"The Spicate Clerodendranthus Extract Market was valued at $ 194.33 million in 2026 and is projected to reach $ 353.87 million by 2034, growing at a CAGR of 7.78%."

The Spicate Clerodendranthus Extract Market is a niche but emerging segment within botanical extracts, herbal supplements, functional ingredients, traditional medicine, nutraceuticals, and natural health products. Spicate clerodendranthus, also associated with kidney tea and cat’s whiskers in herbal ingredient trade, is valued for its traditional use in urinary health, kidney support, detoxification, anti-inflammatory positioning, and wellness formulations. Extracts are typically derived from leaves or aerial parts and processed into powders, liquid extracts, capsules, tablets, herbal teas, functional beverages, and topical or cosmetic ingredients. Demand is supported by rising consumer interest in plant-based remedies, clean-label supplements, preventive healthcare, traditional herbal medicine, and natural ingredients targeting urinary tract wellness, metabolic balance, and general detox support. The market also benefits from growing interest in Asian herbal ingredients, botanical standardization, and functional formulations that combine multiple herbs for kidney, bladder, liver, and inflammation-related wellness positioning.

The competitive landscape of the Spicate Clerodendranthus Extract Market includes botanical extract manufacturers, herbal supplement brands, nutraceutical companies, traditional medicine producers, contract manufacturers, ingredient distributors, and wellness product companies. Companies compete through raw material quality, extract standardization, active compound consistency, traceability, organic or clean-label positioning, regulatory documentation, formulation support, and ability to supply powders or liquid extracts for different applications. Latest trends include standardized polyphenol extracts, herbal tea blends, kidney-support supplements, natural diuretic positioning, plant-based detox products, combination formulas with cranberry or dandelion, and growing use in functional wellness products. Growth is driven by consumer preference for natural health solutions, rising awareness of urinary wellness, expansion of e-commerce supplement channels, and demand for botanical ingredients with traditional use history. However, challenges include limited mainstream awareness, quality variation, regulatory restrictions on health claims, supply-chain inconsistency, taste limitations, and need for stronger clinical substantiation. The outlook remains positive as botanical wellness brands continue exploring differentiated herbal extracts for preventive health and specialty supplement formulations.

Key Insights

- Spicate clerodendranthus extract is gaining attention because of its traditional positioning in kidney, urinary tract, and detox wellness applications. Consumers are increasingly interested in herbal products that support routine health maintenance rather than only treatment-based interventions. This creates opportunities for supplement brands to position the extract within preventive wellness, hydration support, and kidney-care formulations.

- The nutraceutical segment is one of the most important demand areas, as the extract can be formulated into capsules, tablets, powders, liquid drops, and herbal blends. Supplement companies are using botanical extracts to create targeted wellness products for urinary comfort, fluid balance, inflammation support, and metabolic health. Standardized extracts with clear documentation are more attractive for premium formulations.

- Herbal tea and functional beverage applications are creating additional market opportunities because spicate clerodendranthus has a long association with traditional tea consumption. Consumers seeking natural detox beverages, kidney-support teas, and plant-based wellness drinks are helping expand demand beyond capsule-based supplements. Taste refinement and blending with complementary herbs can improve product acceptance.

- Standardization is becoming a key competitive factor because botanical extracts can vary depending on plant origin, harvest timing, processing method, and extraction solvent. Buyers increasingly prefer suppliers that provide consistent active profiles, quality testing, heavy metal screening, microbial control, and batch-level documentation. This is especially important for nutraceutical and export-oriented ingredient markets.

- Asia Pacific remains an important supply and consumption base due to traditional herbal medicine practices, botanical raw material availability, and strong consumer familiarity with kidney tea-type herbal ingredients. Regional producers have opportunities to move from raw herb supply toward higher-value standardized extracts, branded ingredients, and private-label wellness products for domestic and export markets.

- Clean-label and plant-based wellness trends are supporting demand as consumers move toward natural ingredients with recognizable botanical origins. Spicate clerodendranthus extract can benefit from this shift when positioned around traditional use, sustainability, gentle wellness support, and compatibility with vegetarian or vegan supplement formats. Transparent sourcing and minimal processing claims can strengthen brand appeal.

- Combination formulations are becoming more common as brands pair spicate clerodendranthus extract with cranberry, dandelion, corn silk, horsetail, green tea, turmeric, or other botanical ingredients. These multi-ingredient blends allow companies to target broader wellness themes such as urinary support, detoxification, antioxidant support, and fluid balance. Formulation strategy is important for differentiation.

- Regulatory compliance remains a major market challenge because companies must avoid unsupported disease-treatment claims and align labeling with local supplement, food, or herbal product rules. Marketing language must be carefully managed, particularly in export markets with strict health-claim regulations. Suppliers that provide technical dossiers and compliance-ready documentation can support smoother commercialization.

- Raw material quality and supply reliability influence market development because herb identity, purity, and contamination control are essential for botanical extract credibility. Sustainable sourcing, proper drying, controlled storage, and authenticated plant material help reduce quality risks. Companies with traceable sourcing networks and robust testing systems are better positioned to serve premium buyers.

- Competition is shifting toward differentiated botanical ingredients with traditional credibility, functional positioning, and reliable quality control. Spicate clerodendranthus extract remains a niche ingredient, but it can gain stronger market traction through standardized extracts, branded supplement concepts, clinical research support, and stronger awareness among formulators. Suppliers that combine authenticity, documentation, and application support are expected to benefit.

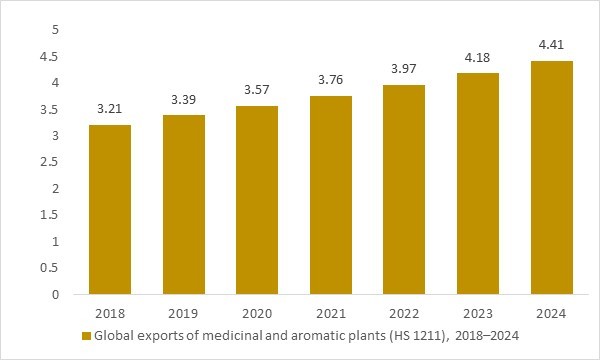

Global exports of medicinal and aromatic plants (HS 1211), 2018–2024

Figure: Global exports of medicinal and aromatic plants (HS 1211) increased from an estimated US$3.2 billion in 2018 to about US$4.2 billion in 2023, with further growth expected in 2024. This expanding trade in dried medicinal herbs and botanicals provides the broader raw material base that includes spicate clerodendranthus (Orthosiphon aristatus) for kidney and metabolic health products. OG Analysis estimates, aligned with UN COMTRADE and ITC trade statistics, highlight how the rapid growth of the medicinal and aromatic plants category supports long-term demand for standardized spicate clerodendranthus extracts.

Global trade in medicinal and aromatic plants (HS 1211) – the broad raw material category that includes spicate clerodendranthus (Orthosiphon aristatus) – expanded from an estimated US$3.2 billion in 2018 to around US$4.2 billion in 2023, with the trajectory pointing towards US$4.4 billion in 2024. UN COMTRADE and ITC trade statistics show that exports of MAPs nearly doubled between 2010 and 2023 as pharmaceutical, nutraceutical, functional beverage and cosmetic manufacturers increasingly substitute synthetic actives with botanical ingredients. Within this growing HS 1211 stream, spicate clerodendranthus leaves and extracts benefit from rising demand for kidney, urinary and metabolic health formulations. The robust growth of the wider MAP export base therefore provides strong context for the expansion of the spicate clerodendranthus extract market, signalling a deeper and more diversified supply chain for high-grade raw herb and standardized extracts.

Regional Analysis

North America Spicate Clerodendranthus Extract Market

North America Spicate Clerodendranthus Extract Market is driven by rising demand for botanical supplements, herbal wellness products, urinary health formulations, detox blends, and natural functional ingredients. Market dynamics are shaped by consumer preference for clean-label supplements, plant-based preventive healthcare, e-commerce wellness brands, and growing interest in traditional herbal ingredients with kidney and bladder support positioning. Lucrative opportunities exist for botanical extract suppliers, nutraceutical companies, herbal tea brands, contract manufacturers, and wellness product formulators offering standardized, traceable, and low-odor extract formats. Latest trends include kidney-support capsules, herbal detox teas, combination botanical formulas, vegan supplement formats, and clean-label urinary wellness products. The forecast outlook remains favorable as consumers continue shifting toward natural wellness solutions and brands explore differentiated herbal extracts for targeted health applications.

Asia Pacific Spicate Clerodendranthus Extract Market

Asia Pacific Spicate Clerodendranthus Extract Market is supported by strong traditional herbal medicine practices, raw material availability, established botanical processing capacity, and consumer familiarity with kidney tea-type herbal ingredients. Market dynamics are driven by demand from herbal medicine producers, nutraceutical brands, functional beverage companies, tea manufacturers, and natural health product exporters. The region presents strong opportunities for extract manufacturers, herbal ingredient suppliers, private-label supplement producers, and wellness brands offering standardized powders, liquid extracts, and herbal blends. Latest trends include botanical tea formulations, urinary wellness supplements, standardized polyphenol extracts, clean-label plant-based products, and export-oriented ingredient development. The forecast remains positive as regional producers move toward higher-value extraction, quality documentation, and branded herbal ingredient solutions.

Europe Spicate Clerodendranthus Extract Market

Europe Spicate Clerodendranthus Extract Market is shaped by rising demand for natural health products, botanical supplements, herbal teas, and clean-label functional ingredients, alongside strict quality and regulatory expectations. Market dynamics are influenced by consumer interest in preventive wellness, plant-based formulations, organic positioning, traceable sourcing, and cautious health-claim compliance. Lucrative opportunities exist for botanical extract distributors, herbal supplement companies, tea brands, nutraceutical formulators, and contract manufacturers that can provide quality-tested and documentation-ready spicate clerodendranthus extract. Latest trends include herbal detox blends, kidney-support wellness products, standardized extracts, organic botanical formulations, and combination products using complementary herbs. The forecast outlook remains steady as European buyers continue prioritizing safety, ingredient authenticity, sustainability, and regulatory-compliant product positioning.

Middle East & Africa Spicate Clerodendranthus Extract Market

Middle East & Africa Spicate Clerodendranthus Extract Market is developing gradually through rising interest in herbal supplements, natural remedies, wellness beverages, traditional medicine, and preventive healthcare products. Market dynamics vary across the region, with Gulf countries showing stronger demand for premium imported supplements and herbal wellness products, while African markets present opportunities through local herbal medicine traditions, natural ingredient trade, and growing retail access to supplements. Companies can benefit by offering affordable, stable, and easy-to-formulate extract formats suitable for capsules, teas, powders, and liquid preparations. Latest trends include natural detox products, plant-based kidney-support blends, herbal tea consumption, and wellness positioning around traditional botanicals. The forecast remains constructive as consumer awareness, retail availability, and interest in natural health products continue improving.

South & Central America Spicate Clerodendranthus Extract Market

South & Central America Spicate Clerodendranthus Extract Market is supported by growing consumer interest in herbal remedies, natural supplements, functional teas, and plant-based wellness products. Market dynamics are shaped by expanding nutraceutical distribution, increasing awareness of urinary and kidney wellness, demand for affordable botanical ingredients, and rising use of traditional and complementary health products. Opportunities exist for herbal supplement brands, botanical extract distributors, tea producers, natural product retailers, and contract manufacturers offering standardized spicate clerodendranthus extract in convenient formats. Latest trends include detox teas, urinary wellness capsules, multi-herb formulations, clean-label supplements, and e-commerce-driven botanical product sales. The forecast outlook remains positive as consumers increasingly adopt natural preventive health solutions and regional brands diversify into specialty herbal extracts.

Report Scope

| Parameter | Spicate Clerodendranthus Extract Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Spicate Clerodendranthus Extract Market Segmentation

By Product

- Powder

- Liquid

By Application

- Cosmetics

- Dietary Supplements

- Food and Beverages

By End User

- Manufacturers

- Retailers

- Wholesalers

By Technology

- Cold Extraction

- Hot Extraction

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Companies Analysed

- Naturalin Bio-Resources Co., Ltd.

- Xi’an Sost Biotech Co., Ltd.

- Shaanxi Jiahe Phytochem Co., Ltd.

- Organic Herb Inc.

- Hunan Nutramax Inc.

- Botanic Healthcare

- Greenutra Resource Inc.

- Changsha Herbway Biotech Co., Ltd.

- Herb Nutritionals Co., Ltd.

- Xi’an Greena Biotech Co., Ltd.

- Guangzhou Phytochem Sciences Inc.

- Shaanxi Hongda Phytochemistry Co., Ltd.

- Sun Ten Pharmaceutical Co., Ltd.

- JIAHERB, Inc.

- Hawlik Gesundheitsprodukte GmbH

Recent Developments

- November 2025 - Orthosiphon was featured in updated consumer-facing botanical guidance covering benefits, dosage, and contraindications. The update supports wider consumer awareness of Java tea-type herbal ingredients in urinary wellness and natural health product positioning.

- March 2025 - A comprehensive scientific review on Clerodendranthus spicatus was published, covering chemical constituents, pharmacology, quality control, and clinical applications. The review strengthens technical understanding for suppliers developing standardized spicate clerodendranthus extract products.

- 2025 - New transcriptome research on Orthosiphon stamineus supported deeper understanding of plant-part differences and antioxidant-related properties. The development is relevant for extract manufacturers seeking better raw material selection, quality consistency, and bioactive compound optimization.

- 2025 - Research interest increased around nephroprotective phytopharmaceuticals, with Orthosiphon-related botanicals appearing within broader kidney-support and chronic kidney disease research discussions. This supports continued positioning of spicate clerodendranthus extract in urinary and renal wellness formulations.

- 2024 - Scientific research on kidney tea showed potential activity in diabetic nephropathy models through gut microbiota and ferroptosis-related mechanisms. The findings support continued interest in Orthosiphon-based ingredients for metabolic and kidney-health research pipelines.

- 2024 - Research on Clerodendranthus spicatus water extracts explored effects related to hyperuricemia and kidney-related health pathways. The study added scientific support for traditional positioning around uric acid balance, kidney protection, and anti-inflammatory applications.

- 2024 - A review of Clerodendranthus spicatus active constituents identified multiple compounds associated with anti-inflammatory, antioxidant, uric acid-lowering, and kidney-protective properties. This reinforced the need for standardized extraction and compound profiling in commercial ingredient development.

- 2024 - Kidney tea research continued to highlight Orthosiphon aristatus as a traditionally used botanical with relevance in urinary health and metabolic wellness. This supports product development opportunities in herbal teas, capsules, and combination wellness supplements.

FAQ's

The Spicate Clerodendranthus Extract Market is estimated to generate $194.33 million in revenue in 2026.

The Spicate Clerodendranthus Extract Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 7.78% during the forecast period from 2026 to 2034.

The Spicate Clerodendranthus Extract Market is estimated to reach $ 353.87 million by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!