"The Global Specialty Chemicals Market was valued at $ 713.88 billion in 2025 and is projected to reach $1128 billion by 2034, growing at a CAGR of 5.22%."

The specialty chemicals market comprises a broad spectrum of high-value, performance-driven chemical products used across industries such as automotive, agriculture, construction, electronics, personal care, and pharmaceuticals. Unlike commodity chemicals, specialty chemicals are formulated to deliver specific functions, such as corrosion inhibition, UV stabilization, emulsification, or adhesion. Their usage is often characterized by low volume but high value, with customized applications tailored to end-user requirements. The market is driven by innovation, R&D investment, and industry-specific technological advancements that enable high-performance formulations. The shift toward green chemistry, bio-based alternatives, and environmental compliance has also shaped new product development trends in this sector. As a result, specialty chemicals play an essential role in enabling product differentiation and efficiency across a wide range of industrial and consumer applications.

Market growth is being fueled by expanding middle-class consumption, industrial expansion, and technological evolution across both emerging and developed economies. In sectors like automotive and electronics, specialty chemicals are integral to lightweighting, thermal management, and miniaturization trends. In agriculture, they improve crop yield and soil health through advanced agrochemical formulations, while in personal care, demand for sustainable and multifunctional ingredients continues to rise. Asia Pacific remains the fastest-growing region, driven by manufacturing shifts and domestic consumption growth. Meanwhile, North America and Europe are witnessing growth through innovation-led value creation and product customization. The increasing focus on sustainable supply chains, regulatory alignment, and digital integration is creating new opportunities for companies offering advanced material science, eco-conscious production, and application-specific chemical solutions.

Key Market Insights

-

The specialty chemicals market is driven by demand for performance-enhancing solutions across industries such as automotive, construction, personal care, and electronics. These chemicals are tailored for specific applications, offering advantages such as durability, thermal stability, corrosion resistance, and formulation flexibility.

-

Innovation is at the core of market competitiveness, with companies investing heavily in R&D to develop high-functionality and environmentally compliant products. Tailored formulations and value-added functionalities are enabling manufacturers to differentiate in highly fragmented end-user markets.

-

Asia Pacific continues to dominate the specialty chemicals landscape due to robust industrialization, expanding consumer markets, and regional production capabilities. Countries like China, India, and South Korea are witnessing increased consumption of specialty chemicals across automotive, agriculture, and packaging sectors.

-

Sustainability is reshaping the product development pipeline, with companies shifting toward bio-based, biodegradable, and low-VOC formulations. Stringent regulatory frameworks in North America and Europe are accelerating adoption of green chemistry and eco-friendly raw materials.

-

Specialty polymer demand is rising across electronics and healthcare applications, where high-performance materials are needed for miniaturized devices, medical implants, and flexible electronics. These applications require precise chemical performance under varying environmental conditions.

-

The agricultural sector is increasingly relying on specialty agrochemicals to enhance crop yields, pest control efficiency, and soil health. Precision agriculture practices are driving demand for controlled-release fertilizers, micronutrients, and biostimulants designed for targeted outcomes.

-

Personal care and cosmetics segments are experiencing strong growth for specialty ingredients that offer multifunctional properties such as moisturization, UV protection, and anti-aging. Consumer preference for clean-label and dermatologically safe products is shaping formulation trends.

-

Construction chemicals, including admixtures, sealants, waterproofing agents, and protective coatings, are seeing increased usage in infrastructure development and urbanization projects. These materials are critical for enhancing structural integrity and durability in diverse climate zones.

-

Digitalization in specialty chemical production is enabling real-time process monitoring, predictive quality control, and supply chain optimization. Smart manufacturing practices are improving consistency, reducing waste, and shortening time-to-market for customized products.

-

Strategic mergers, acquisitions, and joint ventures are reshaping the competitive landscape, with companies aiming to expand their portfolio, geographic reach, and application expertise. These moves are helping firms gain access to emerging markets and specialized product segments.

Regional Insights

North America Specialty Chemicals Market

North America maintains a mature specialty chemicals industry, with strong applications in electronics, water treatment, personal care, and agriculture driving market demand. Companies here are focusing on developing eco-friendly and high-performance formulations to meet sustainability goals and consumer preferences. The push for digitalization and supply chain resilience is fostering opportunities in smart manufacturing and localized production. Industry consolidation is accelerating as firms explore mergers and acquisitions to optimize portfolios and capitalize on efficiencies in fragmented segments. Despite soft industrial demand and macroeconomic uncertainty slowing growth, strategic investors remain optimistic about M&A-led transformation to position companies for long-term resilience.

Asia Pacific Specialty Chemicals Market

Asia Pacific is the fastest-growing and largest region for specialty chemicals demand, underpinned by rapid urbanization, rising manufacturing output, and expanding consumer markets across economies such as China, India, and Southeast Asia. Regional demand is particularly robust in personal care, agrochemical formulations, and electronic-grade specialty additives. Governments are providing regulatory support and infrastructure to fuel sector growth, encouraging local production and tailored offerings. The increasing demand for high-performing, clean-label ingredients is an opportunity for firms that can swiftly deliver scalable, customized solutions. Additionally, regional chemical hubs are strengthening with investments in R&D and production capacity to serve both domestic needs and export markets.

Europe Specialty Chemicals Market

Europe's specialty chemicals sector is being reshaped by stringent environmental regulations, energy cost challenges, and growing competition from lower-cost producers in Asia and the Middle East. While regulatory complexity demands product innovation, it also presents an opening for companies specializing in sustainable chemicals, recycled feedstock solutions, and low-carbon processes. The continent is seeing asset restructuring and consolidation as companies weigh strategic divestments to refocus on core competencies and improve capital efficiency. The trend towards clean chemistry and circular industrial models is creating niche opportunities for skillful players offering compliance-ready, differentiated specialty chemical solutions.

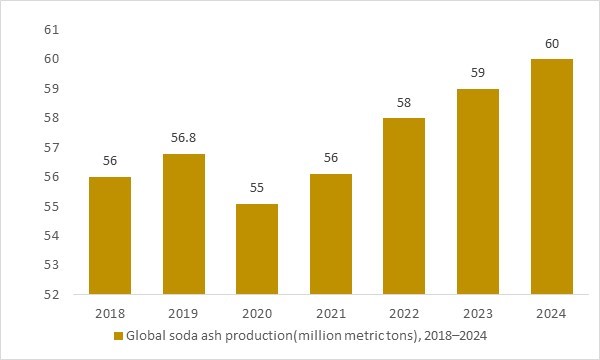

Global soda ash production(million metric tons), 2018–2024

Figure: Global soda ash production increased from around 56 million tonnes in 2018 to an estimated 60 million tonnes in 2024, reflecting steady expansion of glass, detergents and sodium-based intermediates. This rising base chemical output underpins broader demand for specialty formulations, including surfactant builders, process aids and performance additives across industrial and cleaning applications. At the same time, soda ash–driven glass and chemical infrastructure supports specialty glass and process chemistries used in radiation-shielding windows, detector housings and nuclear facilities, reinforcing the link between specialty chemicals and the growing radiation-detection, monitoring and security market.

Global soda ash production has increased from around 56 million tonnes in 2018 to an estimated 60 million tonnes in 2024, signalling steady expansion in glass, detergents, water-treatment and sodium-based intermediates. This rising output underpins demand for a wide range of specialty chemicals used as surfactant builders, process aids, buffers and performance additives across cleaning, industrial and environmental applications. At the same time, soda ash–driven glass and chemical capacity supports specialty glass for shielding windows, detector housings and optical components used in radiation-detection and monitoring systems. As the world’s soda ash base inches upward, it reflects a broader growth in glass and chemical infrastructure, deepening the installed asset base that relies on both specialty chemicals and radiation-detection, monitoring and security solutions.

Report Scope

| Parameter | specialty chemicals market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Type,By Product ,By End-user |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Specialty Chemicals Market Segmentation

By Type

- Plasticizers

- Water-based

- Coagulants and flocculants

- Scale inhibitors

By Product

- Institutional & Industrial Cleaners

- Rubber Processing Chemicals

- Food & Feed Additives

- Cosmetic Chemicals

- Oilfield Chemicals

By End-user

- Agrochemicals

- Lubricant and oilfield chemicals

- Adhesives and sealants

- Industrial and institutional cleaners

- Others

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Companies Covered

BASF, Dow, DuPont, Evonik Industries, Clariant, Solvay, Huntsman Corporation, Akzo Nobel, LANXESS, Croda International, Albemarle Corporation, Ashland Global, Eastman Chemical, Wacker Chemie, Kemira

Recent Industry Developments

-

June 2025: Hindalco announced the acquisition of the US‑based AluChem Companies, aiming to strengthen its specialty alumina portfolio and push toward its goal of scaling production significantly by FY2030.

-

June 2025: Aditya Birla Chemicals confirmed its acquisition of Cargill’s specialty chemical manufacturing facility in Dalton, Georgia, marking a strategic expansion into the U.S. advanced materials sector.

-

May 2025: Safex Chemicals inaugurated its largest-ever manufacturing plant in Bharuch, Gujarat, to enhance supply chain efficiency and expand availability of crop protection formulations across key Indian agricultural markets.

-

June 2025: DCM Shriram received board approval to acquire Hindusthan Specialty Chemicals, signaling its strategic entry into the advanced materials and specialty chemicals space.

-

April 2025: Clariant reported stronger‑than‑expected Q1 results fueled by growth in care chemicals, absorbents, and additives, reaffirmed its medium‑term targets, and announced a CFO transition effective August.

-

May 2025: Nelson Brothers LLC outlined a $19.4 million expansion in Alabama to enhance specialty chemical capabilities, including a new technical center and increased reactor capacity to serve diverse markets.

Who can benefit from this research

The research would help top management/strategy formulators/business/product development/sales managers and investors in this market in the following ways

1. The report provides 2024 Specialty Chemicals market sales data at the global, regional, and key country levels with a detailed outlook to 2034, allowing companies to calculate their market share and analyze prospects, uncover new markets, and plan market entry strategy.

2. The research includes the Specialty Chemicals market split into different types and applications. This segmentation helps managers plan their products and budgets based on the future growth rates of each segment

3. The Specialty Chemicals market study helps stakeholders understand the breadth and stance of the market giving them information on key drivers, restraints, challenges, and growth opportunities of the market and mitigating risks

4. This report would help top management understand competition better with a detailed SWOT analysis and key strategies of their competitors, and plan their position in the business

5. The study assists investors in analyzing Specialty Chemicals business prospects by region, key countries, and top companies' information to channel their investments.

FAQ's

The Global Specialty Chemicals Market is estimated to generate USD 713.88 billion in revenue in 2025.

The Global Specialty Chemicals Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 5.22% during the forecast period from 2025 to 2034.

The Specialty Chemicals Market is estimated to reach USD 1128 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!