"Specialty Foods Market is valued at $ 299.29 billion in 2026. Further, the market is expected to grow at a CAGR of 15.2% to reach $ 928.35 billion by 2034."

The Specialty Foods Market is flourishing as consumers increasingly seek premium, authentic, and artisanal products that stand out in taste, quality, and origin. Ranging from gourmet cheeses, charcuterie, and small-batch condiments to globally sourced spices, rare olive oils, and handcrafted snacks, specialty foods cater to discerning palates and experiential dining trends. E-commerce, cold-chain logistics, and curated retail displays have expanded market access, allowing small producers and food artisans to reach national or even international audiences. Shoppers gravitate toward specialty items for their superior ingredients, cultural storytelling, and perceived wellness benefits, driving ongoing innovation and diversification across product categories.

Manufacturers, retailers, and foodservice operators are embracing trend-led approaches—such as plant-forward formulations, heritage grain baking, and fermentation-based snacks—to capitalize on shifts toward health, sustainability, and global flavors. Younger consumers, fueled by travel and social media exposure, are particularly drawn to exotic or niche offerings. Sustainability credentials—like regenerative farming practices, minimal processing, and eco-friendly packaging—are becoming decision drivers. At the same time, consumers expect traceability through storytelling, origin labels, farm transparency, or carbon footprint claims. As shoppers balance indulgence and mindfulness, the specialty foods market is expected to continue its strong upward trajectory, powered by innovation, storytelling, and elevated consumption experiences.

North America is the leading region in the specialty foods market, propelled by rising health-conscious consumer behavior, the growing demand for organic and clean-label products, and the rapid expansion of premium retail and gourmet food chains. Organic and natural foods are the dominating segment in the specialty foods market, fueled by increasing consumer preference for minimally processed ingredients, heightened awareness of food sensitivities, and the proliferation of sustainable and plant-based food innovations.

Key Insights

- Health and wellness positioning remains one of the strongest demand drivers for specialty foods, as consumers increasingly seek products with cleaner labels, natural ingredients, functional benefits, and better nutritional profiles. This is supporting demand for organic, gluten-free, plant-based, high-protein, low-sugar, and minimally processed offerings. Specialty food brands that combine taste with wellness credibility are gaining stronger relevance across retail and online channels.

- Premiumization continues to shape the market as consumers show willingness to pay for distinctive flavor, superior ingredients, artisanal quality, and elevated food experiences. Gourmet sauces, specialty cheeses, premium snacks, craft bakery products, and high-end confectionery are benefiting from this trend. The market is increasingly defined by products that deliver authenticity, sensory appeal, and perceived value beyond standard food categories.

- Ethnic and global flavors are expanding rapidly as consumers become more adventurous and seek regionally inspired foods from different cuisines. Specialty products featuring Asian, Mediterranean, Latin American, Middle Eastern, and fusion flavors are gaining shelf space and foodservice attention. This trend supports innovation in sauces, seasonings, ready meals, snacks, frozen foods, and meal kits designed around culinary exploration.

- Convenience remains a major factor, with consumers demanding specialty foods that fit busy lifestyles without sacrificing quality or flavor. Ready-to-eat meals, premium frozen foods, gourmet snacks, prepared dips, sauces, and functional beverages are benefiting from this shift. Brands that deliver convenience with authenticity and high-quality positioning are well placed to capture repeat demand.

- Plant-based and alternative food formats are strengthening market opportunities as consumers pursue flexitarian eating, environmental awareness, and dietary variety. Specialty foods are increasingly incorporating plant-based proteins, dairy alternatives, meat substitutes, and vegetable-forward formulations. This category continues to evolve from basic substitution toward premium taste, texture, and culinary creativity.

- Digital commerce and direct-to-consumer models are reshaping how specialty foods reach consumers, enabling niche brands to build loyal communities beyond traditional retail shelves. Online platforms allow brands to tell richer stories around sourcing, ingredients, and production methods. This is particularly important for artisanal, regional, premium, and functional products seeking targeted consumer engagement.

- Sustainability and traceability are becoming stronger purchasing influences, with consumers paying closer attention to ethical sourcing, recyclable packaging, local production, and responsible supply chains. Specialty food brands often use sustainability as a core part of brand differentiation. Companies that can demonstrate authenticity, transparency, and responsible practices are likely to strengthen market positioning.

- Future growth in the specialty foods market will be driven by flavor innovation, health-oriented reformulation, premium snacking, online discovery, and demand for authentic culinary experiences. Opportunities will expand for brands that balance indulgence, nutrition, convenience, and sustainability. Long-term competitiveness will depend on product uniqueness, supply chain reliability, strong branding, and the ability to adapt quickly to changing consumer preferences.

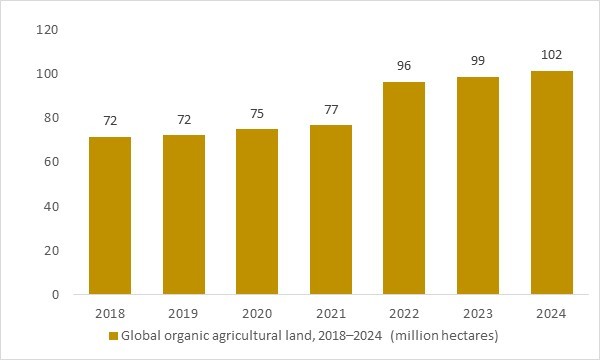

Global organic agricultural land, 2018–2024 (million hectares)

Figure: Global organic agricultural land increased from around 71.5 million hectares in 2018 to nearly 99 million hectares in 2023, with 2024e showing continued growth. This expanding base of certified organic farmland strengthens the supply of premium raw materials supporting the global specialty foods market.

- Global organic agricultural land expanded from about 71.5 million hectares in 2018 to nearly 99 million hectares in 2023, with 2024 showing a continued upward trend. The rapid growth in organically managed farmland illustrates the strengthening raw-material base (grains, fruits, vegetables, dairy and livestock) that underpins the global specialty foods market.

Regional Analysis

North America Specialty Foods Market

North America remains a leading specialty foods market, supported by strong consumer demand for premium, organic, clean-label, plant-based, ethnic, and functional food products. Market dynamics are shaped by high retail penetration, online grocery growth, strong specialty store networks, and rising interest in healthier indulgence. Lucrative opportunities are visible in premium snacks, gourmet sauces, specialty beverages, gluten-free foods, and globally inspired ready meals. The forecast remains favorable as consumers continue seeking differentiated products, while latest developments focus on direct-to-consumer expansion, sustainable packaging, and innovation in wellness-led food categories.

Asia Pacific Specialty Foods Market

Asia Pacific is a fast-growing specialty foods market, driven by urbanization, rising disposable income, expanding modern retail, and increasing consumer interest in premium and international food experiences. Market dynamics are influenced by evolving dietary preferences, demand for convenient packaged foods, and growing adoption of health-oriented and functional products. Lucrative opportunities are strong in premium bakery, ethnic snacks, functional beverages, plant-based foods, and regionally inspired gourmet products. The forecast remains robust as foodservice and online channels expand, while latest developments focus on localized flavor innovation, premiumization, and wider availability of specialty foods through modern trade and e-commerce.

Europe Specialty Foods Market

Europe represents a mature and quality-driven specialty foods market, supported by strong culinary traditions, demand for organic products, artisanal foods, regional specialties, and sustainable food practices. Market dynamics are shaped by consumer preference for authenticity, traceable sourcing, clean-label formulations, and premium food experiences. Lucrative opportunities are concentrated in specialty cheese, bakery, confectionery, sauces, plant-based foods, and gourmet ready meals. The forecast remains constructive as consumers continue balancing indulgence with health and sustainability, while latest developments center on ethical sourcing, recyclable packaging, product reformulation, and expansion of premium private-label specialty ranges.

Middle East & Africa Specialty Foods Market

The Middle East & Africa specialty foods market is developing steadily, supported by expanding modern retail, tourism, hospitality growth, urban lifestyle changes, and rising demand for premium and international food products. Market dynamics are influenced by growing interest in gourmet packaged foods, health-oriented products, halal-certified specialty items, and globally inspired flavors. Lucrative opportunities are emerging in premium snacks, specialty beverages, bakery products, dates-based products, ethnic sauces, and imported gourmet foods. The forecast remains positive as consumer exposure to international cuisines increases, while latest developments focus on retail expansion, premium foodservice offerings, and broader distribution of specialty and wellness-focused products.

South & Central America Specialty Foods Market

South & Central America presents promising growth opportunities in the specialty foods market, supported by rich regional food traditions, rising middle-class consumption, expanding retail channels, and growing demand for premium packaged foods. Market dynamics are shaped by interest in natural ingredients, artisanal products, functional foods, ethnic flavors, and convenient meal solutions. Lucrative opportunities are visible in specialty snacks, sauces, bakery products, confectionery, premium beverages, and organic or clean-label foods. The forecast remains encouraging as local brands and international players expand product availability, while latest developments focus on flavor innovation, modern retail growth, and stronger positioning of regional specialties in premium food categories.

Market Scope

| Parameter | Specialty Foods Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By Consumer Generation, By Distribution Channel |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Product Type

- Cheese and Plant-based cheese

- Frozen or refrigerated meat

- poultry

- and seafood

- Chips

- Pretzels

- and Snacks

- Bread and Baked goods

- Chocolate and Other Confectionery

- Other Product Types

By Consumer Generation

- Gen-Z

- Millennials

- Gen-X

- Baby Boomers

By Distribution Channel

- Food Service

- Retail

- Online

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- Cargill Incorporated

- Archer Daniels Midland Company

- United Natural Foods Inc.

- Compass Group plc

- DuPont de Nemours Inc.

- International Flavors & Fragrances Inc.

- Hormel Foods Corporation

- Koninklijke DSM NV

- Kerry Group plc

- Ingredion Incorporated

- Novozymes A/S

- Tate & Lyle plc

- AMCON Distributing Company

- Lancaster Colony Corporation

- Krispy Kreme Inc.

- Sensient Technologies

- Calavo Growers Inc.

- The a2 Milk Company Limited

- Chobani LLC

- Amy's Kitchen Inc.

- Farmer Bros. Co.

- Beyond Meat Inc.

- Daily Harvest Inc.

- Bear Creek Corporation

- American Spoon Foods Inc.

- Pacmoore Products Inc.

- AeroFarms LLC

- Eden Creamery LLC

- World Central Kitchen Inc.

- Axiom Foods Inc.

- Safe Catch Inc.

- Union Wine Company LLC

Recent Developments

- March 2026 – Woolworths announced the acquisition of in2food Holdings, strengthening its control over premium convenience foods, ready meals, and fresh prepared food supply. The move supports quality consistency, innovation speed, and supply chain resilience in specialty and premium food retail.

- March 2026 – McCormick announced an agreement to combine with Unilever’s foods business, creating a larger global flavor-focused company. The development strengthens its position across sauces, seasonings, condiments, and specialty food categories.

- November 2025 – Prosperity Organic Foods announced the acquisition of Miyoko’s Creamery, expanding its presence in plant-based dairy and organic specialty foods. The deal supports category consolidation in premium vegan cheese, butter, and dairy alternative products.

- July 2025 – Kraft Heinz announced an agreement to sell its Italian baby and specialty food business to NewPrinces Group. The transaction includes specialty food brands and supports portfolio reshaping toward focused food categories.

- June 2025 – Paine Schwartz Partners completed a strategic investment in Chex Finer Foods, a value-added specialty food distributor serving grocery channels. The investment supports expansion in premium, differentiated, and specialty food distribution.

- May 2025 – Danone acquired a majority stake in Kate Farms, a U.S.-based plant-based organic nutrition company. The acquisition strengthens Danone’s specialized nutrition portfolio and expands its position in organic, plant-based functional foods.

- May 2025 – Valeo Foods Group acquired Freddi Dolciaria, strengthening its position in the Italian sweet bakery sector. The deal expands Valeo’s specialty bakery, snacks, and treats portfolio across European markets.

- April 2025 – ITC moved forward with the acquisition of 24 Mantra Organic, strengthening its presence in organic packaged foods. The development supports ITC’s strategy to expand into healthier, premium, and sustainability-oriented specialty food categories.

- January 2025 – Patriot Pickle acquired Cosmo’s Food Products, expanding its specialty food portfolio into marinated vegetables, olives, peppers, garlic, mushrooms, and artichokes. The acquisition improves manufacturing capability and strengthens retail and foodservice reach.

- January 2025 – Deliciously Ella founders acquired the Allplants brand to rebuild and expand a plant-based prepared food platform. The development reflects continued repositioning in specialty plant-based meals, convenience foods, and better-for-you food categories.

FAQ's

The Specialty Foods Market is estimated to reach $ 928.35 billion by 2034.

The Specialty Foods Market is estimated to generate $ 299.29 billion in revenue in 2026.

The Specialty Foods Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 15.2% during the forecast period from 2026 to 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!