"The Sodium Reduction Ingredients Market is valued at $ 1.9 billion in 2025. Further, the market is expected to grow at a CAGR of 11.7% to reach $ 5.2 billion by 2034."

The sodium reduction ingredients market has gained significant traction over the past decade as public health initiatives and regulatory guidelines have spotlighted the link between high sodium intake and chronic conditions such as hypertension, cardiovascular disease, and kidney disorders. This market includes a variety of functional ingredients—such as potassium chloride, magnesium sulfate, yeast extracts, amino acids, and flavor enhancers—designed to replicate the salty taste in processed foods while lowering actual sodium content. The demand is driven by reformulation efforts across baked goods, snacks, sauces, ready meals, and dairy products. Food manufacturers are increasingly under pressure to comply with national sodium targets and meet growing consumer demand for healthier products without compromising flavor. As health awareness rises and consumers seek cleaner labels, sodium reduction ingredients are becoming a crucial part of product development pipelines in both mass-market and premium segments. The balance between taste preservation, affordability, and regulatory compliance is shaping innovation in this space, making it an integral focus for food and beverage companies worldwide.

In 2024, the sodium reduction ingredients market saw significant momentum due to a combination of health-driven consumer behavior, regulatory activity, and industry reformulation efforts. The implementation of government-led sodium reduction initiatives in countries such as the U.K., Canada, and India accelerated the adoption of alternative salts and taste enhancers. Food companies launched reformulated products across categories like soups, frozen meals, and savory snacks, many of which included potassium-based substitutes and fermentation-derived flavor modulators. New product development was particularly active in the plant-based and functional food segments, where health claims and nutrition labels play a key role in purchasing decisions. Technological advancements in masking agents also helped overcome the traditional metallic aftertaste associated with potassium chloride, making it more acceptable in mainstream applications. Ingredient suppliers introduced integrated sodium-reduction systems, offering customized blends tailored to specific product matrices and sensory profiles. At the same time, consumer education campaigns about hidden salt in processed foods gained visibility, pushing brands to make sodium reduction more prominent in their marketing. These developments marked a year of rapid progress in making sodium reduction both scalable and palatable.

Looking ahead to 2025 and beyond, the sodium reduction ingredients market is expected to evolve toward more holistic, multi-functional solutions that combine health benefits with flavor optimization. Ongoing research into umami enhancers, seaweed extracts, and enzyme-based salt reducers is likely to broaden the toolkit for food formulators. Consumer demand for “silent health” improvements—where nutrition enhancements are made without significant sensory or cost trade-offs—will push manufacturers to innovate with stealth nutrition strategies. Personalized nutrition and AI-assisted formulation may also play a role, enabling tailored sodium solutions based on product type and target demographics. As more countries introduce front-of-pack labeling and high-sodium warnings, food companies will intensify reformulation efforts to avoid negative visibility and maintain consumer trust. Clean-label alternatives that support sodium reduction without artificial additives will continue to see strong growth. However, challenges such as cost barriers, regulatory discrepancies across markets, and the sensory limitations of certain substitutes will require ongoing R&D investment. The future of this market lies in collaboration between food technologists, ingredient innovators, and public health stakeholders committed to reducing global sodium consumption without sacrificing consumer experience.

Key Trends in the Sodium Reduction Ingredients Market

- Rising awareness of the health risks of high sodium intake is the single biggest structural driver for sodium-reduction ingredients. Governments, health agencies, and advocacy groups are urging food companies to cut salt in everyday products such as bread, snacks, soups, and processed meat. This creates a sustained reformulation agenda rather than a short-term trend. As a result, sodium-reduction solutions move from niche to mainstream in core staple foods.

- Mineral salts such as potassium-based replacers remain the workhorse of sodium reduction in many categories. They offer relatively straightforward substitution in recipes while preserving key functional roles of salt such as preservation, texture, and processing behavior. However, taste challenges like bitterness or metallic notes drive demand for improved grades. This underpins innovation in blends, masking systems, and optimized usage levels.

- Flavor enhancers and modulators are emerging as crucial tools to maintain palatability in low-sodium products. Ingredients such as yeast extracts, umami boosters, and natural flavor systems help rebuild body and savory impact when salt is reduced. Their use is especially important in soups, sauces, ready meals, and meat products where flavor complexity matters. This drives a shift from simple salt replacement to sophisticated flavor architecture.

- Clean label and natural positioning strongly influence which sodium-reduction ingredients succeed with brand owners and consumers. Companies increasingly favor solutions perceived as familiar, minimally processed, and label-friendly. This benefits natural yeast extracts, vegetable concentrates, and fermentation-derived ingredients over highly synthetic additives. Suppliers that can combine efficacy with simple declarations gain a competitive edge in retail and foodservice channels.

- Application-specific solutions are becoming more important than one-size-fits-all sodium replacers. Bakery, snacks, processed meat, dairy, and beverages each have distinct functional and taste requirements. Leading suppliers therefore offer category-tailored systems that consider dough behavior, texture, color, shelf life, and flavor profile. Close application support and pilot-scale capabilities are key to winning reformulation projects.

- Regional regulations and voluntary targets shape market momentum across geographies. In some regions, formal sodium-reduction frameworks and front-of-pack labeling schemes push faster reformulation. Elsewhere, momentum comes more from multinational brand strategies and retailer standards than from strict rules. Sodium-reduction ingredient suppliers must adapt their portfolios and messaging to these different regulatory environments.

- Technical challenges in achieving deep sodium cuts without compromising taste and safety remain a critical restraint and innovation focus. Salt has multiple roles beyond flavor, including preservation, water binding, and texture. As reductions become more ambitious, simple partial substitution is not enough. This pushes development of multi-component systems combining mineral replacers, flavors, texturizers, and processing adjustments.

- Collaboration between ingredient companies and food manufacturers is intensifying as sodium reduction intersects with broader health and wellness reformulation. Many projects now aim to optimize salt, sugar, and fat simultaneously while preserving cost and consumer acceptance. Co-creation models, joint pilot plants, and long-term supply partnerships are increasingly common. This favors technically strong suppliers capable of integrated reformulation support.

- Cost, supply reliability, and scale are important considerations, especially for high-volume staples and value brands. Some advanced sodium-reduction systems can be significantly more expensive than standard salt, challenging adoption in price-sensitive markets. Companies seek solutions that deliver meaningful sodium cuts with minimal impact on total recipe cost. As volumes grow and production scales up, cost barriers are expected to ease for certain ingredient classes.

- Future growth is supported by ongoing shifts toward preventive healthcare, transparent labeling, and personalized nutrition. As consumers track daily sodium intake through apps and smart devices, demand rises for lower-sodium options across categories. This will encourage further innovation in highly effective, neutral-tasting, and label-friendly sodium-reduction ingredients. Over time, reduced-sodium formulations are likely to become the default rather than the exception in many packaged foods.

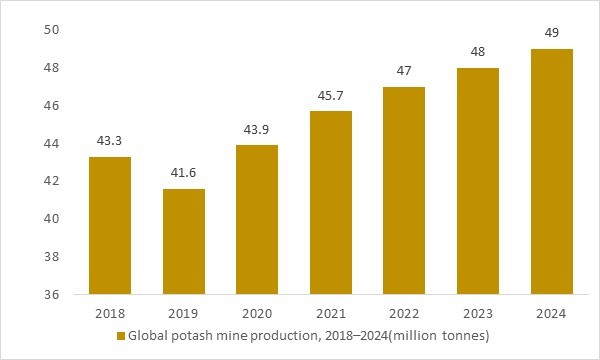

Global potash mine production (million tonnes)2018–2024

Figure: Global potash mine production has increased steadily from the low-40 million tonne range in 2018–2020 to higher levels in 2021–2024e, indicating a broader and more secure supply of potassium minerals. As a portion of this output is refined into food-grade potassium chloride, ingredient suppliers gain greater capacity to formulate reduced-sodium salts, seasonings and processed food systems. OG Analysis estimates, aligned with USGS and international mining data, emphasize how strengthening potash availability underpins the scalability of potassium-based sodium reduction solutions.

The sodium reduction ingredients market is gaining momentum as global potash production—used to produce potassium chloride for low-sodium formulations—has risen steadily from about 43 million tonnes in 2018 to an estimated 49 million tonnes in 2024e. This expanding potassium resource base strengthens the availability of KCl, enabling food manufacturers to reformulate products across snacks, bakery, meat, sauces and ready meals without sacrificing flavor. Increasing regulatory pressure to curb sodium intake and growing consumer interest in heart-healthy choices further accelerate adoption of potassium-based alternatives. As reformulation initiatives scale worldwide, the rising potash supply supports long-term growth and broader application of sodium reduction solutions.

Market Scope

| Parameter | sodium reduction ingredients Market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Type

- Mineral blend

- Amino Acid

- Yeast extracts

- Other Types

By Mineral Blend

- Potassium sulphate

- Magnesium sulphate

- Calcium chloride

- Potassium lactate

- Potassium chloride

By Application

- Bakery and Confectionery

- Dairy and frozen foods

- Meat products

- Sauces

- Snacks

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- Cargill Incorporated

- Angel Yeast Co. Ltd.

- Kerry Group plc

- Givaudan SA

- Innophos Holdings Inc.

- Tate & Lyle plc

- Biospringer

- Corbion NV

- Advanced Food Systems Inc.

- DuPont de Nemours Inc.

- Dr. Paul Lohmann GmbH & Co. KGaA

- K+S Kali GmbH

- Koninklijke DSM NV

- Ajinomoto Co. Inc.

- DSM Food Specialties BV

- Jungbunzlauer International AG

- Fufeng Group Company Limited

- Meihua Holdings Group Co. Ltd.

- Foodchem International Corporation

- Henan Jindan Lactic Acid Technology Co. Ltd.

- Qingdao Huifenghe MSG Co. Ltd.

- Shandong Qilu Biotechnology Group Co. Ltd.

- Saltwell AB

- Savoury Systems International

- Cambiaso Risso Group

- Salt of the Earth Ltd.

- Sensient Technologies Corporation

- Associated British Foods plc

- GNT Group B.V.

- Ingredion Incorporated

Sep 2025 — Meihua Holdings (China): In its 2025 semi-annual filing, Meihua disclosed that its Tongliao MSG capacity upgrade project reached full production, positioning it among the largest single-line MSG capacities globally—supportive for umami-led sodium-reduction reformulations.

Jul 2025 — Kerry: Kerry highlighted Tastesense™ Salt for sauces (with red/white/brown sauce-specific versions) to help brands cut sodium while restoring balance in taste, texture, and mouthfeel—showing continued application-led product development in salt-reduction systems.

Jul 2025 — Angel Yeast: At IFT FIRST 2025, Angel Yeast showcased its yeast extract savory range as a natural flavor enhancer explicitly positioned to enable umami-rich products while reducing sodium content.

Jun 2025 — Ajinomoto Health & Nutrition North America: Ajinomoto launched Salt Answer (sodium reduction) and Palate Perfect platforms, including four new Salt Answer ingredients tailored to key categories (snacks, sauces, dressings, etc.) for sodium reduction without major taste tradeoffs.

Apr 2025 — Fufeng Group: A new corn deep-processing industrial park project in Kazakhstan moved into construction, with planned output including monosodium glutamate and amino acids—a notable capacity diversification step for key savory/sodium-reduction-related ingredients.

May 2024 — Cargill: In its IFT FIRST 2024 prototype pack, Cargill featured reduced-sodium prototypes using Potassium Pro® ultra fine potassium salt alongside salt systems—signaling continued push on potassium-based sodium replacement for mainstream formulations.

Jun 2024 — Lesaffre / DSM-Firmenich: Lesaffre announced an agreement to acquire DSM-Firmenich’s yeast extract business, strengthening yeast-derivative capability (a key toolbox for sodium reduction via savory/umami building).

Apr 2024 — Kerry: Kerry introduced Tastesense™ Salt positioning it for meaningful sodium reduction (notably in savory applications like snacks) while maintaining salty impact—reinforcing fermentation/taste-modulation approaches in salt reduction.

FAQ's

The Global Sodium Reduction Ingredients Market is estimated to generate USD 1.9 billion in revenue in 2025.

The Global Sodium Reduction Ingredients Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 11.7% during the forecast period from 2025 to 2034.

The Sodium Reduction Ingredients Market is estimated to reach USD 5.2 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!