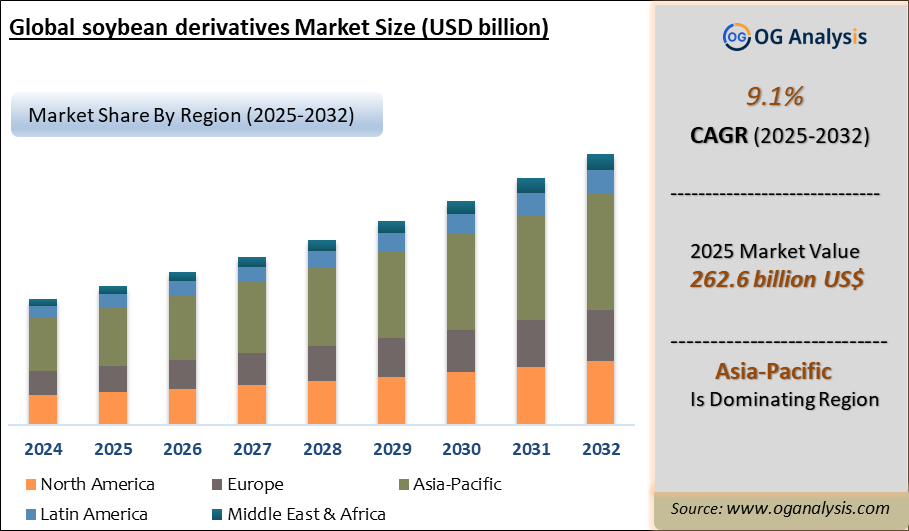

"The Soybean Derivatives Market is valued at $ 286.5 billion in 2026. Further, the market is expected to grow at a CAGR of 9.1% to reach $ 576 billion by 2034."

The Soybean Derivatives Market is a broad segment of plant-based ingredients, edible oils, animal feed materials, protein concentrates, food additives, bio-based chemicals, nutraceutical ingredients, and industrial raw materials, serving food and beverage, animal nutrition, pharmaceuticals, personal care, biodiesel, paints and coatings, plastics, adhesives, and industrial manufacturing applications. Soybean derivatives are obtained through crushing, extraction, refining, fermentation, hydrolysis, and further processing of soybeans into high-value products such as soybean oil, soybean meal, soy protein isolate, soy protein concentrate, textured soy protein, soy flour, lecithin, soy milk powder, soy peptides, soy isoflavones, soy wax, fatty acids, glycerin, methyl esters, and bio-based surfactants. These products are widely used in meat alternatives, bakery products, dairy substitutes, infant nutrition, functional foods, livestock feed, aquaculture feed, dietary supplements, emulsifiers, lubricants, biodiesel, cosmetics, and biodegradable materials. The market benefits from soybean’s strong protein profile, oil content, functional versatility, wide agricultural availability, and compatibility with both food-grade and industrial applications.

The market is gaining traction as food manufacturers, feed producers, biofuel companies, and consumer product brands increase their use of plant-based, renewable, high-functionality, and cost-efficient ingredients. Soybean meal remains a major demand base in animal feed, while soybean oil is widely used in edible oils, processed foods, biodiesel, oleochemicals, and personal care formulations. Soy protein derivatives are expanding through plant-based meat, sports nutrition, weight management products, vegan foods, and high-protein snacks. Lecithin continues to be important in chocolates, bakery, confectionery, pharmaceuticals, and cosmetics due to its emulsifying and stabilizing properties. Key trends include clean-label soy ingredients, non-GMO and organic soy derivatives, enzyme-modified soy proteins, sustainable sourcing, higher-value isolates and concentrates, biodiesel-linked oil demand, and improved extraction technologies. However, challenges include soybean price volatility, concerns over allergens, genetically modified crop acceptance, deforestation-linked sourcing risks, competition from pea and other plant proteins, regulatory restrictions, and trade disruptions. The competitive landscape includes oilseed processors, agribusiness companies, food ingredient suppliers, feed manufacturers, plant-protein companies, oleochemical producers, biodiesel producers, and specialty soy derivative manufacturers.

Regional Analysis

North America Soybean Derivatives Market

North America Soybean Derivatives Market is driven by strong soybean crushing capacity, animal feed demand, edible oil consumption, plant-based protein innovation, biodiesel and renewable diesel production, and industrial use of soy-based ingredients. The United States is the leading regional market, supported by integrated agribusiness companies, large-scale soybean farming, advanced oilseed processing, feed manufacturing, food ingredient production, and renewable fuel policies. Soybean meal remains widely used in poultry, swine, cattle, aquaculture, and pet food formulations, while soybean oil is increasingly important in edible oils, processed foods, oleochemicals, lubricants, and biofuel feedstock. Soy protein isolates, concentrates, lecithin, soy flour, and textured soy protein are gaining demand in meat alternatives, protein snacks, bakery, beverages, and functional foods. Growth opportunities are supported by plant-based diets, clean-label formulations, renewable fuels, high-protein foods, and sustainable sourcing programs. However, the region faces challenges from feedstock price volatility, weather-related crop risk, biofuel-driven oil demand pressure, and competition from other plant proteins. U.S. soybean oil demand is being strongly influenced by renewable fuel use.

Asia Pacific Soybean Derivatives Market

Asia Pacific Soybean Derivatives Market is one of the most important regional markets, supported by large livestock populations, rising meat and aquaculture consumption, expanding food processing, growing edible oil demand, and increasing use of plant-based proteins. China is the dominant demand center due to its large animal feed industry, soybean crushing activity, edible oil consumption, and processed food sector. India, Japan, South Korea, Indonesia, Vietnam, Thailand, and Australia also contribute through feed manufacturing, soy foods, nutraceuticals, bakery ingredients, dairy alternatives, and industrial applications. Soybean meal demand is closely tied to poultry, swine, dairy, and aquaculture growth, while soybean oil is used in cooking, packaged foods, and oleochemical applications. The region is also seeing growth in soy protein derivatives used in vegetarian foods, meat substitutes, beverages, sports nutrition, and affordable protein products. Opportunities are strong in plant-based foods, non-GMO soy ingredients, fortified foods, and feed efficiency solutions. Regional challenges include import dependency, trade policy shifts, price fluctuations, crop supply risk, and regulatory differences across countries. OECD-FAO outlooks identify oilseeds and oilseed products as a major long-term agricultural commodity category across production, consumption, trade, and price projections.

Europe Soybean Derivatives Market

Europe Soybean Derivatives Market is shaped by demand from animal feed, processed foods, plant-based meat alternatives, bakery, confectionery, pharmaceuticals, cosmetics, and sustainable industrial applications. Germany, France, the United Kingdom, Spain, Italy, the Netherlands, and Eastern European countries are key markets due to developed food manufacturing, livestock production, and strong interest in plant-based nutrition. Soybean meal remains important in animal feed, although the region continues to focus on responsible sourcing, traceability, deforestation-free supply chains, and partial substitution with local protein crops. Soy lecithin is widely used in chocolates, bakery products, infant nutrition, pharmaceuticals, and personal care, while soy proteins are gaining demand in vegan foods, dairy alternatives, ready meals, and high-protein snacks. Europe offers strong opportunities for non-GMO, organic, identity-preserved, and sustainably certified soy derivatives. However, strict regulatory requirements, allergen labeling, deforestation-related compliance, dependence on imported soy materials, and consumer preference for alternative plant proteins can constrain market expansion. EU-related soy supply chains remain highly sensitive to responsible sourcing and deforestation-risk exposure.

Middle East & Africa Soybean Derivatives Market

Middle East & Africa Soybean Derivatives Market is developing through demand from animal feed, edible oils, processed foods, bakery, confectionery, dairy alternatives, meat alternatives, cosmetics, and industrial applications. Gulf countries are important consumption centers due to food imports, livestock and poultry feed demand, processed food manufacturing, and rising interest in plant-based and functional foods. South Africa, Egypt, Nigeria, Kenya, and other African markets contribute through poultry feed, edible oil consumption, bakery ingredients, packaged foods, and local food processing. Soybean meal demand is supported by poultry and livestock growth, while soybean oil remains important in household cooking, foodservice, and packaged food production. Soy lecithin and soy proteins are gradually gaining use in confectionery, bakery, nutrition products, and specialty food formulations. Opportunities are emerging in feed security, fortified foods, affordable protein ingredients, halal-certified products, and local crushing or processing investments. Key challenges include import dependency, currency volatility, uneven processing infrastructure, logistics costs, climate-related supply risk, and price-sensitive purchasing across several African economies.

South & Central America Soybean Derivatives Market

South & Central America Soybean Derivatives Market is strongly supported by soybean cultivation, crushing, exports, animal feed demand, edible oil production, biodiesel, and food ingredient manufacturing. Brazil and Argentina are the leading regional markets, with Paraguay, Uruguay, Colombia, Chile, and other countries contributing through agriculture, livestock, feed, edible oil, and food processing activity. The region plays a strategic role in global soybean, soybean meal, and soybean oil supply, making it highly important for feed manufacturers, edible oil companies, biodiesel producers, and food ingredient suppliers. Soybean meal is widely used in poultry, swine, cattle, and aquaculture feed, while soybean oil is used in cooking oils, processed foods, biodiesel, oleochemicals, and industrial applications. Soy proteins, lecithin, and specialty derivatives are gaining demand in plant-based foods, bakery, confectionery, supplements, and personal care. Opportunities are supported by export-oriented crushing, renewable fuel programs, livestock expansion, and sustainable agriculture initiatives. However, deforestation concerns, logistics bottlenecks, weather volatility, policy shifts, and international trade dependency remain key challenges. USDA’s 2026 oilseeds outlook highlights Brazil and the United States as major contributors to soybean export growth.

Key Insights

- Soybean meal is one of the strongest demand drivers for the Soybean Derivatives Market. It is widely used in poultry, swine, cattle, aquaculture, and pet food formulations because of its protein content, amino acid profile, digestibility, and cost efficiency. Rising meat, dairy, egg, and aquaculture consumption continues to support steady demand from animal nutrition sectors.

- Soybean oil is an important demand contributor across edible and industrial applications. It is used in cooking oils, margarines, shortenings, processed foods, biodiesel, lubricants, coatings, printing inks, and personal care products. Its availability, functional stability, and suitability for further chemical processing make it one of the most commercially significant soybean derivatives.

- Soy protein ingredients are gaining momentum due to rising demand for plant-based nutrition. Soy protein isolate, soy protein concentrate, textured soy protein, and soy flour are used in meat alternatives, protein bars, beverages, bakery products, sports nutrition, infant foods, and vegetarian meals. Their ability to provide structure, texture, emulsification, and protein enrichment supports broad adoption.

- Plant-based meat and dairy alternatives are creating new opportunities for soy derivatives. Textured soy protein and soy isolates are used to replicate the bite, chewiness, and protein density of meat products, while soy-based ingredients support milk alternatives, yogurt substitutes, desserts, and ready-to-eat vegan foods. Product innovation is increasing demand from food manufacturers.

- Soy lecithin remains a high-value functional derivative due to its emulsifying, dispersing, stabilizing, and release-agent properties. It is widely used in chocolates, confectionery, bakery products, infant nutrition, pharmaceuticals, cosmetics, dietary supplements, and industrial formulations. Demand is supported by processed food production and preference for plant-derived emulsifiers.

- Biodiesel and renewable fuel demand are influencing soybean oil utilization. Soybean oil is increasingly used as a feedstock for biodiesel and renewable diesel production, particularly in markets pursuing lower-carbon fuel alternatives. This trend strengthens industrial demand but can also tighten availability and influence pricing for food-grade oil users.

- Non-GMO, organic, and identity-preserved soy derivatives are becoming more important in premium food and nutraceutical applications. Consumers and manufacturers are paying closer attention to sourcing, allergen control, traceability, sustainability claims, and clean-label positioning. These factors are encouraging suppliers to offer certified and segregated soy ingredient lines.

- Sustainability and responsible sourcing are critical competitive factors. Concerns around land use, deforestation, biodiversity impact, water use, and supply-chain transparency are encouraging food companies and processors to adopt certified soy sourcing, traceable procurement, regenerative agriculture initiatives, and supplier audits. Sustainability credentials increasingly affect customer selection and brand reputation.

- Competition from alternative plant proteins remains a key challenge. Pea protein, wheat protein, chickpea protein, fava bean protein, rice protein, and algae-based ingredients are gaining attention in some food and nutrition applications. Soy suppliers must continue improving flavor, texture, allergen management, clean-label appeal, and functionality to protect market share.

- Future market growth will be shaped by animal feed demand, plant-based food innovation, renewable fuel expansion, sustainable sourcing, functional ingredient development, and industrial bio-based applications. Companies offering integrated processing, reliable supply, high-purity derivatives, certified soy options, technical formulation support, and diversified food-feed-fuel portfolios are expected to remain competitive.

Market Scope

| Parameter | Soybean Derivatives Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Type, By Lecithin, By sales channel, By Application |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Type

- Soy Oil

- Soy Milk

- Soy meal

- Other Types

By Lecithin

- Water

- Acid

- Enzyme

By Sales Channel

- Departmental Stores

- Supermarkets

- Online Retail

- Other Channels

By Application

- Food And Beverages

- Feed Industry

- Others

- soy-based wood adhesives

- soy ink

- soy crayons

- soy-based lubricants and many more

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- Bunge Ltd

- Archer Daniels Midland and Company

- Louis Dreyfus Commodities B.V.

- Cargill Incorporated

- Wilmar International Limited

- Noble Group Ltd.

- AG Processing Inc.

- Cenex Harvest States Inc.

- DuPont Nutrition and Health

- Ruchi Soya Industries Limited

- Gavyadhar Organic Private Limited

- Terra Firma Organic Private Limited

- Ingredion Incorporated

- Calbee Inc.

- Solbar Industries Ltd.

- SunOpta Inc.

- Scoular Company

- Ceres Global Ag Corp

- American Natural Processors Inc.

- Iowa Soybean Processors (ISP)

- The Scoular Company

- Batory Foods

- Fuerst Day Lawson Holdings Limited

- Fuji Vegetable Oil Inc.

- Pilgrim's Pride Corporation

- Sojaprotein

- Arizona Grain Inc.

- Jiangsu Hongda New Material Co. Ltd.

- Cosucra

- Vippy Industries Ltd. .

Recent Developments

April 2026 – Bunge reported stronger performance from soybean and softseed processing and refining. The company stated that improved market conditions and strong execution supported its first-quarter performance, reinforcing the importance of soybean processing, soybean oil, meal, and related oilseed derivatives in food, feed, and fuel value chains.

April 2026 – Incobrasa Industries advanced its soybean processing expansion in Illinois. The expansion is expected to increase vegetable oil and animal feed production capabilities, strengthening regional supply of soybean oil, soybean meal, and biodiesel-linked derivatives for food, feed, and renewable fuel applications.

March 2026 – Bunge completed the acquisition of IFF’s soy crush, soy protein concentrate, and lecithin businesses. The transaction strengthened Bunge’s position in value-added soybean derivatives, particularly soy protein concentrates, lecithin, and crush-linked ingredient supply for food, feed, and industrial markets.

November 2025 – Louis Dreyfus Company inaugurated a specialty feed protein production line in Tianjin, China. The new line focuses on fermented soybean meal, supporting higher-value soy-based feed ingredients with improved digestibility, palatability, and animal nutrition performance.

August 2025 – ADM announced the streamlining of its soy protein production network. The company said it would leverage capacity at its recommissioned Decatur East facility and other global sites while ceasing operations at its Bushnell, Illinois facility, indicating a shift toward more efficient soy protein production assets.

July 2025 – Bunge completed its merger with Viterra. The combination created a larger global agribusiness platform with expanded capabilities across food, feed, fuel, oilseed processing, plant-based oils, fats, and proteins, strengthening Bunge’s role in global soybean derivative supply chains.

May 2025 – Louis Dreyfus Company inaugurated an automated specialty feed lecithin production line in Tianjin, China. The line expanded the company’s lecithin portfolio, including enzymatically treated and low-viscosity lecithin products for animal feed applications.

April 2025 – ADM confirmed the closure of its soybean processing plant in Kershaw, South Carolina. The decision reflected portfolio consolidation and changing crush economics, with implications for regional soybean meal, soybean oil, and crush-derived product supply.

FAQ's

The Global Soybean Derivatives Market is estimated to generate USD 286.5 billion in revenue in 2026.

The Global Soybean Derivatives Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 9.1% during the forecast period from 2026 to 2034.

The Soybean Derivatives Market is estimated to reach USD 576 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!