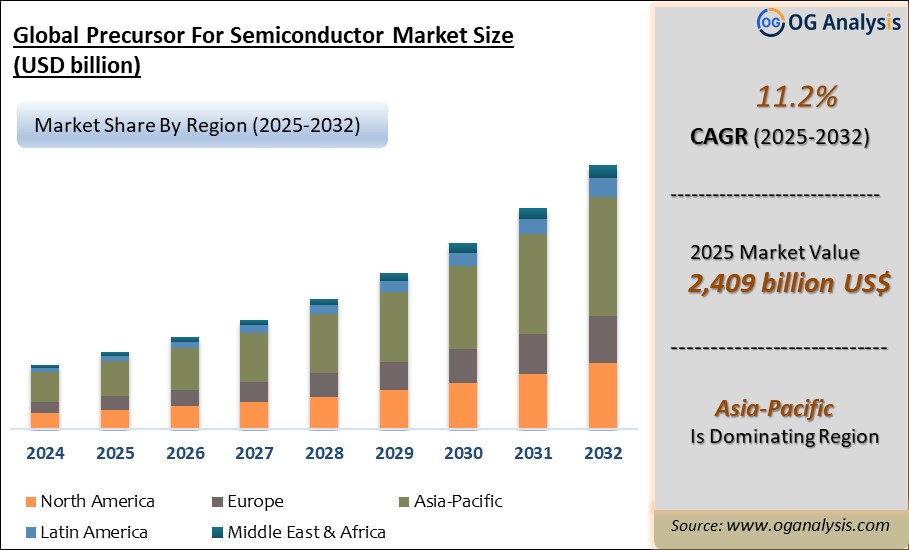

"The Global Precursor for Semiconductor Market valued at USD 2,167. Million in 2024, is expected to grow by 11.2% CAGR to reach market size worth USD 6,396.4 Million by 2034."

The precursor for semiconductor market is an essential pillar of the broader electronics manufacturing ecosystem, delivering high-purity materials vital for semiconductor chip production. These precursors serve as the building blocks in deposition processes like chemical vapor deposition (CVD) and atomic layer deposition (ALD), essential for creating nanoscale features on advanced chips. 2024 has seen major strides in the market as key players have expanded their production capabilities to meet increasing demand from industries reliant on semiconductors, such as automotive, consumer electronics, and telecommunications. These expansions reflect the growing importance of reliable precursor supply chains as the world becomes increasingly digitized.

Looking ahead to 2025, the precursor market is expected to experience robust growth, driven by innovations in semiconductor technologies such as 3D chip architectures and advanced packaging solutions. Companies are investing heavily in research and development to enhance the purity and performance of precursors to enable the creation of more complex and efficient chips. This market expansion is poised to support the continued rollout of next-generation technologies, including AI-driven automation and quantum computing, placing the semiconductor industry at the forefront of global economic growth.

The Global Precursor for Semiconductor Market Analysis Report will provide a comprehensive assessment of business dynamics, offering detailed insights into how companies can navigate the evolving landscape to maximize their market potential through 2034. This analysis will be crucial for stakeholders aiming to align with the latest industry trends and capitalize on emerging market opportunities.

Asia-Pacific is the leading region in the Precursor for Semiconductor Market, fueled by a strong semiconductor manufacturing base, substantial investments in advanced fabrication technologies, and other key driving factors.

Precursor for Semiconductor Market Strategy, Price Trends, Drivers, Challenges and Opportunities to 2034

In terms of market strategy, price trends, drivers, challenges, and opportunities from2025 to 2034, Precursor for Semiconductor market players are directing investments toward acquiring new technologies, securing raw materials through efficient procurement and inventory management, enhancing product portfolios, and leveraging capabilities to sustain growth amidst challenging conditions. Regional-specific strategies are being emphasized due to highly varying economic and social challenges across countries.

Factors such as global economic slowdown, the impact of geopolitical tensions, delayed growth in specific regions, and the risks of stagflation necessitate a vigilant and forward-looking approach among Precursor for Semiconductor industry players. Adaptations in supply chain dynamics and the growing emphasis on cleaner and sustainable practices further drive strategic shifts within companies.

The market study delivers a comprehensive overview of current trends and developments in the Precursor for Semiconductor industry, complemented by detailed descriptive and prescriptive analyses for insights into the market landscape until 2034.

North America Precursor for Semiconductor Market Analysis

The North America Precursor for Semiconductor market showcased robust advancements in 2024, driven by the region's rapid adoption of advanced electronic and semiconductor technologies across industries such as defense, telecommunications, and industrial automation. Key developments included increased investments in radiation-hardened electronics, the proliferation of intelligent power distribution units, and advancements in programmable logic controllers (PLCs) tailored for Industry 4.0 applications. Anticipated Precursor for Semiconductor growth from 2025 is fueled by burgeoning demand for semiconductor materials and components, coupled with strong R&D initiatives. The region's competitive landscape is characterized by dominant players leveraging innovative designs, strategic acquisitions, and collaborations to secure supply chain resilience and penetrate high-growth sectors, including aerospace and renewable energy.

Europe Precursor for Semiconductor Market Outlook

In 2024, the European Precursor for Semiconductor market experienced significant growth, underpinned by a surge in demand for silicon-based semiconductor solutions and sustainable electronics. The Precursor for Semiconductor market was bolstered by advancements in next-generation products, expected to cater to the automotive and industrial sectors’ growing needs for precision and efficiency. From 2025, growth is anticipated to accelerate due to the region's commitment to green technologies and the expansion of intelligent power and control systems. Precursor for Semiconductor competitive landscape defined by established regional players and a surge of local startups focuses on innovation in systems and biosensors, aligning with Europe’s stringent environmental and safety regulations.

Asia-Pacific Precursor for Semiconductor Market Forecast

Asia-Pacific led the global Precursor for Semiconductor market in 2024, driven by the rapid expansion of consumer electronics, telecommunications, and semiconductor manufacturing. Key developments included the widespread deployment of advanced SCARA robots and sensor fusion technologies in industrial applications. The region's leadership in semiconductor foundry and fabrication further solidified its dominance, supported by government incentives and private sector investments. Growth from 2025 is expected to be propelled by rising demand for precision products across smart cities and energy management projects. The competitive landscape is shaped by a mix of global giants and agile local firms, leveraging economies of scale and innovation hubs in countries like China, Japan, and South Korea.

Middle East, Africa, Latin America Precursor for Semiconductor Market Overview

In 2024, the Precursor for Semiconductor market across the Rest of the World demonstrated steady progress, particularly in emerging economies embracing advanced semiconductor applications in infrastructure and security. Key developments centered on the adoption of biosensors and radiation detection devices in healthcare and energy sectors. Growth from 2025 is anticipated to stem from increasing investments in semiconductor intellectual property (IP) and SCADA systems to support industrial modernization and energy distribution. The competitive landscape is marked by the entry of new players targeting niche applications, while established firms focus on partnerships and localized manufacturing to tap into underserved markets in the Middle East, Africa, and South America.

Precursor for Semiconductor Market Dynamics and Future Analytics

The research analyses the Precursor for Semiconductor parent market, derived market, intermediaries’ market, raw material market, and substitute market are all evaluated to better prospect the Precursor for Semiconductor market outlook. Geopolitical analysis, demographic analysis, and Porter’s five forces analysis are prudently assessed to estimate the best Precursor for Semiconductor market projections.

Recent deals and developments are considered for their potential impact on Precursor for Semiconductor's future business. Other metrics analyzed include the Threat of New Entrants, Threat of New Substitutes, Product Differentiation, Degree of Competition, Number of Suppliers, Distribution Channel, Capital Needed, Entry Barriers, Govt. Regulations, Beneficial Alternative, and Cost of Substitute in Precursor for Semiconductor market.

Precursor for Semiconductor trade and price analysis helps comprehend Precursor for Semiconductor's international market scenario with top exporters/suppliers and top importers/customer information. The data and analysis assist our clients in planning procurement, identifying potential vendors/clients to associate with, understanding Precursor for Semiconductor price trends and patterns, and exploring new Precursor for Semiconductor sales channels. The research will be updated to the latest month to include the impact of the latest developments such as the Russia-Ukraine war on the Precursor for Semiconductor market.

Precursor for Semiconductor Market Structure, Competitive Intelligence and Key Winning Strategies

The report presents detailed profiles of top companies operating in the Precursor for Semiconductor market and players serving the Precursor for Semiconductor value chain along with their strategies for the near, medium, and long term period.

OGAnalysis’ proprietary company revenue and product analysis model unveils the Precursor for Semiconductor market structure and competitive landscape. Company profiles of key players with a business description, product portfolio, SWOT analysis, Financial Analysis, and key strategies are covered in the report. It identifies top-performing Precursor for Semiconductor products in global and regional markets. New Product Launches, Investment & Funding updates, Mergers & Acquisitions, Collaboration & Partnership, Awards and Agreements, Expansion, and other developments give our clients the Precursor for Semiconductor market update to stay ahead of the competition.

Company offerings in different segments across Asia-Pacific, Europe, the Middle East, Africa, and South and Central America are presented to better understand the company strategy for the Precursor for Semiconductor market. The competition analysis enables users to assess competitor strategies and helps align their capabilities and resources for future growth prospects to improve their market share.

Precursor for Semiconductor Market Research Scope

• Global Precursor for Semiconductor market size and growth projections (CAGR), 2024- 2034

• Policies of USA New President Trump, Russia-Ukraine War, Israel-Palestine, Middle East Tensions Impact on the Precursor for Semiconductor Trade and Supply-chain

• Precursor for Semiconductor market size, share, and outlook across 5 regions and 27 countries, 2023- 2034

• Precursor for Semiconductor market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2023- 2034

• Short and long-term Precursor for Semiconductor market trends, drivers, restraints, and opportunities

• Porter’s Five Forces analysis, Technological developments in the Precursor for Semiconductor market, Precursor for Semiconductor supply chain analysis

• Precursor for Semiconductor trade analysis, Precursor for Semiconductor market price analysis, Precursor for Semiconductor supply/demand

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products

• Latest Precursor for Semiconductor market news and developments

The Precursor for Semiconductor Market international scenario is well established in the report with separate chapters on North America Precursor for Semiconductor Market, Europe Precursor for Semiconductor Market, Asia-Pacific Precursor for Semiconductor Market, Middle East and Africa Precursor for Semiconductor Market, and South and Central America Precursor for Semiconductor Markets. These sections further fragment the regional Precursor for Semiconductor market by type, application, end-user, and country.

Market Scope

| Parameter | Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, and By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Regional Insights

North America Precursor for Semiconductor market data and outlook to 2034

United States

Canada

Mexico

Europe Precursor for Semiconductor market data and outlook to 2034

Germany

United Kingdom

France

Italy

Spain

BeNeLux

Russia

Asia-Pacific Precursor for Semiconductor market data and outlook to 2034

China

Japan

India

South Korea

Australia

Indonesia

Malaysia

Vietnam

Middle East and Africa Precursor for Semiconductor market data and outlook to 2034

Saudi Arabia

South Africa

Iran

UAE

Egypt

South and Central America Precursor for Semiconductor market data and outlook to 2034

Brazil

Argentina

Chile

Peru

* We can include data and analysis of additional coutries on demand

Who can benefit from this research

The research would help top management/strategy formulators/business/product development/sales managers and investors in this market in the following ways

1. The report provides 2024 Precursor for Semiconductor market sales data at the global, regional, and key country levels with a detailed outlook to 2034 allowing companies to calculate their market share and analyze prospects, uncover new markets, and plan market entry strategy.

2. The research includes the Precursor for Semiconductor market split into different types and applications. This segmentation helps managers plan their products and budgets based on the future growth rates of each segment

3. The Precursor for Semiconductor market study helps stakeholders understand the breadth and stance of the market giving them information on key drivers, restraints, challenges, and growth opportunities of the market and mitigating risks

4. This report would help top management understand competition better with a detailed SWOT analysis and key strategies of their competitors, and plan their position in the business

5. The study assists investors in analyzing Precursor for Semiconductor business prospects by region, key countries, and top companies' information to channel their investments.

Available Customizations

The standard syndicate report is designed to serve the common interests of Precursor for Semiconductor Market players across the value chain and include selective data and analysis from entire research findings as per the scope and price of the publication.

However, to precisely match the specific research requirements of individual clients, we offer several customization options to include the data and analysis of interest in the final deliverable.

Some of the customization requests are as mentioned below –

Segmentation of choice – Our clients can seek customization to modify/add a market division for types/applications/end-uses/processes of their choice.

Precursor for Semiconductor Pricing and Margins Across the Supply Chain, Precursor for Semiconductor Price Analysis / International Trade Data / Import-Export Analysis,

Supply Chain Analysis, Supply – Demand Gap Analysis, PESTLE Analysis, Macro-Economic Analysis, and other Precursor for Semiconductor market analytics

Processing and manufacturing requirements, Patent Analysis, Technology Trends, and Product Innovations

Further, the client can seek customization to break down geographies as per their requirements for specific countries/country groups such as South East Asia, Central Asia, Emerging and Developing Asia, Western Europe, Eastern Europe, Benelux, Emerging and Developing Europe, Nordic countries, North Africa, Sub-Saharan Africa, Caribbean, The Middle East and North Africa (MENA), Gulf Cooperation Council (GCC) or any other.

Capital Requirements, Income Projections, Profit Forecasts, and other parameters to prepare a detailed project report to present to Banks/Investment Agencies.

Customization of up to 10% of the content can be done without any additional charges.

Note Latest developments will be updated in the report and delivered within 2 to 3 working days

Precursor For Semiconductor Market Segmentation

by Product Type

- Analog Semiconductors

- Digital Semiconductors

- Mixed-Signal Semiconductors

- Optoelectronics

- Discrete Semiconductors

by Technology

- Wafer Fabrication

- Packaging Technologies

- 3D ICs

- System-on-Chip (SoC) Technology

- Power Semiconductors

by Material Type

- Silicon

- Gallium Nitride (GaN)

- Silicon Carbide (SiC)

- Flexible Materials

- Additive Manufacturing Materials

by End User

- Original Equipment Manufacturers (OEMs)

- Electronic Manufacturing Services (EMS)

- Semi-conductor Foundries

- Research and Development Units

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

-

Merck

-

Air Liquide

-

SK Materials

-

UP Chemical

-

Entegris

-

ADEKA

-

Hansol Chemical

-

DuPont

-

SoulBrain

-

Nanmat

-

DNF Solutions

-

Natachem

-

Tanaka Kikinzoku

-

Botai Electronic Material

-

Gelest

-

Strem Chemicals

-

Anhui Adchem

-

EpiValence

-

FUJIFILM

FAQ's

The Precursor for Semiconductor Market is estimated to reach USD 6,396.4 Million by 2034.

The Global Precursor for Semiconductor Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 11.2% during the forecast period from 2025 to 2034.

The Global Precursor for Semiconductor Market is estimated to generate USD 2,385.6 Million in revenue in 2025

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!