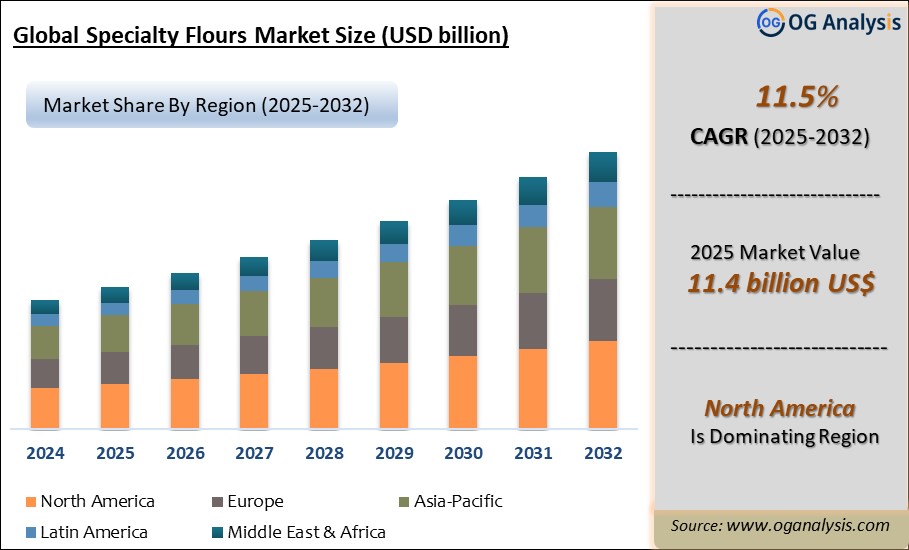

"Global Specialty Flours Market is valued at USD 11.4 billion in 2025. Further, the market is expected to grow at a CAGR of 11.5% to reach USD 30.4 billion by 2034."

The Specialty Flours Market comprises flours produced from non-traditional grains, legumes, nuts, and seeds or processed through unique techniques to enhance nutritional, functional, and sensory properties. It includes gluten-free flours (rice, chickpea, almond), high-protein flours (pea, lentil), sprouted flours, and fortified or enriched variants tailored for bakery, snacks, pasta, infant nutrition, and health supplements. Market growth is driven by rising consumer awareness of gluten intolerance, celiac disease, and dietary diversification, along with increasing demand for clean-label, high-fiber, and protein-rich formulations. Food manufacturers are adopting specialty flours to create premium, functional, and allergen-free products that align with evolving health and wellness trends globally.

North America and Europe lead the market due to widespread gluten-free adoption, strong health food cultures, and innovation in bakery and snack segments. Asia-Pacific is emerging as the fastest-growing market, driven by rising urban health awareness, traditional use of legume flours, and growing premium bakery consumption in India, China, and Southeast Asia. Challenges include higher production costs, supply chain complexities, and functional differences in processing versus wheat flour. However, advances in milling technologies, supply chain integration, and formulation expertise are expanding market potential. With increasing consumer focus on plant-based, ancient grain, and allergen-free diets, specialty flours are set to grow across retail, foodservice, and industrial applications worldwide.

The conventional segment is the largest in the specialty flours market due to its widespread availability, cost-effectiveness, and established consumer preference across both household and industrial applications. Conventional specialty flours are commonly used in baking, snacks, and processed foods on a large scale.

The online retail segment is the fastest-growing distribution channel, fueled by increasing digital penetration, convenience of home delivery, and rising demand for niche and gluten-free specialty flours. E-commerce platforms offer broader product selection and target health-conscious consumers more effectively.

Key Insights

- Gluten-free flours such as rice, almond, coconut, and buckwheat are witnessing strong demand in bakery, confectionery, and snack products targeting celiac and health-conscious consumers.

- High-protein flours from peas, lentils, chickpeas, and soybeans are gaining traction in protein-enriched pastas, bakery products, and meal replacements due to rising plant-based diets.

- Sprouted grain flours are emerging for their improved digestibility, bioavailability of nutrients, and unique flavor profiles, particularly in artisanal breads and health supplements.

- Ancient grain flours such as quinoa, amaranth, teff, and sorghum are incorporated into bakery, breakfast cereals, and baby food for their nutritional density and gluten-free benefits.

- Nut-based flours including almond, hazelnut, and cashew are widely used in gluten-free bakery, keto-friendly products, and confectionery for their rich taste and low-carb profile.

- Functional specialty flours enriched with omega-3, fiber, or vitamins are being developed to support immunity, digestive health, and cognitive wellness in health-oriented products.

- Asia-Pacific market growth is driven by traditional use of chickpea and millet flours, coupled with rising demand for gluten-free and fortified bakery and snack products.

- Manufacturers are investing in advanced milling, drying, and sprouting technologies to retain nutrient integrity and ensure consistent quality in specialty flour production.

- Private label and e-commerce channels are expanding specialty flour availability, offering blended flours and custom baking mixes to cater to diverse dietary preferences.

- Challenges include higher costs compared to wheat flour, functional differences in baking performance, and the need for formulation adaptation to achieve desired textures and taste.

Reort Scope

| Parameter | Detail |

|---|---|

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Nature, By Distribution Channel, By Application |

| Countries Covered | North America (USA, Canada, Mexico) Europe (Germany, UK, France, Spain, Italy, Rest of Europe) Asia-Pacific (China, India, Japan, Australia, Rest of APAC) The Middle East and Africa (Middle East, Africa) South and Central America (Brazil, Argentina, Rest of SCA) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10 % free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Datafile |

Market Segmentation

By Nature

- Organic

- Conventional

By Distribution channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retail

- Other Distribution Channel

By Application

- Bakery Products

- Noodles and Pasta

- Animal Feed and Pet Food

- Meat Products

- Snacks and Savory Products

- Tortillas

- Soups and Sauces

- Others

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- Syngenta Crop Protection AG (ChemChina)

- Bayer Crop Science LLC

- BASF SE

- Dow AgroSciences LLC

- Sumitomo Chemicals Co. Ltd.

- Corteva Agriscience Division of DowDuPont

- Monsanto Company (Bayer)

- FMC Corporation

- UPL Limited

- Nufarm Limited

- ADAMA Agricultural Solutions Ltd.

- Arysta Lifescience Inc.

- Isagro SPA

- Limin Group Co. Ltd.

- Hailir Pesticides and Chemicals Group Co. Ltd.

- Shandong Luba Chemical Co. Ltd.

- Jiangsu Changqing Agrochemical Co. Ltd.

- Guangdong Zhongxun Agricultural Science Co. Ltd.

- Zhejiang Heben Pesticide & Chemicals Co. Ltd.

- Nippon Soda Co. Ltd.

- Nissan Chemical Corporation

- Mitsui Chemicals Agro Inc.

- Cheminova A/S

- DuPont de Nemours Inc.

- Makhteshim Agan Industries Ltd.

- Sinochem International Corporation

- Jiangsu Huifeng Agrochemical Co. Ltd.

- Jiangsu Yangnong Chemical Group Co. Ltd.

- Rotam CropSciences Ltd.

- Gowan Company LLC

- Albaugh LLC

What You Receive

• Global Specialty Flours market size and growth projections (CAGR), 2024- 2034• Impact of recent changes in geopolitical, economic, and trade policies on the demand and supply chain of Specialty Flours.

• Specialty Flours market size, share, and outlook across 5 regions and 27 countries, 2025- 2034.

• Specialty Flours market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2025- 2034.

• Short and long-term Specialty Flours market trends, drivers, restraints, and opportunities.

• Porter’s Five Forces analysis, Technological developments in the Specialty Flours market, Specialty Flours supply chain analysis.

• Specialty Flours trade analysis, Specialty Flours market price analysis, Specialty Flours Value Chain Analysis.

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products.

• Latest Specialty Flours market news and developments.

The Specialty Flours Market international scenario is well established in the report with separate chapters on North America Specialty Flours Market, Europe Specialty Flours Market, Asia-Pacific Specialty Flours Market, Middle East and Africa Specialty Flours Market, and South and Central America Specialty Flours Markets. These sections further fragment the regional Specialty Flours market by type, application, end-user, and country.

Who can benefit from this research

The research would help top management/strategy formulators/business/product development/sales managers and investors in this market in the following ways1. The report provides 2024 Specialty Flours market sales data at the global, regional, and key country levels with a detailed outlook to 2034, allowing companies to calculate their market share and analyze prospects, uncover new markets, and plan market entry strategy.

2. The research includes the Specialty Flours market split into different types and applications. This segmentation helps managers plan their products and budgets based on the future growth rates of each segment

3. The Specialty Flours market study helps stakeholders understand the breadth and stance of the market giving them information on key drivers, restraints, challenges, and growth opportunities of the market and mitigating risks

4. This report would help top management understand competition better with a detailed SWOT analysis and key strategies of their competitors, and plan their position in the business

5. The study assists investors in analyzing Specialty Flours business prospects by region, key countries, and top companies' information to channel their investments.

Available Customizations

The standard syndicate report is designed to serve the common interests of Specialty Flours Market players across the value chain and include selective data and analysis from entire research findings as per the scope and price of the publication.However, to precisely match the specific research requirements of individual clients, we offer several customization options to include the data and analysis of interest in the final deliverable.

Some of the customization requests are as mentioned below :

Segmentation of choice – Our clients can seek customization to modify/add a market division for types/applications/end-uses/processes of their choice.

Specialty Flours Pricing and Margins Across the Supply Chain, Specialty Flours Price Analysis / International Trade Data / Import-Export Analysis

Supply Chain Analysis, Supply–Demand Gap Analysis, PESTLE Analysis, Macro-Economic Analysis, and other Specialty Flours market analytics

Processing and manufacturing requirements, Patent Analysis, Technology Trends, and Product Innovations

Further, the client can seek customization to break down geographies as per their requirements for specific countries/country groups such as South East Asia, Central Asia, Emerging and Developing Asia, Western Europe, Eastern Europe, Benelux, Emerging and Developing Europe, Nordic countries, North Africa, Sub-Saharan Africa, Caribbean, The Middle East and North Africa (MENA), Gulf Cooperation Council (GCC) or any other.

Capital Requirements, Income Projections, Profit Forecasts, and other parameters to prepare a detailed project report to present to Banks/Investment Agencies.

Customization of up to 10% of the content can be done without any additional charges.

Note: Latest developments will be updated in the report and delivered within 2 to 3 working days.

FAQ's

The Global Specialty Flours Market is estimated to generate USD 11.4 billion in revenue in 2025.

The Global Specialty Flours Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% during the forecast period from 2025 to 2034.

The Specialty Flours Market is estimated to reach USD 30.4 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!