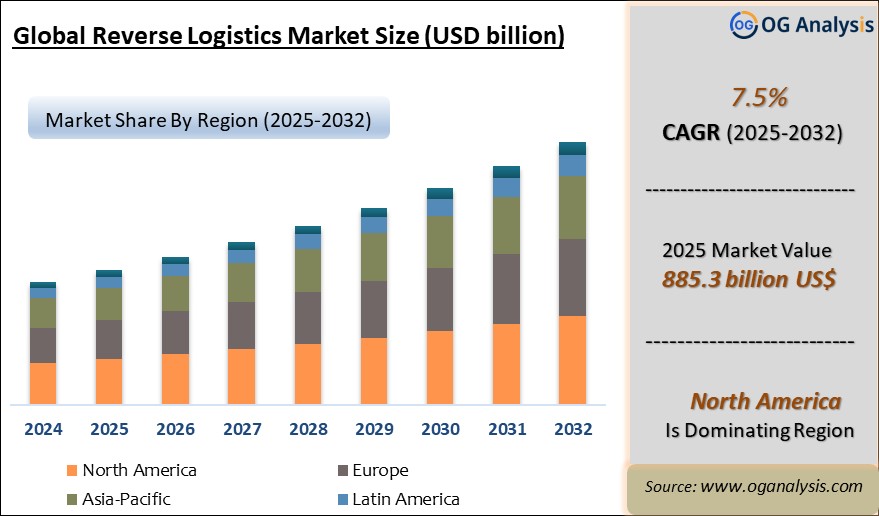

"The Global Reverse Logistics Market valued at USD 823.5 Billion in 2024, is expected to grow by 7.5% CAGR to reach market size worth USD 1,732.9 Billion by 2034."

The Reverse Logistics market plays a vital role in today’s global supply chains, focusing on the efficient movement of goods from consumers back to manufacturers or distribution centers for returns, repairs, recycling, refurbishing, or proper disposal. As e-commerce continues to surge, reverse logistics has become increasingly important for retailers and logistics providers seeking to optimize customer service and manage operational costs associated with returns. High return rates, especially in online retail sectors like apparel, electronics, and consumer goods, are driving the adoption of advanced reverse logistics solutions. These solutions enable faster processing, better inventory recovery, and sustainable end-of-life product management. The market is further supported by rising environmental concerns and regulations mandating proper waste management and resource recovery. With businesses aiming to improve circular economy outcomes and reduce landfill contributions, reverse logistics is no longer viewed as a cost burden but rather as a strategic function that drives customer loyalty and operational efficiency.

The evolving competitive landscape of the Reverse Logistics market includes third-party logistics (3PL) providers, specialized return solution companies, manufacturers, and retailers developing in-house capabilities. Technology integration—such as AI, IoT tracking, blockchain, and automated return processing systems—is reshaping how businesses handle returned goods. Companies are also investing in analytics tools to gain better visibility into return patterns, optimize routes, and reduce waste. Additionally, the increasing focus on sustainable practices has prompted the development of closed-loop systems, where used products are reintroduced into the value chain through repair, remanufacturing, or recycling. Key industries driving market growth include retail and e-commerce, automotive, consumer electronics, and pharmaceuticals. As global trade expands and regulations tighten around product disposal and reuse, the Reverse Logistics market is expected to see consistent growth through 2034, transforming from a reactive service into a proactive, value-generating function across multiple sectors.

Reverse Logistics Market Strategy, Price Trends, Drivers, Challenges and Opportunities to 2034

-

The rapid expansion of e-commerce has drastically increased return volumes, making reverse logistics a critical element of supply chain management. Companies are implementing centralized return processing centers and intelligent routing to handle high product turnover efficiently and cost-effectively while maintaining customer satisfaction and brand reputation.

-

Environmental sustainability is a major driver of reverse logistics investment, as businesses face growing pressure to reduce waste and carbon emissions. Reuse, recycling, and refurbishment through reverse channels are helping organizations align with ESG targets and comply with global waste reduction regulations.

-

Third-party logistics (3PL) providers are strengthening their reverse logistics capabilities by offering integrated services like inspection, grading, repair, and restocking. These providers allow businesses to scale returns handling and focus on core operations without investing heavily in dedicated infrastructure.

-

Artificial intelligence and machine learning are being applied to predict return likelihood, streamline authorizations, and automate routing decisions. These tools help lower return-related costs, reduce fraud, and improve response time across various industries, especially in high-return sectors like fashion and electronics.

-

The integration of IoT sensors and tracking devices in packaging and products is improving transparency in reverse logistics operations. These technologies enable real-time tracking, condition monitoring, and predictive maintenance, which helps reduce losses and optimize asset recovery.

-

Closed-loop supply chains are gaining momentum in the electronics and automotive industries. Manufacturers are designing products for disassembly, reuse, or component harvesting, which reduces dependency on virgin materials and supports circular economy models.

-

Enhancing customer experience during the return process is becoming a priority, with offerings such as instant credit, automated return approvals, and home pickup. These initiatives improve brand loyalty while enabling more predictable and streamlined return workflows.

-

The pharmaceutical sector is seeing rising investment in reverse logistics to ensure the secure return and disposal of expired or unused medications. Strict traceability requirements and regulatory compliance are driving demand for controlled, transparent, and tamper-proof systems.

-

Data analytics is playing a transformative role in reverse logistics by uncovering insights into return frequency, reasons, and product-level performance. These findings are being used to reduce future returns through improved product design, quality control, and marketing clarity.

-

Cross-border returns are increasingly complex due to differing tax structures, regulations, and customs procedures. Businesses are addressing this with regional reverse logistics hubs and digital solutions that automate customs documentation and ensure timely, compliant returns handling.

North America Reverse Logistics Market Analysis

The North American Reverse Logistics market experienced significant developments in 2024, driven by the rapid adoption of advanced automotive technologies such as electric vehicle telematics, artificial intelligence, and blockchain solutions. The region has become a hub for innovation in automotive IoT, autonomous driving, and electrification, supported by favorable regulatory frameworks and increasing investments in R&D. The Reverse Logistics market is projected to witness robust growth from 2025, fueled by the expansion of EV charging infrastructure, rising demand for smart mobility solutions, and advancements in lightweight materials like copper busbars and tire fabrics. Key players are enhancing their competitive edge through strategic partnerships and product diversification, focusing on sustainability and energy efficiency. The market landscape remains dynamic with a high degree of competition, marked by major OEMs and emerging startups leveraging digital transformation to address evolving consumer demands.

Europe Reverse Logistics Market Outlook

In 2024, the European Reverse Logistics market showcased a strong focus on sustainability, aligning with stringent environmental regulations and the European Green Deal. Key developments included advancements in electric vehicle components, such as HVAC compressors and turbochargers, alongside innovations in AI-powered automotive technologies and smart mobility solutions. Anticipated growth from 2025 is underpinned by increased electrification in the automotive sector, expansion of bike and scooter-sharing telematics, and the deployment of second-life EV batteries. The region’s automotive giants are collaborating with technology providers to enhance vehicle connectivity and automation. The competitive landscape is shaped by a mix of established players and innovative disruptors, as the market transitions towards circular economy models and next-generation mobility solutions.

Asia-Pacific Reverse Logistics Market Forecast

The Asia-Pacific Reverse Logistics market recorded exceptional progress in 2024, primarily driven by booming EV adoption, urbanization, and rising disposable incomes. Developments spanned automotive powertrain sensors, AI-driven telematics, and tire cord innovations catering to high-performance vehicles. Growth projections for 2025 are bolstered by government incentives for EV manufacturing, rapid advancements in semiconductor technologies, and the integration of IoT across automotive applications. The competitive landscape is characterized by a strong presence of regional manufacturers and global players expanding operations to cater to this high-potential market. China and India remain focal points, with escalating demand for smart, connected, and sustainable automotive solutions.

Middle East, Africa, Latin America Reverse Logistics Market Overview

The Reverse Logistics market across the Middle East, Africa, Latin America witnessed steady advancements in 2024, driven by growing investments in automotive refinish coatings, reverse logistics, and railcar leasing for freight transportation. Markets in Latin America and the Middle East are positioning themselves as emerging hubs for smart mobility and automotive blockchain technologies. Expected growth from 2025 will be driven by rising industrialization, improved logistics networks, and adoption of second-life EV batteries to address sustainability challenges. Competitive dynamics in the RoW are defined by niche players catering to local demands and global manufacturers exploring untapped markets. The focus remains on affordability, customization, and fostering innovation to navigate diverse market conditions.

Reverse Logistics Market Dynamics and Future Analytics

The research analyses the Reverse Logistics parent market, derived market, intermediaries’ market, raw material market, and substitute market are all evaluated to better prospect the Reverse Logistics market outlook. Geopolitical analysis, demographic analysis, and Porter’s five forces analysis are prudently assessed to estimate the best Reverse Logistics market projections.

Recent deals and developments are considered for their potential impact on Reverse Logistics's future business. Other metrics analyzed include the Threat of New Entrants, Threat of New Substitutes, Product Differentiation, Degree of Competition, Number of Suppliers, Distribution Channel, Capital Needed, Entry Barriers, Govt. Regulations, Beneficial Alternative, and Cost of Substitute in Reverse Logistics market.

Reverse Logistics trade and price analysis helps comprehend Reverse Logistics's international market scenario with top exporters/suppliers and top importers/customer information. The data and analysis assist our clients in planning procurement, identifying potential vendors/clients to associate with, understanding Reverse Logistics price trends and patterns, and exploring new Reverse Logistics sales channels. The research will be updated to the latest month to include the impact of the latest developments such as the Russia-Ukraine war on the Reverse Logistics market.

Reverse Logistics Market Structure, Competitive Intelligence and Key Winning Strategies

The report presents detailed profiles of top companies operating in the Reverse Logistics market and players serving the Reverse Logistics value chain along with their strategies for the near, medium, and long term period.

OGAnalysis’ proprietary company revenue and product analysis model unveils the Reverse Logistics market structure and competitive landscape. Company profiles of key players with a business description, product portfolio, SWOT analysis, Financial Analysis, and key strategies are covered in the report. It identifies top-performing Reverse Logistics products in global and regional markets. New Product Launches, Investment & Funding updates, Mergers & Acquisitions, Collaboration & Partnership, Awards and Agreements, Expansion, and other developments give our clients the Reverse Logistics market update to stay ahead of the competition.

Company offerings in different segments across Asia-Pacific, Europe, the Middle East, Africa, and South and Central America are presented to better understand the company strategy for the Reverse Logistics market. The competition analysis enables users to assess competitor strategies and helps align their capabilities and resources for future growth prospects to improve their market share.

Reverse Logistics Market Research Scope

• Global Reverse Logistics market size and growth projections (CAGR), 2024- 2034

• Policies of USA New President Trump, Russia-Ukraine War, Israel-Palestine, Middle East Tensions Impact on the Reverse Logistics Trade and Supply-chain

• Reverse Logistics market size, share, and outlook across 5 regions and 27 countries, 2023- 2034

• Reverse Logistics market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2023- 2034

• Short and long-term Reverse Logistics market trends, drivers, restraints, and opportunities

• Porter’s Five Forces analysis, Technological developments in the Reverse Logistics market, Reverse Logistics supply chain analysis

• Reverse Logistics trade analysis, Reverse Logistics market price analysis, Reverse Logistics supply/demand

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products

• Latest Reverse Logistics market news and developments

The Reverse Logistics Market international scenario is well established in the report with separate chapters on North America Reverse Logistics Market, Europe Reverse Logistics Market, Asia-Pacific Reverse Logistics Market, Middle East and Africa Reverse Logistics Market, and South and Central America Reverse Logistics Markets. These sections further fragment the regional Reverse Logistics market by type, application, end-user, and country.

Who can benefit from this research

The research would help top management/strategy formulators/business/product development/sales managers and investors in this market in the following ways

1. The report provides 2024 Reverse Logistics market sales data at the global, regional, and key country levels with a detailed outlook to 2034 allowing companies to calculate their market share and analyze prospects, uncover new markets, and plan market entry strategy.

2. The research includes the Reverse Logistics market split into different types and applications. This segmentation helps managers plan their products and budgets based on the future growth rates of each segment

3. The Reverse Logistics market study helps stakeholders understand the breadth and stance of the market giving them information on key drivers, restraints, challenges, and growth opportunities of the market and mitigating risks

4. This report would help top management understand competition better with a detailed SWOT analysis and key strategies of their competitors, and plan their position in the business

5. The study assists investors in analyzing Reverse Logistics business prospects by region, key countries, and top companies' information to channel their investments.

Available Customizations

The standard syndicate report is designed to serve the common interests of Reverse Logistics Market players across the value chain and include selective data and analysis from entire research findings as per the scope and price of the publication.

However, to precisely match the specific research requirements of individual clients, we offer several customization options to include the data and analysis of interest in the final deliverable.

Some of the customization requests are as mentioned below –

Segmentation of choice – Our clients can seek customization to modify/add a market division for types/applications/end-uses/processes of their choice.

Reverse Logistics Pricing and Margins Across the Supply Chain, Reverse Logistics Price Analysis / International Trade Data / Import-Export Analysis,

Supply Chain Analysis, Supply – Demand Gap Analysis, PESTLE Analysis, Macro-Economic Analysis, and other Reverse Logistics market analytics

Processing and manufacturing requirements, Patent Analysis, Technology Trends, and Product Innovations

Further, the client can seek customization to break down geographies as per their requirements for specific countries/country groups such as South East Asia, Central Asia, Emerging and Developing Asia, Western Europe, Eastern Europe, Benelux, Emerging and Developing Europe, Nordic countries, North Africa, Sub-Saharan Africa, Caribbean, The Middle East and North Africa (MENA), Gulf Cooperation Council (GCC) or any other.

Capital Requirements, Income Projections, Profit Forecasts, and other parameters to prepare a detailed project report to present to Banks/Investment Agencies.

Customization of up to 10% of the content can be done without any additional charges.

Note: Latest developments will be updated in the report and delivered within 2 to 3 working days

| Parameter | Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application and By End-User |

| Countries Covered | North America (USA, Canada, Mexico) Europe (Germany, UK, France, Spain, Italy, Rest of Europe) Asia-Pacific (China, India, Japan, Australia, Rest of APAC) The Middle East and Africa (Middle East, Africa) South and Central America (Brazil, Argentina, Rest of SCA) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Datafile |

Recent Developments

-

June 2025 ReverseLogix was recognized as the Overall eCommerce Solution Provider of the Year for its comprehensive returns management platform. The award highlights its contributions to automation, sustainability, and streamlined recommerce processing across multiple retail channels.

-

June 2025 UPS completed the integration of Happy Returns, while DHL Supply Chain finalized the acquisition of Inmar Supply Chain Solutions. These moves expand reverse logistics capabilities across North America, adding automation, returns tracking, and asset recovery solutions.

-

June 2025 The National Retail Federation announced the launch of NRF Rev, a rebranded event that will debut in 2026 alongside the NRF Big Show. The new format will focus on reverse logistics, circular economy models, and technology-driven return management.

-

March 2025 At the Reverse Logistics Association Conference & Expo in Las Vegas, industry leaders emphasized reverse logistics as a strategic advantage. Companies are increasingly focused on turning returns into revenue streams through remarketing and closed-loop supply chains.

-

June 2025 Reverse Logistics Group (RLG) confirmed participation in Responsible Business USA 2025 in New York City. The company plans to highlight its initiatives in extended producer responsibility (EPR), take-back programs, and circular supply chain services.

-

April 2025 DHL Supply Chain announced major upgrades to its returns handling services, featuring automation, smart warehouse integrations, and analytics tools. These enhancements aim to reduce processing time and increase value recovery for e-commerce clients.

-

February 2025 GXO Logistics expanded its global reverse logistics services with new return management hubs. The company is focusing on large-scale refurbishment, repair, and return-to-stock operations to support clients in retail, electronics, and apparel sectors.

FAQ's

The Reverse Logistics Market is estimated to reach USD 1,732.9 Billion by 2034.

The Global Reverse Logistics Market is estimated to generate USD 876.4 Billion in revenue in 2025

The Global Reverse Logistics Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% during the forecast period from 2025 to 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!