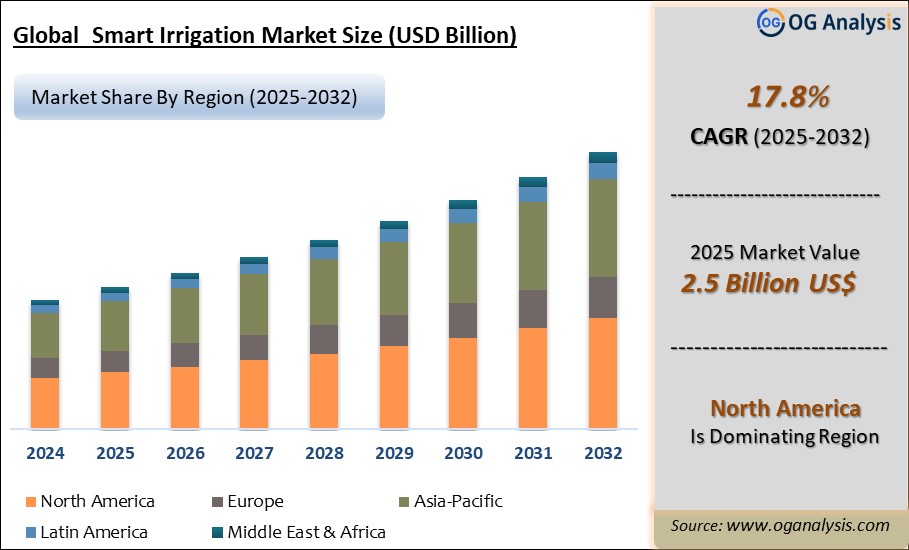

"Smart Irrigation Market is valued at $ 2.95 billion in 2026. Further, the market is expected to grow at a CAGR of 17.8% to reach USD 11.1 billion by 2034."

The Smart Irrigation Market is a rapidly growing segment of water management, precision agriculture, landscaping automation, and climate-resilient infrastructure, driven by the need to optimize water use, improve crop productivity, reduce labor dependency, and respond to rising water scarcity. Smart irrigation systems use sensors, controllers, weather data, soil moisture monitoring, flow meters, remote valves, mobile applications, analytics platforms, and automated scheduling tools to deliver water based on real-time field, landscape, or environmental conditions. These systems are widely used in agriculture, greenhouses, commercial landscapes, residential lawns, golf courses, sports grounds, municipal parks, nurseries, and institutional campuses. Demand is supported by groundwater depletion, irregular rainfall, rising irrigation costs, government water-conservation programs, and increasing adoption of precision farming technologies.

The competitive landscape of the Smart Irrigation Market includes irrigation equipment manufacturers, sensor companies, agricultural technology firms, landscape automation providers, IoT platform vendors, pump and valve suppliers, weather intelligence companies, and system integrators. Companies compete through water-saving performance, sensor accuracy, ease of installation, mobile connectivity, automation capability, compatibility with existing irrigation infrastructure, durability, service support, and cost-effectiveness. Latest trends include soil moisture-based irrigation, weather-based controllers, AI-enabled irrigation scheduling, remote monitoring, fertigation integration, solar-powered irrigation systems, drip irrigation automation, and smart irrigation linked with farm management platforms. Growth is driven by precision agriculture adoption, water-use regulations, commercial landscaping efficiency, climate variability, and demand for higher crop yields with lower water input. However, challenges include high upfront costs, limited technical awareness, connectivity gaps in rural areas, sensor maintenance, fragmented farm holdings, and difficulty proving return on investment for small users. The outlook remains positive as water efficiency becomes a central priority across agriculture, urban landscapes, and sustainable infrastructure.

Key Insights

- Smart irrigation is becoming essential as water scarcity increases pressure on farmers, municipalities, and property owners to use water more efficiently. Traditional irrigation methods often lead to overwatering, runoff, and uneven distribution, while smart systems apply water based on actual soil, crop, and weather conditions. This improves resource efficiency and supports long-term water security.

- Agriculture remains the largest opportunity area because irrigation directly affects crop yield, quality, and farm profitability. Soil moisture sensors, automated valves, drip irrigation controls, and weather-linked scheduling help growers reduce water waste while maintaining crop health. Smart irrigation is especially valuable for high-value crops, orchards, vineyards, vegetables, and greenhouse farming.

- Weather-based irrigation controllers are gaining adoption in residential, commercial, and municipal landscapes because they automatically adjust watering schedules based on temperature, rainfall, humidity, wind, and evapotranspiration data. These systems reduce unnecessary watering and help landscapes remain healthy without manual schedule changes. Their convenience makes them attractive for urban water conservation programs.

- Soil moisture sensors are a key technology segment because they provide direct field-level data on water availability in the root zone. This allows irrigation to be applied only when needed, reducing under-irrigation and over-irrigation risks. Sensor accuracy, placement, calibration, and durability strongly influence system performance and user confidence.

- Drip irrigation automation is expanding as growers combine precise water delivery with smart controllers and fertigation systems. Automated drip systems reduce evaporation losses, improve nutrient delivery, and support better crop uniformity. This approach is particularly relevant in water-stressed agricultural regions and high-value horticulture operations.

- Commercial landscaping and public green spaces are adopting smart irrigation to reduce water bills, comply with conservation rules, and improve maintenance efficiency. Hotels, corporate campuses, schools, hospitals, parks, sports grounds, and golf courses use smart systems to manage large irrigated areas more consistently. Remote monitoring helps maintenance teams detect faults and adjust schedules quickly.

- IoT and mobile connectivity are improving system usability by allowing users to monitor irrigation performance, change schedules, receive alerts, and track water use remotely. Cloud-based platforms can integrate sensor data, weather forecasts, pump status, and zone-level irrigation activity. This supports better decision-making for both farmers and landscape managers.

- AI and analytics are emerging as important differentiators as smart irrigation systems move beyond basic automation toward predictive water management. Advanced platforms can recommend irrigation timing, estimate crop water demand, detect leaks, and optimize schedules based on historical and real-time data. These capabilities improve water savings and operational control.

- Government incentives and water-use regulations are supporting market adoption, particularly in drought-prone regions and urban areas facing water restrictions. Subsidies, conservation rebates, green building standards, and agricultural water-efficiency programs encourage users to invest in smart irrigation technologies. Policy support can significantly accelerate market penetration.

- Competition is shifting toward integrated water management solutions that combine sensors, controllers, valves, pumps, fertigation, weather intelligence, software, and support services. Customers increasingly prefer systems that are easy to install, compatible with existing infrastructure, and capable of delivering measurable water savings. Companies offering reliable, scalable, and user-friendly solutions are expected to remain well positioned.

Regional Analysis

North America Smart Irrigation Market

North America Smart Irrigation Market is driven by water conservation mandates, drought management needs, advanced farming practices, commercial landscaping efficiency, and strong adoption of precision agriculture technologies. Market dynamics are shaped by demand from farms, golf courses, residential landscapes, municipal parks, corporate campuses, and institutional facilities seeking automated irrigation scheduling, soil moisture monitoring, and remote water-use control. Lucrative opportunities exist for irrigation equipment manufacturers, sensor providers, IoT platform companies, landscape automation firms, pump and valve suppliers, and precision farming solution providers. Latest trends include weather-based controllers, AI-enabled irrigation scheduling, mobile app-based monitoring, smart sprinkler systems, drip automation, and integration with farm management platforms. The forecast outlook remains favorable as growers, municipalities, and property owners continue prioritizing water savings, labor efficiency, crop productivity, and climate-resilient landscape management.

Asia Pacific Smart Irrigation Market

Asia Pacific Smart Irrigation Market is expanding due to rising agricultural water demand, population growth, food security concerns, groundwater depletion, and increasing government support for efficient irrigation systems. Market dynamics are supported by adoption across rice, fruits, vegetables, plantations, orchards, greenhouses, and high-value crops, along with growing use in urban landscaping and smart city projects. The region presents strong opportunities for smart irrigation controller suppliers, sensor manufacturers, drip irrigation companies, agri-tech platforms, solar pump providers, and local system integrators offering affordable and scalable solutions. Latest trends include sensor-based irrigation, mobile advisory platforms, automated drip systems, fertigation integration, solar-powered irrigation, and remote monitoring for smallholder and commercial farms. The forecast remains positive as farmers and governments continue investing in water-efficient agriculture, higher crop yields, and digitally enabled farm management.

Europe Smart Irrigation Market

Europe Smart Irrigation Market is shaped by sustainability regulations, water-use efficiency goals, precision agriculture adoption, climate variability, and demand for smart landscaping across urban and commercial environments. Market dynamics are influenced by the need to reduce water wastage in agriculture, vineyards, orchards, greenhouses, sports grounds, parks, and public infrastructure. Lucrative opportunities exist for irrigation automation providers, sensor companies, greenhouse technology firms, farm software vendors, smart water management companies, and sustainable landscaping solution providers. Latest trends include evapotranspiration-based scheduling, IoT-enabled irrigation networks, smart greenhouse irrigation, low-water landscaping, automated fertigation, and integration with climate-smart farming tools. The forecast outlook remains steady as European users continue focusing on resource efficiency, environmental compliance, sustainable crop production, and intelligent water management.

Middle East & Africa Smart Irrigation Market

Middle East & Africa Smart Irrigation Market is developing through water scarcity pressures, arid climate conditions, food security programs, controlled-environment agriculture, landscaping needs, and efforts to improve irrigation efficiency. Market dynamics vary across the region, with Gulf countries showing stronger demand from smart farms, greenhouses, golf courses, municipal landscaping, and large commercial properties, while African markets present opportunities through drip irrigation, solar-powered pumps, mobile-based advisory systems, and smallholder water management. Companies can benefit by offering durable, affordable, low-maintenance, and climate-suitable smart irrigation solutions. Latest trends include automated drip irrigation, soil moisture sensing, smart fertigation, protected cultivation, solar irrigation systems, and remote monitoring for water-stressed farms. The forecast remains constructive as governments, growers, and developers continue prioritizing water conservation, agricultural productivity, and resilient irrigation infrastructure.

South & Central America Smart Irrigation Market

South & Central America Smart Irrigation Market is supported by large-scale agriculture, export-oriented crop production, water-efficiency needs, climate variability, and rising adoption of precision farming tools. Market dynamics are shaped by demand from soybean, corn, sugarcane, coffee, fruits, vegetables, vineyards, and livestock-related forage production, where irrigation efficiency directly affects yield quality and farm profitability. Opportunities exist for irrigation equipment companies, agri-tech start-ups, sensor providers, drone and satellite analytics firms, pump suppliers, and farm automation integrators offering practical smart irrigation systems. Latest trends include automated drip and sprinkler systems, soil moisture monitoring, fertigation control, satellite-linked irrigation planning, and mobile-based water-use management. The forecast outlook remains positive as commercial farms and agribusinesses continue investing in productivity, sustainability, input optimization, and climate-resilient water management.

Report Scope

| Parameter | Smart Irrigation Market Detail |

| Base Year | 2024 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Type, By Technology, By Component, By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Type

- Climate-Based

- Sensor-Based

By Technology

- Evapotranspiration

- Soil Moisture

By Component

- Sensors

- Controllers

- Water Flow Meters

- Software

- Other Components

By End User

- Agriculture

- Golf Course

- Residential

- Other End Users

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- AquaSpy Inc.

- Calsense

- Galcon Ltd.

- Hunter Industries Inc.

- HydroPoint Data Systems Inc.

- Netafim USA

- Rachio Inc.

- Rain Bird Corporation

- Stevens Water Monitoring Systems Inc.

- The Toro Company

- Weathermatic Industries Inc.

- Banyan Water Inc.

- Caipos GmbH

- Delta-T Devices Ltd.

- Jain Irrigation Systems Ltd.

- Manna Irrigation Ltd.

- Orbit Irrigation Products LLC

- Soil Scout Oy

- Valmont Industries Inc.

- Nelson Irrigation Corporation

- Tucor Inc.

- Irritec S. p. A.

- Antelco Pty Ltd.

- Conserva Irrigation Holdings LLC

- WaterBit Inc.

- Hortau Inc.

- Ewing Irrigation & Landscape Supply Inc.

- Signature Control Systems Inc.

- Green IQ Ltd.

- Hortech Systems Ltd.

- Spraying Systems Co.

- Acclima Inc.

- HortControl LLC

Recent Developments

- April 2026 - Rachio, now a Rain Bird company, bundled its Smart Sprinkler Controller with Rain Bird Rotary Nozzles through a Zone Upgrade Kit. The move supports easier residential smart irrigation adoption by combining controller intelligence with water-efficient nozzle upgrades in one purchase.

- April 2026 - CropX expanded its digital agronomy platform with the Apex multi-depth soil sensor. The product strengthens root-zone monitoring, irrigation decision support, salinity tracking, and remote crop management for precision agriculture users.

- April 2026 - Irrigreen’s Smart Irrigation System 3.0 gained attention for its digitally controlled “water-printing” sprinkler technology and expanded drip irrigation support. The system highlights growing demand for app-based, zone-specific watering with pressure sensing and weather-based automation.

- March 2026 - Research activity advanced around smart automated irrigation systems with real-time sensor monitoring, mobile application control, and IoT-based water-use optimization. This supports the market shift toward low-cost, connected irrigation platforms for small-scale and commercial farms.

- February 2026 - John Deere announced its 2026 Startup Collaborator cohort, including companies working on soil sensing, edge AI, drone crop intelligence, robotics models, and telematics. The program reinforces stronger collaboration between equipment manufacturers and smart irrigation or precision agriculture technology start-ups.

- January 2026 - Netafim advanced plans to roll out a digital farming system for smallholders in Asia, with GrowSphere positioned to simplify precision irrigation and fertigation using IoT, cloud computing, data analytics, and agronomic recommendations.

- December 2025 - Lindsay Corporation announced a major irrigation equipment order, with deliveries expected through fiscal 2026. The order supports continued demand for pivot irrigation, FieldNET-connected systems, and smart irrigation scheduling technologies.

- October 2025 - Rain Bird acquired Rachio, expanding its position in smart and sustainable irrigation solutions. The acquisition brought together Rain Bird’s irrigation expertise and Rachio’s connected controller platform for residential water management.

- July 2025 - Netafim India expanded its climate-smart farming mission, including use of GrowSphere digital farming tools for remote irrigation and fertigation management. The development supports broader adoption of smart irrigation in water-stressed agricultural regions.

- January 2025 - Aiper introduced the IrriSense Smart Irrigation Sprinkler at CES 2025, featuring app-defined spray mapping, weather-aware watering schedules, soil moisture sensing, and targeted sprinkler coverage. The product reflects smart irrigation expansion into consumer lawn and garden applications.

FAQ's

The Smart Irrigation Market is estimated to reach $ 11.1 billion by 2034.

The Smart Irrigation Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 17.8% during the forecast period from 2026 to 2034.

The Smart Irrigation Market is estimated to generate $ 2.95 billion in revenue in 2026.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!