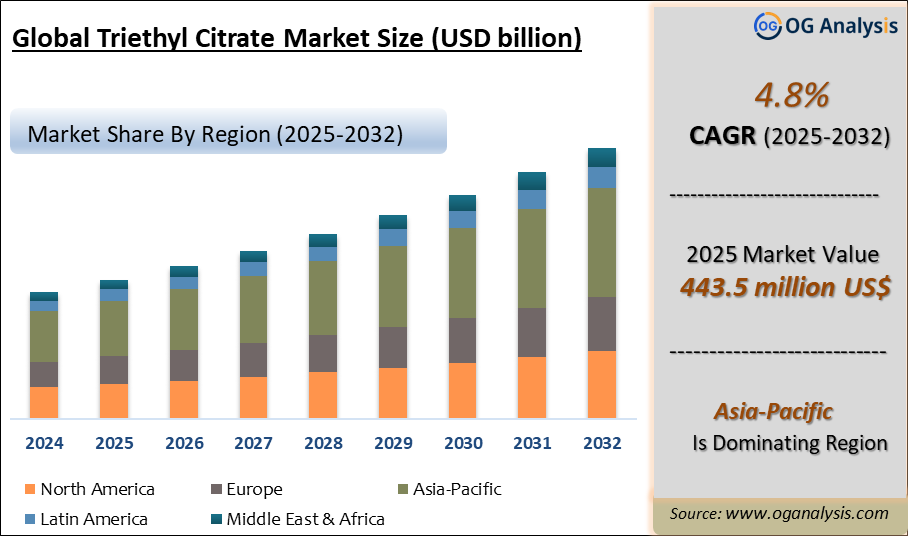

The Triethyl Citrate Market is estimated at USD 406.7 million in 2023. Further, the market is expected to grow from USD 423.2 million in 2024 to USD 589.9 million in 2031 at a CAGR of 4.8%.

Triethyl Citrate Market Overview

Triethyl Citrate also known as Ethyl Citrate, a chemical compound represented by the formula C12H20O7, plays an important role as a flavour enhancer, plasticizer, solubilizer, and emollient in different applications. Triethyl Citrate is a colourless oily liquid with a fruity odor. It is a highly pure and versatile ingredient, well known for its exceptional properties. It is prepared by the esterification of citric acid and ethanol in the presence of a catalyst. It's a versatile lightweight emollient that is non-blocking, non-greasy, has low viscosity, quickly absorbs, and leaves minimal stickiness on the skin.

The applications of triethyl citrate are found in different industries including the food industry, pharmaceutical industry, cosmetics industry, personal care industry, and plastic and polymer industry. Triethyl citrate meets the highest standards of quality and is compliant with FG (USP-NF) and Food Chemicals Codex regulations, ensuring its suitability in different applications. Triethyl Citrate is used as a flavouring agent in foods, as a plasticizer in the pharmaceutical industry for coating, as a food additive for stabilizing foams, and as a pseudo-emulsifier in e-cigarette juices.

Trade Intelligence for Triethyl Citrate Market

|

Global Salts and esters of citric acid (excl. inorganic or organic compounds of mercury) Trade, Imports, USD million, 2020-24 |

|||||

|

|

2020 |

2021 |

2022 |

2023 |

2024 |

|

World |

660 |

840 |

1,356 |

1,090 |

952 |

|

United States of America |

74.4 |

107 |

186 |

165 |

141 |

|

France |

27.1 |

33.9 |

48.3 |

50.6 |

56.3 |

|

Germany |

42.4 |

62.0 |

101 |

56.7 |

50.5 |

|

Poland |

31.4 |

56.0 |

66.4 |

80.3 |

49.8 |

|

Netherlands |

50.1 |

56.2 |

99.3 |

88.2 |

48.9 |

|

Source: OGAnalysis, International Trade Centre (ITC) |

|||||

- United States of America, France, Germany, Poland and Netherlands are the top five countries importing 36.4% of global Salts and esters of citric acid (excl. inorganic or organic compounds of mercury) in 2024

- Global Salts and esters of citric acid (excl. inorganic or organic compounds of mercury) Imports increased by 44.2% between 2020 and 2024

- United States of America accounts for 14.8% of global Salts and esters of citric acid (excl. inorganic or organic compounds of mercury) trade in 2024

- France accounts for 5.9% of global Salts and esters of citric acid (excl. inorganic or organic compounds of mercury) trade in 2024

- Germany accounts for 5.3% of global Salts and esters of citric acid (excl. inorganic or organic compounds of mercury) trade in 2024

|

Global Salts and esters of citric acid (excl. inorganic or organic compounds of mercury) Export Prices, USD/Ton, 2020-24 |

|

|

|

Source: OGAnalysis |

Latest Trends in Triethyl Citrate Market

Emerging Applications of Triethyl Citrate in the Cosmetics & Personal Care Industry:

Triethyl Citrate is used in the formulation for making skincare products such as hand creams, foot balsams, facial creams, sun care creams, hand creams, exfoliation creams, facial moisturizers, anti-aging creams and body lotions. Due to increasing middle-class disposable income and rising aspirations for a fulfilling life and attractive appearance, there is a greater demand for cosmetic products. Triethyl citrate is a common ingredient in numerous cosmetic and beauty products. Triethyl citrate is used by perfumers as a fixative, diluent, and solvent.

Triethyl citrate is an effective solvent for lacquers, varnish, and deodorants because it mixes easily with water and a variety of organic substances. In personal care, Triethyl Citrate is used in infant care products, bath products, creams and lotions, cosmetic sprays and many other types of personal care products. It is also an active ingredient in many chemical skin peels. Triethyl citrate effectively mitigates the accumulation of undesirable body odor by impeding the activity of sweat-producing bacteria enzymes. Its skin tolerance, along with deodorizing attributes, make triethyl citrate highly suitable for deodorant formulations.

Driving Factors

Superior Properties of Triethyl Citrate:

The triethyl citrate market is estimated to experience growth during the forecast period, driven by its excellent properties. Triethyl citrate is generally considered a safe and non-toxic compound, as it improves the flexibility and softness of materials. Triethyl citrate is compatible with a variety of polymers which enhances its utility in different industrial applications. Triethyl citrate is biodegradable and has a low boiling point ensuring easy vaporization. It is a colourless, odourless liquid exhibiting notable solvency and minimal toxicity.

Triethyl citrate possesses excellent flavour and fragrance enhancement properties, natural origin, and exceptional purity. Triethyl citrate is commonly included for its ability to control oil, promoting the well-being of skin and hair. Moreover, it enhances the viscosity of specific formulations, yielding a luxurious texture that is more user-friendly. Also, triethyl citrate serves as an effective solvent and perfuming agent, effectively masking the odors of other ingredients within a formulation. Triethyl citrate is a vital choice for companies focusing on green, natural, and organic mixture

Market Challenges

Strict Environmental Regulations Regarding Triethyl Citrate:

Triethyl citrate is regulated differently across the globe, like in the U.S., it is regulated as a dietary supplement by the Food and Drug Administration (FDA). In the European Union, triethyl citrate is regulated as a food additive by the European Food Safety Authority (EFSA). In Canada, it is regulated as a food additive by Health Canada. In Australia, it is regulated as a food additive by Food Standards Australia New Zealand (FSANZ).

In India, it is regulated as a food additive by the Food Safety and Standards Authority of India (FSSAI). An accidental release of triethyl citrate to the environment may pose a danger to fish, invertebrates and other aquatic organisms before degradation. Triethyl citrate is not expected to adsorb to suspended solids and sediment or accumulate in the tissues of aquatic organisms. The compound gets absorbed in the body by ingestion and inhalation causing irritation in the eyes, lung irritation with coughing and nausea, central nervous depression, and slowing of reflexes. This becomes the biggest limitation to the market growth.

Companies Mentioned

- BASF SE

- Fuso Chemical Co., Ltd.

- Merck KGaA

- Jiangsu Lemon Chemical & Technology Co., Ltd

- Debye Scientific Co., Ltd

- A&J Pharmtech Co., LTD

- RennoTech Co., Ltd

- Finetech Industry Limited

- Sigma-Aldrich

- Tokyo Chemical Industry Co., Ltd.

- MORIMURA BROS. Inc.

- Viachem Ltd.

- Vertellus

Report Scope

|

Parameter |

Triethyl Citrate Market scope Detail |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Market Size-Units |

USD million |

|

Market Splits Covered |

By Grade, By End-User, By Sales Channel |

|

Countries Covered |

North America (USA, Canada, Mexico) |

|

Analysis Covered |

Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

|

Customization |

10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

|

Post-Sale Support |

4 analyst hours, available up to 4 weeks |

|

Delivery Format |

The Latest Updated PDF and Excel Data file |

Market Segmentation

By Grade

- Industrial Grade

- Food Grade

- Pharmaceutical Grade

By End-Use Industry

- Specialty Chemicals

- Food & Beverages

- Pharmaceutical

- Cosmetics & Personal care

- Other

By Sales Channel

- Direct B2B

- Offline Retail

- Online

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, South Korea, Indonesia, Malaysia, Vietnam, Rest of APAC)

- The Middle East and Africa (Saudi Arabia, South Africa, UAE, Iran, Egypt, Rest of MEA)

- South and Central America (Brazil, Argentina, Chile, Rest of SCA)

Recent Developments

- September 2025: Jungbunzlauer announced the acquisition of a multipurpose production site in Thomson, Illinois, from International Flavors & Fragrances Inc., marking its first U.S. manufacturing footprint to expand local production of citric acid derivatives including triethyl citrate.

- August 2025: Jungbunzlauer received the EcoVadis Platinum Medal for sustainability excellence, ranking among the top 1% of companies globally for ethical, social, and environmental performance in chemical manufacturing.

- July 2025: BASF revised its 2025 financial outlook downward due to weaker global demand for specialty and base chemicals, affecting product categories such as plasticizers and citrates used in coatings and personal care formulations.

- July 2025: Jungbunzlauer introduced TayaGel LA, a new low-acyl gellan gum designed for clean-label formulations, strengthening its biobased ingredient portfolio alongside its citrate product range.

- April 2025: BASF reported lower quarterly sales and margins driven by ongoing chemical market headwinds, signaling continued cost and demand pressures across its performance materials and plasticizer value chains.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!