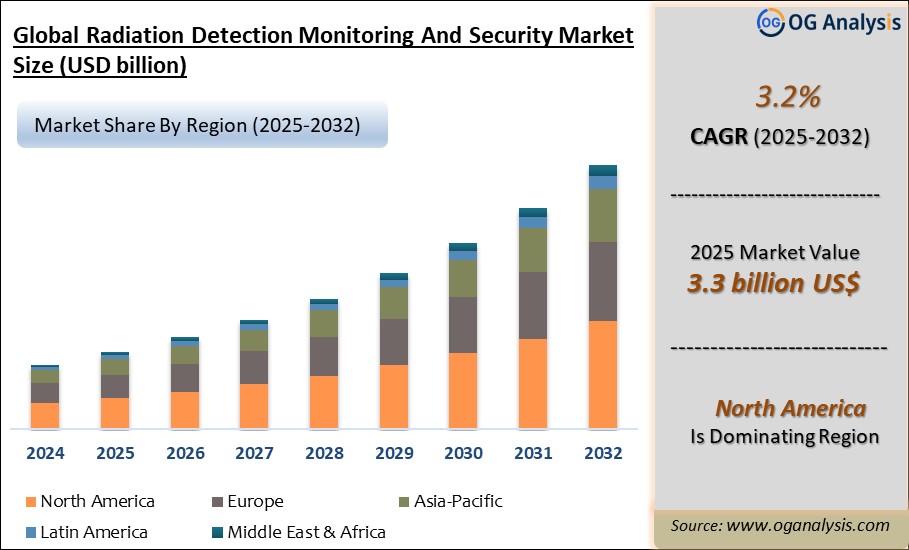

"The Global Radiation Detection Monitoring and Security Market is valued at $ 3.2 billion in 2024 and is projected to reach $ 3.3 billion in 2025. Worldwide sales of Radiation Detection Monitoring and Security are expected to grow at a significant CAGR of 3.2%, reaching USD 4.38 billion by the end of the forecast period in 2034."

The Radiation Detection, Monitoring, and Security Market is growing steadily driven by rising security concerns, regulatory mandates, and expanding applications in nuclear power, healthcare, environmental monitoring, and homeland security sectors. Radiation detection systems include detectors, dosimeters, survey meters, and portal monitors used to detect, measure, and analyse ionising radiation for safety, compliance, and threat prevention. Increasing deployment at borders, ports, nuclear facilities, and hospitals is driven by terrorism threats, radioactive material trafficking risks, and nuclear safety protocols. Technological advancements in scintillators, semiconductors, neutron detectors, and portable devices are enhancing detection accuracy, sensitivity, and operational efficiency, supporting public health protection and national security initiatives globally.

The market is competitive with key players focusing on product innovation, miniaturisation, and integration with IoT, AI, and cloud-based platforms for real-time monitoring and predictive analytics. North America dominates due to stringent nuclear safety standards, strong homeland security investments, and high medical imaging volumes, while Asia Pacific is the fastest-growing region driven by expanding nuclear power capacity, industrial safety regulations, and counter-terrorism investments in China, India, Japan, and South Korea. Key challenges include high equipment costs, regulatory approval complexities, and shortage of trained radiation safety professionals. However, future growth will be supported by advancements in wearable dosimeters, wireless monitoring networks, AI-enabled threat analysis, and integration with smart city safety systems to enhance rapid response and operational efficiency globally.

By Product, the largest segment is Radiation Detection & Monitoring Products. This is because these products are widely used across nuclear power plants, healthcare facilities, homeland security, and industrial applications to measure and monitor radiation levels in real time, ensuring safety compliance, operational efficiency, and environmental protection, thereby driving high demand globally.

By Composition, the fastest-growing segment is Solid-state Detectors. This rapid growth is driven by their superior sensitivity, compact design, faster response times, and increasing adoption in portable, handheld, and wearable devices for diverse applications including medical imaging, environmental monitoring, and security screening where high accuracy and reliability are critical.

Key Insights

- The radiation detection, monitoring, and security market is growing steadily as governments, utilities, healthcare, and security agencies deploy radiation monitoring solutions to ensure safety, regulatory compliance, environmental protection, and prevention of radioactive material misuse in nuclear, industrial, and public infrastructure operations worldwide.

- Scintillator-based detectors hold the largest market share due to their high sensitivity, detection accuracy, and widespread adoption in nuclear power plants, homeland security, environmental monitoring, and medical imaging applications requiring precise real-time radiation measurement and threat detection capabilities.

- North America dominates the market driven by strict nuclear safety regulations, strong homeland security investments, and high healthcare imaging volumes requiring advanced radiation detection systems for operational safety, compliance, and national security across multiple sectors.

- Asia Pacific is the fastest-growing regional market due to rapid industrialisation, nuclear power expansion, environmental safety regulations, and rising counter-terrorism and border security infrastructure investments in China, India, Japan, and Southeast Asian countries supporting market demand.

- Handheld and portable radiation detectors are witnessing strong demand due to their lightweight design, rapid deployment, ease of use, and suitability for field inspections, security screening, emergency response, and industrial safety monitoring applications globally.

- Integration of IoT, AI, and cloud-based platforms with radiation monitoring systems is gaining traction as they enable real-time data collection, predictive analysis, remote monitoring, and rapid decision-making to improve operational efficiency and safety outcomes.

- Healthcare applications such as nuclear medicine, oncology, radiology, and cancer treatment drive significant demand for radiation monitoring devices to ensure accurate dose measurement, patient and staff safety, and regulatory compliance in hospitals and diagnostic centres.

- Technological advancements in semiconductor-based detectors, wearable dosimeters, neutron detection materials, and wireless monitoring networks are enhancing detection sensitivity, operational reliability, portability, and scalability for diverse industrial, environmental, and security applications.

- High equipment costs, stringent regulatory approvals, and shortage of skilled radiation safety professionals remain key challenges limiting market adoption, especially in developing regions with limited technical expertise and financial resources for advanced safety infrastructure investments.

- Future market growth will be driven by innovations in AI-enabled threat analysis, wireless radiation monitoring networks, integration with smart city safety systems, and increasing global emphasis on environmental radiation monitoring and nuclear security to protect public health and national safety.

Global uranium mine production (tonnes U), 2018–2024

Figure: Global uranium mine production has rebounded since 2021, signalling higher activity across the nuclear fuel cycle. This underpins sustained demand for advanced radiation detection, monitoring and security systems in mining, processing, transport and nuclear power operations.

- The market outlook is closely tied to activity across the nuclear fuel cycle. According to the World Nuclear Association, global uranium mine production recovered from around 47–48 thousand tonnes U in 2020–2021 to more than 60 thousand tonnes U in 2024, marking an increase of roughly a quarter over this period. This resurgence in uranium mining and fuel-cycle investment, together with record nuclear electricity generation in 2024, is driving sustained demand for high-performance radiation detection, monitoring and security systems at mines, processing plants, transport corridors and reactor sites.

Reort Scope

| Parameter | Detail |

|---|---|

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Composition, By End User, By Equipment |

| Countries Covered | North America (USA, Canada, Mexico) Europe (Germany, UK, France, Spain, Italy, Rest of Europe) Asia-Pacific (China, India, Japan, Australia, Rest of APAC) The Middle East and Africa (Middle East, Africa) South and Central America (Brazil, Argentina, Rest of SCA) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10 % free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Datafile |

Market Segmentation

By Product

- Radiation Detection & Monitoring Products

- Radiation Safety Products

By Composition

- Gas-filled Detectors

- Scintillators

- Solid-state Detectors

By End User

- Medical and Healthcare

- Industrial

- Homeland Security and Defense

- Energy and Power

- Other End User Industries

By Equipment

- Personal Dosimeters

- Area Process Monitors

- Environmental Radiation Monitor

- Surface Contamination Monitor

- Radioactive Material Monitor

- Others

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- Thermo Fisher Scientific Inc.

- Mirion Technologies Inc.

- AMETEK Inc. (ORTEC)

- Fortive Corp. (LANDAUER & Fluke Biomedical)

- Fuji Electric Co., Ltd.

- Smiths Detection

- Teledyne FLIR

- Rapiscan Systems Inc. (OSI Systems)

- Leidos Holdings, Inc.

- Kromek Group plc

- Polimaster LLC

- Ludlum Measurements Inc.

- CAEN SpA (CAEN SyS)

- Arktis Radiation Detectors Ltd.

- Alpha Spectra Inc.

Recent Development

February 2025 – Mirion Technologies launched the IC3™ Portable Ion Chamber Survey Meter, a handheld tool offering accurate gamma, beta, and X-ray detection without the need for desiccant, ideal for nuclear plants and regulatory compliance.

What You Receive

• Global Radiation Detection Monitoring And Security market size and growth projections (CAGR), 2024- 2034

• Impact of recent changes in geopolitical, economic, and trade policies on the demand and supply chain of Radiation Detection Monitoring And Security.

• Radiation Detection Monitoring And Security market size, share, and outlook across 5 regions and 27 countries, 2025- 2034.

• Radiation Detection Monitoring And Security market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2025- 2034.

• Short and long-term Radiation Detection Monitoring And Security market trends, drivers, restraints, and opportunities.

• Porter’s Five Forces analysis, Technological developments in the Radiation Detection Monitoring And Security market, Radiation Detection Monitoring And Security supply chain analysis.

• Radiation Detection Monitoring And Security trade analysis, Radiation Detection Monitoring And Security market price analysis, Radiation Detection Monitoring And Security Value Chain Analysis.

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products.

• Latest Radiation Detection Monitoring And Security market news and developments.

The Radiation Detection Monitoring And Security Market international scenario is well established in the report with separate chapters on North America Radiation Detection Monitoring And Security Market, Europe Radiation Detection Monitoring And Security Market, Asia-Pacific Radiation Detection Monitoring And Security Market, Middle East and Africa Radiation Detection Monitoring And Security Market, and South and Central America Radiation Detection Monitoring And Security Markets. These sections further fragment the regional Radiation Detection Monitoring And Security market by type, application, end-user, and country.

Who can benefit from this research

The research would help top management/strategy formulators/business/product development/sales managers and investors in this market in the following ways

1. The report provides 2024 Radiation Detection Monitoring And Security market sales data at the global, regional, and key country levels with a detailed outlook to 2034, allowing companies to calculate their market share and analyze prospects, uncover new markets, and plan market entry strategy.

2. The research includes the Radiation Detection Monitoring And Security market split into different types and applications. This segmentation helps managers plan their products and budgets based on the future growth rates of each segment

3. The Radiation Detection Monitoring And Security market study helps stakeholders understand the breadth and stance of the market giving them information on key drivers, restraints, challenges, and growth opportunities of the market and mitigating risks

4. This report would help top management understand competition better with a detailed SWOT analysis and key strategies of their competitors, and plan their position in the business

5. The study assists investors in analyzing Radiation Detection Monitoring And Security business prospects by region, key countries, and top companies' information to channel their investments.

Available Customizations

The standard syndicate report is designed to serve the common interests of Radiation Detection Monitoring And Security Market players across the value chain and include selective data and analysis from entire research findings as per the scope and price of the publication.

However, to precisely match the specific research requirements of individual clients, we offer several customization options to include the data and analysis of interest in the final deliverable.

Some of the customization requests are as mentioned below :

Segmentation of choice – Our clients can seek customization to modify/add a market division for types/applications/end-uses/processes of their choice.

Radiation Detection Monitoring And Security Pricing and Margins Across the Supply Chain, Radiation Detection Monitoring And Security Price Analysis / International Trade Data / Import-Export Analysis

Supply Chain Analysis, Supply–Demand Gap Analysis, PESTLE Analysis, Macro-Economic Analysis, and other Radiation Detection Monitoring And Security market analytics

Processing and manufacturing requirements, Patent Analysis, Technology Trends, and Product Innovations

Further, the client can seek customization to break down geographies as per their requirements for specific countries/country groups such as South East Asia, Central Asia, Emerging and Developing Asia, Western Europe, Eastern Europe, Benelux, Emerging and Developing Europe, Nordic countries, North Africa, Sub-Saharan Africa, Caribbean, The Middle East and North Africa (MENA), Gulf Cooperation Council (GCC) or any other.

Capital Requirements, Income Projections, Profit Forecasts, and other parameters to prepare a detailed project report to present to Banks/Investment Agencies.

Customization of up to 10% of the content can be done without any additional charges.

Note: Latest developments will be updated in the report and delivered within 2 to 3 working days.

FAQ's

The Global Radiation Detection Monitoring and Security Market is estimated to generate USD 3.2 billion in revenue in 2024.

The Global Radiation Detection Monitoring and Security Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 3.2% during the forecast period from 2025 to 2032.

The Radiation Detection Monitoring and Security Market is estimated to reach USD 4.1 billion by 2032.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!