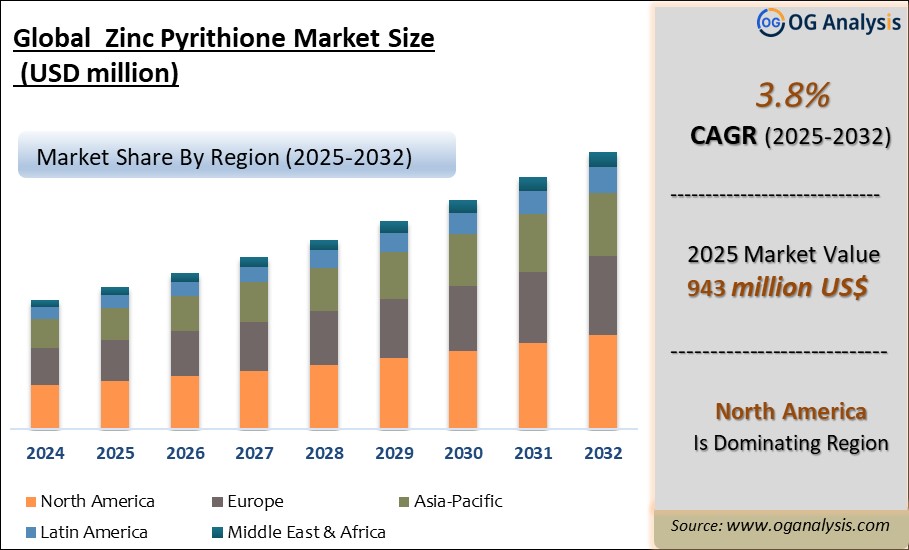

"The Global Zinc Pyrithione Market Size was valued at USD 913 million in 2024 and is projected to reach USD 943 million in 2025. Worldwide sales of Zinc Pyrithione are expected to grow at a significant CAGR of 3.8%, reaching USD 1,340 million by the end of the forecast period in 2034."

Introduction and Overview

The zinc pyrithione market has witnessed significant growth due to the increasing demand for effective antifungal and antimicrobial agents across various industries. Zinc pyrithione, a compound known for its potent antifungal properties, is widely utilized in personal care products, particularly in anti-dandruff shampoos and treatments for scalp conditions. Its efficacy in combating fungal infections and reducing dandruff has made it a staple ingredient in many cosmetic formulations. Additionally, the compound's use extends to industrial applications, such as in coatings and paints, where it helps prevent microbial growth and degradation. As consumer awareness regarding skin health and hygiene increases, the demand for products containing zinc pyrithione is expected to continue rising, driving market expansion.

The market's growth is further fueled by the rising prevalence of skin disorders and the expanding pharmaceutical sector. Zinc pyrithione's effectiveness in treating conditions like seborrheic dermatitis and psoriasis contributes to its increasing adoption in medical and over-the-counter treatments. Furthermore, innovations in product formulations and the development of new applications for zinc pyrithione are creating opportunities for market players. As companies invest in research and development to enhance the compound's efficacy and safety, the market is poised for continued growth. Overall, the zinc pyrithione market is positioned for robust expansion, driven by both consumer demand and advancements in product technology.

Trade Intelligence for zinc pyrithione market

| Global Heterocyclic compounds with nitrogen hetero-atom[s] only, containing an unfused pyridine ring, n.e.s. Trade, Imports, USD million, 2020-24 | |||||

|

| 2020 | 2021 | 2022 | 2023 | 2024 |

| World | 15,790 | 13,674 | 16,493 | 26,040 | 13,301 |

| Germany | 3,333 | 1,724 | 2,623 | 2,933 | 1,539 |

| United States of America | 1,609 | 1,658 | 1,881 | 1,669 | 1,350 |

| Brazil | 712 | 931 | 1,310 | 1,065 | 1,047 |

| Belgium | 3,095 | 2,026 | 715 | 2,378 | 791 |

| China | 683 | 671 | 821 | 683 | 562 |

| Source: OGAnalysis, International Trade Centre (ITC) | |||||

- Germany, United States of America, Brazil, Belgium and China are the top five countries importing 39.8% of global Heterocyclic compounds with nitrogen hetero-atom[s] only, containing an unfused pyridine ring, n.e.s. in 2024

- Global Heterocyclic compounds with nitrogen hetero-atom[s] only, containing an unfused pyridine ring, n.e.s. Imports decreased by 15.8% between 2020 and 2024

- Germany accounts for 11.6% of global Heterocyclic compounds with nitrogen hetero-atom[s] only, containing an unfused pyridine ring, n.e.s. trade in 2024

- United States of America accounts for 10.2% of global Heterocyclic compounds with nitrogen hetero-atom[s] only, containing an unfused pyridine ring, n.e.s. trade in 2024

- Brazil accounts for 7.9% of global Heterocyclic compounds with nitrogen hetero-atom[s] only, containing an unfused pyridine ring, n.e.s. trade in 2024

| Global Heterocyclic compounds with nitrogen hetero-atom[s] only, containing an unfused pyridine ring, n.e.s. Export Prices, USD/Ton, 2020-24 |

|

|

| Source: OGAnalysis |

Latest Trends in the Zinc Pyrithione Market

One of the latest trends in the zinc pyrithione market is the growing emphasis on natural and organic formulations. Consumers are increasingly seeking products with fewer synthetic ingredients and are favoring those with natural components. This shift has led manufacturers to explore and incorporate zinc pyrithione into organic and eco-friendly personal care products. Companies are developing formulations that combine zinc pyrithione with other natural ingredients to enhance their effectiveness while meeting consumer preferences for sustainability and reduced chemical exposure. This trend is expected to drive innovation and increase market opportunities for zinc pyrithione products that align with these consumer demands.

Another significant trend is the expansion of zinc pyrithione's application beyond traditional personal care products. Recent research has explored its potential in new areas, such as in the treatment of various skin conditions and even in environmental applications like anti-fungal coatings for surfaces. The versatility of zinc pyrithione in addressing different needs is opening up new market segments and opportunities for growth. As industries explore its broader applications, the market for zinc pyrithione is likely to experience increased interest and investment in innovative product development.

The rise of e-commerce and digital marketing is also shaping the zinc pyrithione market. Online platforms provide a convenient and accessible way for consumers to discover and purchase products containing zinc pyrithione. This trend is driving the growth of direct-to-consumer sales channels and allowing smaller brands to reach a global audience. Additionally, digital marketing strategies are being employed to educate consumers about the benefits of zinc pyrithione, further boosting its market presence. As online shopping continues to grow, it is expected to have a positive impact on the market, facilitating increased sales and brand visibility.

Drivers of the Zinc Pyrithione Market

The primary drivers of the zinc pyrithione market include the increasing prevalence of skin conditions such as dandruff, seborrheic dermatitis, and psoriasis. These conditions are prompting consumers to seek effective treatments, boosting the demand for products containing zinc pyrithione. The compound's well-documented antifungal and antimicrobial properties make it a preferred choice for managing these skin disorders. Additionally, the rising awareness of personal hygiene and skin health is leading to greater consumption of anti-dandruff and scalp treatment products, further driving market growth.

Another key driver is the continuous innovation and development of new formulations incorporating zinc pyrithione. Manufacturers are investing in research to enhance the effectiveness and safety of products containing the compound, which is contributing to market expansion. Advances in technology and formulation techniques are enabling the creation of more effective and versatile products, catering to a wider range of consumer needs. As new applications and product types emerge, the market is likely to experience sustained growth and increased investment.

The growing popularity of e-commerce and online retail channels is also fueling the zinc pyrithione market. The convenience and accessibility of online shopping have made it easier for consumers to find and purchase products containing zinc pyrithione. This trend is expanding the market reach and providing opportunities for brands to engage with a broader audience. As online sales continue to rise, they are expected to drive growth in the zinc pyrithione market by increasing product availability and consumer awareness.

Market Challenges

Despite its promising growth prospects, the zinc pyrithione market faces several challenges. One significant challenge is the potential for regulatory hurdles and compliance issues. As the compound is used in personal care and pharmaceutical products, it must meet stringent regulations and safety standards. Variations in regulatory requirements across different regions can create barriers for market entry and increase the cost of compliance for manufacturers. Additionally, concerns about the long-term safety of zinc pyrithione and its environmental impact may lead to more rigorous regulations, affecting market dynamics and potentially limiting growth.

Market Players

1. AkzoNobel N.V.

2. BASF SE

3. Clariant AG

4. Lonza Group

5. Vanderbilt Minerals, LLC

6. Kumar Organic Products Limited

7. Salicylates and Chemicals Pvt. Ltd.

8. Zhejiang Regen Chemical Co., Ltd.

9. Kolon Industries, Inc.

10. Hubei Xiangyun (Group) Chemical Co., Ltd.

Report Scope

| Parameter | zinc pyrithione market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD million |

| Market Splits Covered | By Application, By Grade, By Form, and By End-User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

- By Application

- Cosmetic and Personal Care

- Paint and Coatings

- Pharmaceuticals

- Biocides

- Others

- By Grade

- Industrial Grade

- Pharmaceutical Grade

- By Form

- Liquid Form

- Powder Form

- By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Recent Developments

- Lonza announced senior leadership changes with new appointments in operations and quality to strengthen its manufacturing and regulatory oversight across specialty chemicals including antimicrobial ingredients.

- Lonza reported strong revenue growth in its half-year performance and revised its annual guidance upward, reflecting steady demand across its life sciences and specialty ingredient portfolio.

- Kumar Organic Products updated its zinc pyrithione product line, highlighting continued engagement in antimicrobial and personal care applications with refreshed portfolio details.

FAQ's

The Global Zinc Pyrithione Market is estimated to generate USD 913 million in revenue in 2024.

The Global Zinc Pyrithione Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 3.8% during the forecast period from 2025 to 2032.

The Zinc Pyrithione Market is estimated to reach USD 1230.4 million by 2032.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!