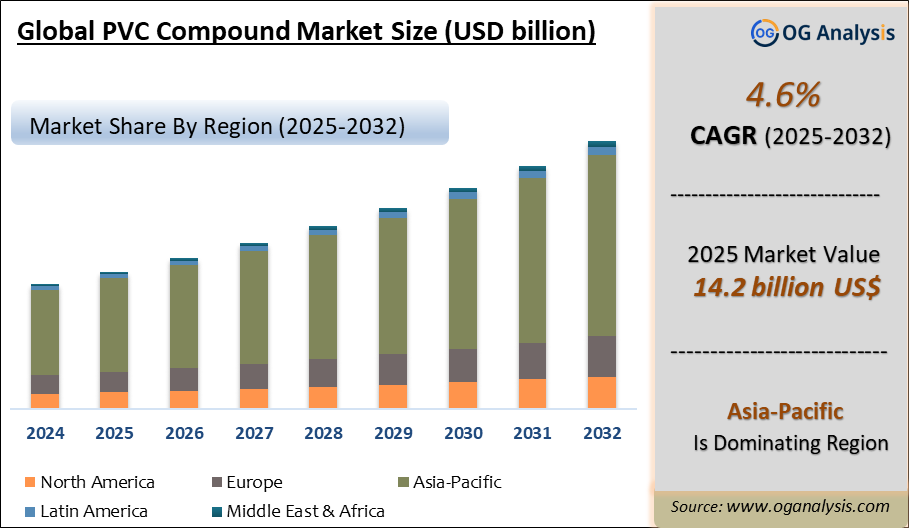

""The Global PVC Compound Market valued at USD 13.6 Billion in 2024, is expected to grow by 4.6% CAGR to reach market size worth USD 21.8 Billion by 2034.""

The PVC (Polyvinyl Chloride) Compound Market is witnessing a transformative phase, driven by significant advancements in manufacturing technologies and increasing demand for sustainable materials across various industries. In 2024, the market has seen a surge in the adoption of eco-friendly practices, with manufacturers focusing on developing greener PVC formulations that minimize environmental impact. This shift aligns with global initiatives promoting sustainability and responsible consumption. Key developments include the introduction of bio-based PVC compounds and the integration of recycling technologies that enhance the lifecycle of PVC products. Additionally, the emergence of innovative applications in the construction, automotive, and packaging sectors is further propelling market growth.

As we look towards 2025, the PVC Compound Market is poised for continued expansion, fueled by increasing urbanization and infrastructure development. The demand for lightweight, durable materials in the automotive and construction sectors is expected to rise, enhancing the applications of PVC compounds. Furthermore, advancements in polymerization processes and compounding techniques will enable the creation of customized compounds tailored to specific industry needs. These developments will not only improve product performance but also contribute to cost efficiencies, driving the adoption of PVC compounds in diverse applications. The focus on sustainability and innovation is set to redefine the landscape of the PVC Compound Market in the coming years.

The Global PVC Compound Market Analysis Report will provide a comprehensive assessment of business dynamics, offering detailed insights into how companies can navigate the evolving landscape to maximize their market potential through 2034. This analysis will be crucial for stakeholders aiming to align with the latest industry trends and capitalize on emerging market opportunities.

Trade Intelligence for pvc compound Market

| Global Plasticised poly vinyl chloride Trade, Imports, USD million, 2020-24 | |||||

|

| 2020 | 2021 | 2022 | 2023 | 2024 |

| World | 1,820 | 2,514 | 2,666 | 2,141 | 2,191 |

| Mexico | 204 | 218 | 248 | 253 | 231 |

| Viet Nam | 92.03 | 112 | 120 | 78.50 | 119 |

| China | 135 | 145 | 139 | 102 | 106 |

| Poland | 72.08 | 111 | 122 | 104 | 96.35 |

| Germany | 69.81 | 102 | 102 | 93.99 | 82.86 |

| Source: OGAnalysis | |||||

- Mexico, Viet Nam, China, Poland and Germany are the top five countries importing 29.1% of global Plasticised poly vinyl chloride in 2024

- Global Plasticised poly vinyl chloride Imports increased by 20.4% between 2020 and 2024

- Mexico accounts for 10.6% of global Plasticised poly vinyl chloride trade in 2024

- VietNam accounts for 5.5% of global Plasticised poly vinyl chloride trade in 2024

- China accounts for 4.9% of global Plasticised poly vinyl chloride trade in 2024

| Global Plasticised poly vinyl chloride Export Prices, USD/Ton, 2020-24 |

| |

| Source: OGAnalysis |

PVC Compound Market Key Insights

- The PVC compound market is expanding due to its versatility, cost-efficiency, and performance, serving industries such as construction, automotive, healthcare, electronics, and packaging. Formulations can be tailored for impact resistance, weatherability, flexibility, and clarity, making PVC compounds a go-to material for complex application needs.

- Regulatory compliance and sustainability are reshaping formulations, with growing demand for low-VOC, heavy metal-free, and phthalate-free PVC compounds. Manufacturers are pivoting toward bio-based plasticizers, recycled content, and non-toxic stabilizers to align with stringent environmental and health standards in global markets.

- The construction sector remains a robust driver for PVC compounds—particularly in applications like pipes, window profiles, siding, roofing membranes, and flooring. Demand is boosted by infrastructure growth, urbanization, and a heightened focus on long-lasting, low-maintenance building materials.

- In automotive, lightweighting and enhanced safety demands are fueling the use of PVC compounds in interior components, electrical cable jacketing, under-the-hood parts, and soft-touch surfaces. Flame-retardant and low-smoke formulations help meet standards while balancing aesthetics, durability, and weight savings.

- The healthcare segment is adopting medical-grade PVC compounds for tubing, blood bags, catheter components, and flexible packaging, relying on the material’s clarity, sterilization tolerance, and cost-effectiveness. Regulatory emphasis on biocompatibility and extractables is driving further refinement of medical-specific formulations.

- The electronics and cable sector is using PVC compounds for wire insulation, jacket sheaths, and cable compounds due to their dielectric reliability, flame retardance, and processability. There is increasing interest in halogen-free alternatives to improve fire safety and meet green building codes.

- Processing innovations such as twin-screw compounding, nanofiller integration, and reactive extrusion are enhancing dispersion, stability, and performance of PVC compounds. These methods help reduce additive usage, improve homogeneity, and support high-throughput manufacturing while maintaining product integrity.

- Color, masterbatch, and additive integration services are differentiating compound suppliers by offering turnkey customized solutions. Shared R&D platforms enable rapid development of application-specific grades, such as UV-stable outdoor PVC, microcellular foamed profiles, and thermoformable sheets.

- Geographically, Asia-Pacific is the fastest-growing PVC compound market driven by construction booms, grid expansion, and rising manufacturing bases. Growth is propelled by affordable labor, expanding compounding infrastructure, and a growing focus on localized supply chains.

- Supply chain volatility—especially in raw materials like vinyl chloride monomer, plasticizers, and stabilizers—is prompting manufacturers to adopt dual sourcing, backward integration, and inventory optimization strategies. Flexible recipe frameworks that can accommodate feedstock shifts are increasingly valued in managing cost and availability risks.

North America PVC Compound Market Analysis

The North America PVC Compound market demonstrated robust growth in 2024, driven by advancements in eco-friendly materials, regulatory shifts favoring sustainable production, and increased investments in R&D. Chemicals and Materials markets such as bio-based polymers, adhesives and sealants, and paints and coatings additives saw significant traction, spurred by strong demand from construction, automotive, and packaging sectors. The anticipated PVC Compound industry growth in 2025 is underpinned by heightened focus on green building materials, innovative self-healing materials, and expansion of end-user industries such as electronics and aerospace. Competitive dynamics reflect increasing collaboration between key players and technology providers, with a focus on sustainable innovation and scaling advanced manufacturing technologies. Major players are leveraging partnerships and acquisitions to address regulatory standards and expand their market presence, creating an intensely competitive landscape.

Europe PVC Compound Market Outlook

The European PVC Compound market maintained a steady growth trajectory in 2024, bolstered by stringent environmental regulations and the growing adoption of circular economy principles. High demand for specialty chemicals and bio-based polymers was observed due to infrastructure projects and the push for green building initiatives. From 2025 onward, growth is expected to accelerate with innovations in materials catering to advanced applications in pharmaceuticals, cosmetics, and industrial coatings. The region’s leadership in sustainable technologies and commitment to reducing carbon footprints are key driving factors. The competitive landscape is characterized by well-established global leaders and emerging regional players focusing on localized manufacturing and energy-efficient solutions, creating a diverse and evolving market.

Asia-Pacific PVC Compound Market Forecast

Asia-Pacific’s PVC Compound market experienced dynamic growth in 2024, fueled by industrialization, urbanization, and increasing investments in construction, automotive, and consumer goods. Overall, the chemicals and Materials segment saw exponential demand due to infrastructure projects and expanding manufacturing bases. Anticipated growth from 2025 is supported by government initiatives promoting domestic production and green manufacturing. Its competitive production costs and technological advancements drive the region's dominance in key end-use markets. The competitive landscape is highly fragmented, with local manufacturers scaling operations to meet global export demands while international players continue to expand their footprints through joint ventures and acquisitions.

Middle East, Africa, Latin America PVC Compound Market Overview

The PVC Compound market across the Rest of the World, encompassing Latin America, the Middle East, and Africa, showed promising growth in 2024. This growth was supported by rising investments in the construction and energy sectors, driven by increasing oil and gas exploration and infrastructure development. From 2025, anticipated growth will stem from industrial diversification efforts, especially in GCC countries, and the adoption of high-performance materials like potassium sorbate and self-healing materials in emerging industries. The competitive landscape is evolving as regional players strengthen production capabilities and international players capitalize on untapped markets through strategic partnerships.

PVC Compound Market Dynamics and Future Analytics

The research analyses the PVC Compound parent market, derived market, intermediaries’ market, raw material market, and substitute market are all evaluated to better prospect the PVC Compound market outlook. Geopolitical analysis, demographic analysis, and Porter’s five forces analysis are prudently assessed to estimate the best PVC Compound market projections.

Recent deals and developments are considered for their potential impact on PVC Compound's future business. Other metrics analyzed include the Threat of New Entrants, Threat of New Substitutes, Product Differentiation, Degree of Competition, Number of Suppliers, Distribution Channel, Capital Needed, Entry Barriers, Govt. Regulations, Beneficial Alternative, and Cost of Substitute in PVC Compound market.

PVC Compound trade and price analysis helps comprehend PVC Compound's international market scenario with top exporters/suppliers and top importers/customer information. The data and analysis assist our clients in planning procurement, identifying potential vendors/clients to associate with, understanding PVC Compound price trends and patterns, and exploring new PVC Compound sales channels. The research will be updated to the latest month to include the impact of the latest developments such as the Russia-Ukraine war on the PVC Compound market.

PVC Compound Market Structure, Competitive Intelligence and Key Winning Strategies

The report presents detailed profiles of top companies operating in the PVC Compound market and players serving the PVC Compound value chain along with their strategies for the near, medium, and long term period.

OGAnalysis’ proprietary company revenue and product analysis model unveils the PVC Compound market structure and competitive landscape. Company profiles of key players with a business description, product portfolio, SWOT analysis, Financial Analysis, and key strategies are covered in the report. It identifies top-performing PVC Compound products in global and regional markets. New Product Launches, Investment & Funding updates, Mergers & Acquisitions, Collaboration & Partnership, Awards and Agreements, Expansion, and other developments give our clients the PVC Compound market update to stay ahead of the competition.

Company offerings in different segments across Asia-Pacific, Europe, the Middle East, Africa, and South and Central America are presented to better understand the company strategy for the PVC Compound market. The competition analysis enables users to assess competitor strategies and helps align their capabilities and resources for future growth prospects to improve their market share.

PVC Compound Market Research Scope

• Global PVC Compound market size and growth projections (CAGR), 2024- 2034

• Policies of USA New President Trump, Russia-Ukraine War, Israel-Palestine, Middle East Tensions Impact on the PVC Compound Trade and Supply-chain

• PVC Compound market size, share, and outlook across 5 regions and 27 countries, 2023- 2034

• PVC Compound market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2023- 2034

• Short and long-term PVC Compound market trends, drivers, restraints, and opportunities

• Porter’s Five Forces analysis, Technological developments in the PVC Compound market, PVC Compound supply chain analysis

• PVC Compound trade analysis, PVC Compound market price analysis, PVC Compound supply/demand

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products

• Latest PVC Compound market news and developments

The PVC Compound Market international scenario is well established in the report with separate chapters on North America PVC Compound Market, Europe PVC Compound Market, Asia-Pacific PVC Compound Market, Middle East and Africa PVC Compound Market, and South and Central America PVC Compound Markets. These sections further fragment the regional PVC Compound market by type, application, end-user, and country.

Report Scope

| Parameter | pvc compound Market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End-User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Regional Insights

North America PVC Compound market data and outlook to 2034

United States

Canada

Mexico

Europe PVC Compound market data and outlook to 2034

Germany

United Kingdom

France

Italy

Spain

BeNeLux

Russia

Asia-Pacific PVC Compound market data and outlook to 2034

China

Japan

India

South Korea

Australia

Indonesia

Malaysia

Vietnam

Middle East and Africa PVC Compound market data and outlook to 2034

Saudi Arabia

South Africa

Iran

UAE

Egypt

South and Central America PVC Compound market data and outlook to 2034

Brazil

Argentina

Chile

Peru

* We can include data and analysis of additional coutries on demand

Who can benefit from this research

The research would help top management/strategy formulators/business/product development/sales managers and investors in this market in the following ways

1. The report provides 2024 PVC Compound market sales data at the global, regional, and key country levels with a detailed outlook to 2034 allowing companies to calculate their market share and analyze prospects, uncover new markets, and plan market entry strategy.

2. The research includes the PVC Compound market split into different types and applications. This segmentation helps managers plan their products and budgets based on the future growth rates of each segment

3. The PVC Compound market study helps stakeholders understand the breadth and stance of the market giving them information on key drivers, restraints, challenges, and growth opportunities of the market and mitigating risks

4. This report would help top management understand competition better with a detailed SWOT analysis and key strategies of their competitors, and plan their position in the business

5. The study assists investors in analyzing PVC Compound business prospects by region, key countries, and top companies' information to channel their investments.

Available Customizations

The standard syndicate report is designed to serve the common interests of PVC Compound Market players across the value chain and include selective data and analysis from entire research findings as per the scope and price of the publication.

However, to precisely match the specific research requirements of individual clients, we offer several customization options to include the data and analysis of interest in the final deliverable.

Some of the customization requests are as mentioned below –

Segmentation of choice – Our clients can seek customization to modify/add a market division for types/applications/end-uses/processes of their choice.

PVC Compound Pricing and Margins Across the Supply Chain, PVC Compound Price Analysis / International Trade Data / Import-Export Analysis,

Supply Chain Analysis, Supply – Demand Gap Analysis, PESTLE Analysis, Macro-Economic Analysis, and other PVC Compound market analytics

Processing and manufacturing requirements, Patent Analysis, Technology Trends, and Product Innovations

Further, the client can seek customization to break down geographies as per their requirements for specific countries/country groups such as South East Asia, Central Asia, Emerging and Developing Asia, Western Europe, Eastern Europe, Benelux, Emerging and Developing Europe, Nordic countries, North Africa, Sub-Saharan Africa, Caribbean, The Middle East and North Africa (MENA), Gulf Cooperation Council (GCC) or any other.

Capital Requirements, Income Projections, Profit Forecasts, and other parameters to prepare a detailed project report to present to Banks/Investment Agencies.

Customization of up to 10% of the content can be done without any additional charges.

Note: Latest developments will be updated in the report and delivered within 2 to 3 working days

Market Segmentation

By Product

- Rigid PVC

- Flexible PVC

- Semi‑rigid PVC

By Application

- Pipes and Fittings

- Profiles and Tubes

- Film and Sheets

- Wire and Cables

- Flooring

- Others

By End-User

- Electrical & Electronics

- Building & Construction

- Packaging

- Automotive

- Others

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, South Korea, Rest of APAC)

- The Middle East and Africa (Saudi Arabia, UAE, Iran, South Africa, Rest of MEA)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- DIC Corporation

- Borealis AG

- Westlake Chemical Corporation

- Chemours

- Lotte Chemical Corporation

- Solvay

- Chang Chun Petrochemical

- Eastman Chemical Company

- ShinEtsu Chemical Co., Ltd.

- LG Chem, Ltd.

- LyondellBasell Industries Holdings B.V.

- SABIC

- Formosa Plastics Corporation

- Shanghai Huayi (Group) Company

Recent Developments

May 2025 – Manner Polymers laid the foundation for a cutting-edge flexible PVC compounding plant, aiming to become the lowest-cost, highest-quality, and most environmentally sustainable facility in the world.

November 2024 – Orbia’s Alphagary completed an expansion of its production capacity for healthcare-grade PVC compounds, incorporating advanced safety features and state-of-the-art equipment expected to be operational shortly.

September 2024 – Reliance Industries announced plans to build new PVC and CPVC plants at its Dahej and Nagothane sites, significantly increasing annual production capacity to meet growing local demand in India.

FAQ's

The Global PVC Compound Market is estimated to generate USD 14.1 Billion in revenue in 2025

The Global PVC Compound Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 4.6% during the forecast period from 2025 to 2034.

The PVC Compound Market is estimated to reach USD 21.8 Billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!