"The Space Robotic Solutions Market was valued at $ 6.6 billion in 2026 and is projected to reach $ 12.7 billion by 2034, growing at a CAGR of 8.5%."

The space robotic solutions market is a rapidly growing segment of the space industry, driven by advancements in automation, artificial intelligence (AI), and robotics. Space robots are used for a variety of applications, including satellite servicing, space exploration, assembly of space infrastructure, and debris removal. The market is characterized by robotic systems designed to operate in harsh environments, performing tasks such as robotic arm movements, precision manipulations, autonomous navigation, and data collection. Companies and space agencies are increasingly focusing on autonomous robotic systems that can perform complex missions without human intervention, reducing costs and risks associated with human spaceflight. Space robotics plays a critical role in expanding the capabilities of spacecraft and space stations, supporting deep space missions, and addressing emerging space sustainability concerns, such as satellite maintenance and debris management. The increasing interest in the commercialization of space and the planned human missions to the Moon and Mars are expected to fuel further growth in the space robotics market.

In 2024, the space robotic solutions market saw significant advancements with the successful deployment of robotic systems in a variety of space missions. Space agencies such as NASA and ESA made substantial investments in robotic solutions for tasks such as servicing defunct satellites, collecting space debris, and even assembling space structures in orbit. Robotic arms, such as those used in the Canadarm2 system on the International Space Station (ISS), were further enhanced for autonomous operations. In addition, robotic solutions for lunar exploration, such as lunar rovers and autonomous robotic miners, were actively developed for NASA's Artemis program. Companies like Astrobotic and Orbit Fab also worked on technologies for in-orbit servicing and resource gathering. The year marked key milestones in demonstrating the capabilities of space robotics for long-term space exploration and commercialization, with several successful test runs in satellite servicing and autonomous space operations. The use of AI-driven robots that can make decisions in real time on autonomous tasks without the need for human intervention was a key focus in 2024.

Looking ahead to 2025 and beyond, the space robotic solutions market is expected to evolve with a focus on more advanced, autonomous, and multifunctional robots. The demand for in-orbit servicing robots, capable of refueling, repairing, and upgrading satellites, will increase as satellite constellations expand. These robots will also play a vital role in the planned Moon and Mars missions, where they will support construction and maintenance of infrastructure such as lunar habitats, solar power stations, and resource extraction systems. Robotics will also be crucial for space tourism, where robots will assist with passenger safety, transportation, and maintenance. AI and machine learning algorithms will enable robotic systems to become more intelligent and adaptable, allowing them to perform increasingly complex and critical tasks autonomously. Moreover, the use of robots for space debris removal is likely to become more widespread, addressing the growing issue of space traffic management. However, technical challenges such as the development of highly reliable and cost-effective robotic systems for deep space missions will continue to need attention as the industry moves forward.

Key Insights

- Space robotics evolved from niche technology demonstrators to mission-critical tools for orbiting platforms and planetary exploration, establishing a strong legacy of reliability in harsh environments. This historic track record underpins current confidence in deploying more complex, autonomous robotic systems for servicing, assembly, and surface operations across multiple orbits and bodies.

- On-orbit servicing and life-extension missions are emerging as a flagship application, using robotic arms, docking mechanisms, and guidance systems to refuel, reposition, or repair satellites. By protecting high-value assets and deferring replacement launches, these solutions create a compelling economic rationale for both commercial operators and government customers.

- The growing focus on space sustainability and debris mitigation is catalyzing demand for inspection and debris-removal robots capable of rendezvous, capture, and controlled deorbit of non-cooperative objects. This drives innovation in relative navigation, autonomous approach, and adaptable end-effectors, while opening new service categories in an evolving regulatory framework.

- Lunar and planetary surface robotics represent a key growth frontier, with rovers, lander-mounted manipulators, and construction robots supporting science, resource mapping, and infrastructure preparation for future human missions. The need for ruggedized hardware, power-efficient locomotion, and long-duration autonomy underpins sustained investment in specialized robotic platforms.

- Advances in autonomy, artificial intelligence, and machine vision are enabling space robots to perform more complex tasks with reduced ground-control intervention. Enhanced onboard processing, cooperative behaviors, and intelligent path-planning are central to lowering operations cost, shortening response times, and unlocking new mission concepts such as swarms and distributed robotic systems.

- In-orbit assembly and manufacturing are emerging as transformative use cases, relying on robotic systems to build and maintain large structures such as antennas, telescopes, and future power or habitation platforms. Modular robotic architectures and standardized interfaces allow systems to be reconfigured for multiple tasks, improving asset utilization and scalability.

- The commercialization of low Earth orbit and the expansion of satellite constellations are reshaping demand patterns for robotic inspection and servicing. Operators seek standardized, rapidly deployable robotic payloads and hosted solutions that integrate with existing satellite buses, enabling more flexible maintenance and logistics concepts over the satellite lifecycle.

- Competitive dynamics are shifting as agile start-ups and specialized robotics companies enter alongside established aerospace integrators, leading to a diverse mix of offerings. Partnerships, joint ventures, and public–private collaboration are common as players combine space heritage, robotics know-how, software capabilities, and access to launch and mission operations infrastructure.

- Regulatory, legal, and insurance frameworks for in-orbit servicing, debris removal, and proximity operations remain in evolution, influencing adoption and business models. Clear norms around ownership, liability, safety corridors, and data sharing will be critical to unlock scaled deployment of space robotic services and encourage private investment in new capabilities.

- Standardization, modularity, and interoperable interfaces are becoming strategic themes, as stakeholders seek to avoid bespoke designs for every mission. Common docking systems, robotic tool interfaces, software frameworks, and test protocols will lower integration barriers, reduce costs, and support a more robust ecosystem of compatible space robotic solutions and services.

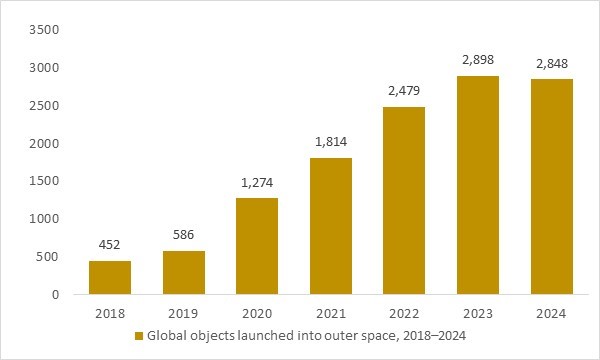

Global objects launched into outer space, 2018–2024

Figure: Global objects launched into outer space have risen steadily from earlier years through 2024e, creating an increasingly dense and operationally complex orbital environment that directly amplifies the need for autonomous space robotic systems. As more satellites, mega-constellations and mission payloads are deployed across low, medium and geostationary orbits, operators require robotic platforms capable of inspection, servicing, assembly, refuelling and debris-removal to maintain asset longevity and orbital safety. Expanding launch activity, particularly from commercial space firms and national space agencies, strengthens demand for radiation-hardened sensing, precision manipulation and autonomous navigation technologies integrated into space-robotic solutions. OG Analysis estimates, derived from international space-object registries and global space-traffic studies, demonstrate how rising orbital population enhances long-term opportunities in on-orbit servicing, robotic maintenance and advanced space-safety infrastructure.

The Space Robotic Solutions Market is rapidly expanding as the number of objects launched into outer space continues to climb each year, creating a larger and more complex orbital environment. The growth of satellites, mega-constellations and deep-space missions is driving demand for robotic systems capable of inspection, servicing, refuelling, assembly and debris-removal. As operators prioritize safety, asset longevity and congestion management, autonomous robotic platforms equipped with advanced sensing and radiation-hardened monitoring technologies are becoming essential. This accelerating activity in Earth orbit strengthens long-term opportunities for innovative, on-orbit robotic solutions across commercial, government and defense sectors.

Market Scope

| Parameter | Space Robotic Solutions Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Solution, By Application, By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Space Robotic Solutions Market Segmentation

By Solution

- Remotely Operated Vehicles

- Remote Manipulator System

- Software

- Services

By Application

- Deep Space

- Near Space

- Ground

By End User

- Commercial

- Government

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Major Companies Analysed

Northrop Grumman Corporation, Oceaneering International Inc., Maxar Technologies Inc., iRobot Corporation, MDA Space and Robotics Ltd., Redwire Corporation, Astroscale Holdings Inc., Intuitive Machines LLC., AMP Robotics Corp., Olis Robotics Inc., D-Orbit SpA, Tethers Unlimited Inc., ClearSpace SA, Exyn Technologies Inc., Astrobotic Technology Inc., Tethers Unlimited Inc., Space Applications Services NV/SA, Metecs LLC., BluHaptics Inc., Motiv Space Systems Inc., Altius Space Machines Inc., Bradford Space Inc., Kubos Corporation, Oceaneering Space Systems Inc., Ubotica Technologies Ltd.

Recent Industry Developments

April 2026 – Astroscale unveiled ISSA-J1 as the world’s first commercial multi-orbit satellite inspection mission. The robotic servicing spacecraft is designed to inspect two retired Japanese satellites in different orbital regimes, expanding the commercial case for on-orbit robotic inspection services.

March 2026 – Intuitive Machines announced a major NASA CLPS award expansion tied to wider lunar surface operations. The IM-5 mission will carry Honeybee Robotics’ next-generation lunar rover, reinforcing demand for robotic mobility, autonomy, and science-support systems on the Moon.

March 2026 – Astrobotic announced it was awarded a contract by Thales Alenia Space to develop a lunar wheel assembly for the Italian Space Agency’s Multi-Purpose Habitation system. The work strengthens Astrobotic’s position in robotic mobility solutions for sustained lunar surface operations.

January 2026 – Astroscale UK announced an ESA contract to study a world-first in-orbit refurbishment and upgrading service. The program focuses on robotic and servicing technologies that could connect with satellites in orbit and replace degraded subsystems, moving robotic solutions beyond inspection into repair and upgrade services.

July 2025 – MDA Space announced that its team was selected for Canada’s Lunar Utility Vehicle study. The company said the effort will use its SKYMAKER robotics and autonomy technologies to support scalable lunar mobility and logistics operations.

June 2025 – Astrobotic announced that CubeRover-1 completed its acceptance test campaign and was declared flight-ready for Griffin Mission One. The milestone advanced one of the sector’s most visible lightweight robotic mobility platforms for lunar science and payload transport.

March 2025 – GITAI announced that JAXA awarded it a concept study contract for a robotic arm on Japan’s crewed pressurized lunar rover. The arm is being designed for excavation, sample collection, payload handling, and autonomous science support during lunar missions.

March 2025 – Firefly Aerospace and Honeybee Robotics announced that Honeybee will provide the rover for Firefly’s lunar mission to the Gruithuisen Domes. The agreement highlights growing demand for integrated robotic mobility solutions as a core element of commercial lunar exploration missions.

FAQ's

The Global Space Robotic Solutions Market is estimated to generate USD 6.6 billion in revenue in 2026.

The Global Space Robotic Solutions Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% during the forecast period from 2026 to 2034.

The Space Robotic Solutions Market is estimated to reach USD 12.7 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!