 2024

- Germany accounts for 9.2% of global Parts and accessories equally suitable for use with machines trade in 2024

- Netherlands accounts for 7.8% of global Parts and accessories equally suitable for use with machines trade in 2024

| Global Parts and accessories equally suitable for use with machines Export Prices, USD/Ton, 2020-24 |

|

|

| Source: OGAnalysis |

Regional Insights

North America Point of Sale Terminal Market

The North American Point of Sale terminal market is shaped by rapid migration to contactless payments, cloud-managed POS, and tight integration with ecommerce, loyalty, and inventory systems. Market dynamics favor platform vendors that can unify countertop, handheld, self-checkout, and kiosks under centralized device management and analytics. Lucrative opportunities exist in grocery, fuel and convenience, quick-service restaurants, healthcare, and stadiums seeking queue-busting mobility and resilient offline capabilities. Latest trends include softPOS enablement on commercial smartphones, tap-to-pay expansion, pay-at-table, and AI-driven personalization and loss prevention at checkout. The forecast points to sustained replacement cycles as PCI updates, tokenization, and P2PE requirements intersect with enterprise rollouts of omnichannel features like BOPIS and curbside. Recent developments emphasize Wi-Fi 6 and 5G connectivity, Android-first hardware, and partnerships between processors, ISVs, and retailers to deliver configurable, subscription-based bundles that lower total cost of ownership.

Asia Pacific Point of Sale Terminal Market

Asia Pacific’s POS terminal market is propelled by explosive digital payment adoption across super-app ecosystems, QR acceptance, and government-backed real-time rails. Market dynamics favor agile vendors that localize for diverse tax rules, languages, and payment schemes while scaling through channel partners to reach micro and small merchants. Opportunities are strongest in modernizing SMB retail, food delivery and mobility commerce, travel and entertainment, and cross-border tourism corridors. Key trends include Android all-in-ones, mPOS for gig and field services, and fiscal-compliant e-receipting and e-invoicing, alongside AI for demand forecasting and fraud analytics. The forecast underscores outsized growth for mobile and unattended formats in convenience, transit, and vending as connectivity and battery efficiency improve. Latest developments highlight softPOS pilots moving to production, expanded acceptance of domestic wallets and real-time transfers at the point of interaction, and cloud orchestration that syncs catalog, pricing, and loyalty across marketplaces and stores.

Europe Point of Sale Terminal Market

Europe’s POS terminal market is anchored by stringent security and privacy regimes, evolving fiscalization and e-invoicing mandates, and strong card and contactless penetration. Market dynamics reward providers that deliver certified devices, robust remote key injection, and seamless SCA-compliant flows while supporting regional wallets and instant payment schemes. Attractive opportunities lie in specialty retail modernization, hospitality self-service, public transport ticketing, and pharmacy and healthcare checkout digitization. Trends include accelerated rollouts of self-checkout, kiosks for order-ahead, softPOS for pop-up and seasonal retail, and sustainability-focused hardware with modular repairability. The forecast anticipates continued consolidation toward cloud POS and managed services, with analytics and real-time inventory visibility becoming standard across multi-country operations. Recent developments center on Android migration, device attestation, tokenization at scale, and partnerships between acquirers, ISVs, and large merchants to deliver unified commerce capabilities with consistent pricing, promotions, and loyalty across channels.

Key Market Insights

-

The Point of Sale terminal market is increasingly driven by the accelerated adoption of digital and contactless payments, especially in retail, hospitality, and quick-service restaurants. Businesses are shifting toward cashless ecosystems, fueled by customer demand for speed, hygiene, and convenience. This is pushing vendors to upgrade hardware and software to support QR codes, NFC, EMV standards, and mobile wallets, positioning POS terminals as key enablers of seamless consumer experiences.

-

Cloud-based POS systems are reshaping the industry by offering scalability, centralized data management, and real-time integration across multiple store locations. Retail chains, franchises, and small businesses are deploying cloud POS to enhance operational efficiency and reduce upfront investment. This shift supports omnichannel strategies, where online and offline transactions converge into unified customer and inventory management systems, ensuring consistency across sales channels.

-

Mobile POS (mPOS) adoption is gaining momentum among small and medium-sized enterprises, delivery services, and field businesses. Lightweight, app-driven systems allow merchants to accept payments anytime and anywhere, reducing infrastructure costs. The affordability and subscription-based models provided by fintechs make POS solutions accessible to micro-merchants, driving financial inclusion and expanding the addressable market for service providers.

-

Integration of POS with analytics, CRM, and loyalty programs is turning terminals into multifunctional business tools. Beyond processing payments, POS solutions now enable inventory tracking, customer insights, personalized offers, and marketing campaigns. This transformation strengthens customer engagement, improves sales forecasting, and helps businesses refine promotional strategies, enhancing the role of POS in long-term business intelligence.

-

Security and compliance are critical drivers of market demand, with emphasis on data protection, encryption, and regulatory standards like PCI DSS. Rising cyberattacks and fraud incidents make security features a top priority for businesses. Tokenization, point-to-point encryption, and biometric authentication are increasingly embedded into POS systems to build trust and comply with evolving international and regional regulatory frameworks.

-

The rise of self-service and unattended POS systems, including kiosks and self-checkout counters, is reshaping consumer behavior in retail, quick-service restaurants, and transportation. Automation reduces queues, lowers labor costs, and enhances customer autonomy. These systems are increasingly integrated with AI to enable personalized upselling and voice or gesture recognition, making them vital to future customer experience strategies.

-

Regional dynamics play a major role in market expansion. In North America and Europe, advanced compliance regulations and card penetration dominate trends, while Asia-Pacific is seeing rapid adoption through smartphone-driven POS and government-backed digitalization initiatives. Latin America and Africa are experiencing strong growth from micro-merchant onboarding and financial inclusion efforts, supported by partnerships with fintech firms and local payment providers.

-

The role of POS terminals in omnichannel retailing is becoming indispensable. Businesses rely on integrated systems to synchronize inventory, promotions, and pricing across online platforms, physical stores, and mobile applications. This creates a consistent shopping experience and supports hybrid models such as buy-online-pickup-in-store (BOPIS) and order-ahead for restaurants, further broadening the scope of POS deployment.

-

Artificial intelligence and machine learning are being embedded in POS terminals for predictive analytics, fraud detection, and real-time customer insights. AI-powered POS systems help optimize product placement, improve sales conversion, and deliver personalized promotions at checkout. These capabilities make POS not just a transactional tool but a decision-making engine for merchants, reshaping competitive strategies in retail and hospitality.

-

Sustainability and lifecycle management are emerging considerations for POS hardware design. Businesses are demanding energy-efficient terminals, recyclable components, and longer device lifespans to align with ESG goals. Manufacturers are responding with modular, repairable systems that reduce e-waste, while software-led upgrades ensure devices remain relevant without frequent hardware replacements, supporting cost savings and sustainable operations.

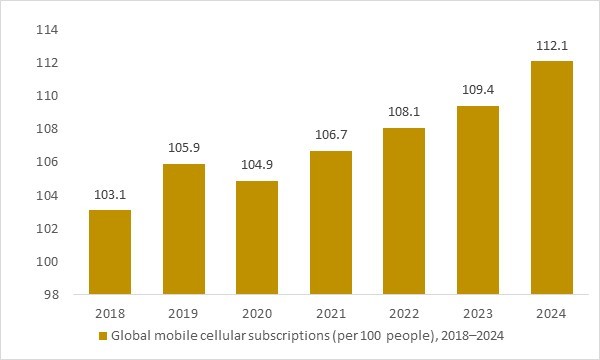

Global mobile cellular subscriptions (per 100 people), 2018–2024

Figure: Global mobile cellular subscriptions increased from about 103 subscriptions per 100 people in 2018 to an estimated 112 subscriptions per 100 people in 2024, reflecting the expanding connectivity base that supports digital payments and POS terminal deployment. As mobile penetration deepens across both developed and emerging economies, merchants increasingly adopt mPOS, softPOS and QR-based acceptance models that rely on smartphone and network availability. OG Analysis estimates, derived from World Bank mobile connectivity indicators and global digital commerce studies, illustrate how rising mobile subscription density strengthens long-term POS rollout, merchant onboarding and transaction digitization across retail and service sectors.

Global mobile cellular subscription density increased from about 103 subscriptions per 100 people in 2018 to roughly 112 per 100 people in 2024, highlighting steady expansion of worldwide mobile connectivity. This growth underpins the rapid adoption of mPOS, softPOS and QR-based payment solutions that rely on smartphone and network access. Rising mobile penetration lowers entry barriers for small merchants and accelerates POS terminal deployment across emerging and developed markets. Overall, the connectivity trend supports sustained transaction digitization and replacement demand in the point of sale terminal market.

Report Scope

| Parameter | Point of Sale (POS) Terminal Market scope Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2027-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Point of Sale Terminal Market Segmention

By Product

- Mobile

- Fixed

By Component

- Hardware

- Software

- Service

By Technology

- Biometric

- Traditional

By Operating System

- Windows

- Linux

- MAC

By Application

- Restaurants

- Hospitality

- Healthcare

- Retail

- Warehouse

- Entertainment

- Other Applications

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

Samsung Electronics Co. Ltd., NEC Corporation, Panasonic Corporation, Toshiba Corporation, Hewlett-Packard Development Company L. P., VeriFone Systems Inc., Qashier PTE Ltd., Newland Payment Technology, GK Software SE, PAX Technology Limited, Casio Computer Co. Ltd., iMetrics Pte Ltd, Acrelec Group SAS, AURES Technologies SA, HM Electronics Inc., NCR Corporation, Oracle Corporation, Presto Group LLC, Qu Inc., Quail Digital Limited, Revel Systems Inc., Toast Inc., TouchBistro Inc., Xenial Inc., Aireus Inc., Dinerware Inc., Posist Technologies Private Limited, Ingenico Group S. A., BBPOS Limited, Honeywell International Inc.

Recent Industry Developments

April 2025 – Global Payments announced a major strategic move to acquire Worldpay for over $22 billion (cash and stock), significantly expanding its global transaction capacity and merchant reach.

May 2025 – Square unveiled its Square Handheld device, a sleek, ultra-mobile POS that combines tap-to-pay, barcode scanning, inventory tools, and a 6.2-inch touchscreen into an 11-ounce form factor.

May 2025 – Global Payments launched its unified Genius™ POS platform, aiming to consolidate multiple legacy systems into one scalable solution tailored for restaurants, retail, and enterprise environments.

July 2025 – Global Payments introduced softPOS capability within its Genius platform, enabling merchants to accept contactless payments directly through mobile devices without additional hardware.

FAQ's

The Global Point of Sale Terminal Market is estimated to generate $ 98.18 billion in revenue in 2026.

The Global Point of Sale Terminal Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 9.24% during the forecast period from 2026 to 2034.

The Point of Sale Terminal Market is estimated to reach $ 199.11 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!