"The Space Exploration Technologies Market is valued at $ 653.5 Billion in 2026 and is projected to grow at a CAGR of 18.2% to reach $ 2489 Billion by 2034."

The Space Exploration Technologies Market encompasses launch vehicles, spacecraft, propulsion systems, satellites, robotic platforms, habitats, communication infrastructure, navigation technologies, scientific instruments, and ground-support systems developed for missions beyond Earth. Major applications include lunar and planetary exploration, space science, human spaceflight, in-orbit research, deep-space communications, resource prospecting, national security, and commercial transportation. Government space agencies, defense organizations, satellite operators, research institutions, launch-service providers, and private aerospace companies represent the principal end users. Market development is supported by renewed lunar exploration programs, growing commercial participation, increasing demand for scientific missions, and broader use of space-based infrastructure for communications, observation, navigation, and climate research.

Current trends include reusable launch systems, autonomous spacecraft operations, advanced electric and nuclear propulsion, in-space manufacturing, satellite servicing, and artificial intelligence-enabled mission management. Public-private partnerships are reducing development timelines and enabling companies to participate in missions previously led exclusively by governments. Competition includes established aerospace contractors, emerging launch companies, spacecraft manufacturers, robotics specialists, and technology startups competing through reliability, payload capacity, mission flexibility, cost efficiency, and engineering innovation. Expansion is driven by falling launch costs, improved miniaturization, stronger government funding, and growing strategic interest in lunar and deep-space capabilities. However, lengthy development cycles, mission failure risks, regulatory complexity, orbital congestion, radiation exposure, and supply-chain dependence on specialized components remain major challenges. Future market progress will increasingly depend on reusable architecture, international cooperation, commercial lunar services, advanced robotics, and sustainable space operations.

Key Insights

- Reusable launch vehicles remain one of the most important market developments because they reduce recurring launch costs and improve mission frequency. Manufacturers are advancing booster recovery, rapid refurbishment, and reusable upper-stage concepts. Higher launch cadence is enabling more scientific, commercial, and government missions. Reliability and turnaround time remain central competitive factors.

- Lunar exploration has become a major focus for government agencies and commercial companies developing landers, rovers, communication systems, navigation services, and surface infrastructure. Missions increasingly target scientific research, technology demonstration, crewed operations, and resource assessment. Commercial delivery services are creating new opportunities for specialized technology providers.

- Robotic spacecraft continue to dominate deep-space exploration due to their ability to operate in hazardous and distant environments. Orbiters, landers, rovers, probes, and sample-return systems support planetary science and resource mapping. Improved autonomy allows these platforms to make operational decisions with limited communication from Earth.

- Advanced propulsion technologies are receiving greater investment as mission planners seek faster travel, improved fuel efficiency, and higher payload capability. Electric propulsion is increasingly used for long-duration spacecraft operations, while nuclear and solar-thermal concepts are being evaluated for deep-space missions. Propulsion innovation will influence future mission range and duration.

- Artificial intelligence and autonomous navigation are transforming spacecraft control, image analysis, fault detection, and mission planning. Autonomous systems can respond to changing conditions without continuous ground intervention. These capabilities are particularly important for planetary missions where communication delays restrict real-time human decision-making.

- In-space servicing, assembly, and manufacturing are emerging as important commercial opportunities. Robotic platforms may inspect, repair, refuel, upgrade, or reposition satellites while additive manufacturing could support production of structures in orbit. These technologies can extend asset life and reduce dependence on fully assembled launches from Earth.

- Human spaceflight is creating demand for crew vehicles, habitats, life-support systems, radiation protection, spacesuits, and surface mobility solutions. Government-led programs are increasingly supported by commercial transportation and infrastructure providers. Long-duration missions will require improved reliability, closed-loop life support, and medical monitoring technologies.

- Competition is shifting toward integrated mission capabilities supported by launch, spacecraft, communications, data services, and ground operations. Established aerospace companies offer program-management experience, while emerging firms compete through faster development and specialized technologies. Long-term success will depend on funding access, technical reliability, partnerships, and regulatory compliance.

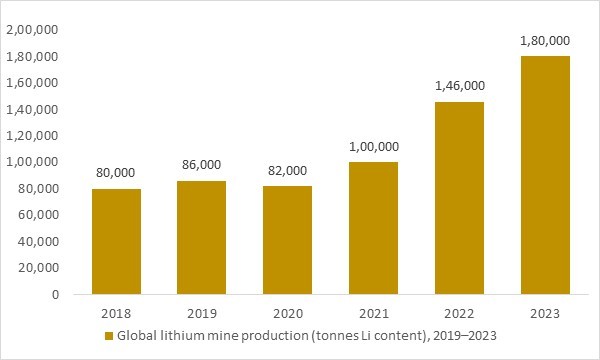

Global lithium mine production (tonnes Li content), 2019–2023

Figure: Global lithium mine production has more than doubled since 2019, reflecting rapid growth in battery materials supply. This expanding lithium base is critical for advanced space exploration technologies that rely on high-energy lithium-ion batteries in satellites, launch systems, rovers and deep-space missions.

- The development of space exploration technologies is increasingly tied to the availability of high-energy battery materials. Lithium, a critical input for lithium-ion batteries used in satellites, crewed spacecraft, rovers and ground segment power systems, has seen rapid growth in global mine output. According to the U.S. Geological Survey, world lithium mine production (excluding the United States) increased from roughly 86 thousand tons of lithium content in 2019 to around 180 thousand tons in 2023. This more than doubling of supply in just four years underscores the scale of upstream investment into battery materials, providing a broader industrial foundation for the next generation of all-electric satellites, deep-space missions and surface power systems that underpin the space exploration technologies market.

Regional Analysis

North America Space Exploration Technologies Market

North America leads the Space Exploration Technologies Market, supported by extensive government programs, advanced private-sector participation, strong defense investment, and a mature aerospace supply chain. The United States drives regional development through lunar exploration, planetary science, human spaceflight, reusable launch systems, deep-space communications, and commercial space transportation. Public-private partnerships are accelerating the development of landers, spacecraft, propulsion systems, robotic platforms, habitats, and in-orbit services. The region also benefits from strong venture funding, research institutions, launch infrastructure, and specialized component manufacturers. Growing focus on reusable architectures, autonomous spacecraft, commercial lunar services, and national security missions is expected to sustain regional leadership.

Europe Space Exploration Technologies Market

Europe maintains a significant market position through established space agencies, aerospace manufacturers, research institutions, and multinational exploration programs. France, Germany, Italy, the United Kingdom, Spain, and several Nordic countries contribute to launch systems, scientific instruments, propulsion technologies, satellite platforms, robotics, and ground infrastructure. Regional companies participate extensively in lunar missions, planetary observation, Earth science, space telescopes, and international human-spaceflight programs. Europe is also strengthening investment in independent launch access, reusable technologies, sustainable propulsion, and space-debris management. Regulatory coordination, fragmented funding structures, and dependence on international partnerships can affect program timelines, although collaborative capabilities remain a major regional advantage.

Asia-Pacific Space Exploration Technologies Market

Asia-Pacific is experiencing rapid development, driven by expanding national space programs, growing launch capabilities, technological self-reliance, and rising commercial participation. China, India, Japan, South Korea, and Australia are among the key regional markets. Major activities include lunar and planetary missions, reusable launch-vehicle development, sample-return programs, space-station operations, robotic exploration, and deep-space observation. Governments are increasing investment in domestic manufacturing, propulsion, navigation, communication, and scientific payload technologies. Emerging private companies are also developing small launch vehicles, lunar platforms, and in-space services. Expanding research capabilities and lower-cost engineering are strengthening the region’s role in global exploration missions.

Middle East & Africa Space Exploration Technologies Market

The Middle East & Africa market is developing gradually, supported by government diversification strategies, international partnerships, scientific research initiatives, and growing investment in domestic space capabilities. The United Arab Emirates, Saudi Arabia, Israel, and South Africa represent important regional participants. Regional programs increasingly focus on lunar exploration, planetary science, satellite development, astronaut missions, space research, and ground-station infrastructure. Partnerships with established global agencies and aerospace companies provide access to technical expertise and mission experience. Limited domestic manufacturing, specialist workforce constraints, and reliance on imported technologies remain key challenges, although education programs and sovereign investment are improving the long-term outlook.

South & Central America Space Exploration Technologies Market

South & Central America represents an emerging market, with activity concentrated in Brazil, Argentina, Mexico, Chile, and selected smaller economies. Regional demand is primarily associated with satellite technologies, scientific research, launch-site development, ground stations, Earth observation, and participation in international exploration programs. Brazil has the strongest aerospace manufacturing and launch infrastructure, while Argentina contributes through satellite engineering and scientific capabilities. Strategic geographic locations also provide opportunities for tracking stations and equatorial launch services. Budget limitations, political uncertainty, and dependence on foreign technology restrict large-scale exploration programs, encouraging countries to pursue collaborative missions, research partnerships, and specialized technology development.

Report Scope

| Parameter | Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Technology Type, By Application, By End use |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Technology Type

- Launch Vehicles

- Spacecraft

- Satellites

- Space Stations

By Application

- Communication

- Earth Observation

- Scientific Research

- Space Tourism

- National Security

By End User

- Government

- Commercial

- Research Organizations

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Major Players in the Space Exploration Technologies Market

1. SpaceX

2. Blue Origin

3. Rocket Lab

4. Northrop Grumman Corporation

5. Lockheed Martin Corporation

6. Boeing Defense, Space & Security

7. Airbus Defence and Space

8. Virgin Galactic

9. Sierra Nevada Corporation

10. Thales Alenia Space

11. Maxar Technologies

12. Relativity Space

13. Planet Labs

14. OneWeb

15. United Launch Alliance (ULA)

Recent Developments

- June 2026 – NASA selected 41 proposals from 37 companies to advance space transportation, lunar power generation, navigation, landing systems, in-space servicing, and planetary-surface technologies supporting sustained Moon and Mars exploration.

- June 2026 – Rocket Lab was selected to provide three dedicated Electron launches for NASA science missions, while also preparing its Photon spacecraft for the LOXSAT in-space refueling technology demonstration supporting future lunar and Mars missions.

- June 2026 – JAXA and its partners published the lunar demonstration results of the LEV-2 transformable rover, confirming autonomous deployment, movement, image selection, and data transmission by an ultra-compact robotic platform on the Moon.

- May 2026 – NASA advanced its Moon Base strategy by announcing upcoming commercial lander missions and awarding Astrolab and Lunar Outpost contracts to develop crewed and remotely operated lunar terrain vehicles for surface mobility.

- April 2026 – NASA completed the Artemis II crewed lunar flyby, validating the Space Launch System, Orion spacecraft, deep-space life-support systems, manual piloting capabilities, re-entry systems, and international mission architecture.

- March 2026 – NASA announced plans to accelerate commercial lunar payload services toward a higher cadence of robotic landings while advancing nuclear electric propulsion and surface infrastructure technologies for future Moon and Mars exploration.

- January 2026 – Blue Origin announced that it would pause New Shepard flights and redirect resources toward accelerating the development of its human lunar transportation and exploration capabilities.

- November 2025 – Blue Origin’s New Glenn successfully deployed NASA’s ESCAPADE twin spacecraft and landed its reusable first-stage booster, demonstrating heavy-lift launch and recovery capabilities for planetary exploration missions.

- September 2025 – Blue Origin’s Blue Alchemist lunar resource-utilization system completed its Critical Design Review, advancing technology designed to convert lunar regolith into oxygen, metals, construction materials, and solar-power components.

- July 2025 – Firefly Aerospace received a NASA contract for a lunar south-pole mission using its Blue Ghost lander and Elytra orbital vehicle to deploy rovers, investigate lunar resources, and provide long-duration communications and imaging services.

FAQ's

The Space Exploration Technologies Market is estimated to reach $ 2943.1 Billion by 2034.

The Space Exploration Technologies Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 18.2% during the forecast period from 2026 to 2034.

The Space Exploration Technologies Market is estimated to generate $ 772.4 Billion in revenue in 2026.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!