Allulose Market Outlook 2026–2034: Sugar Reduction Trends, Growth Drivers, Leading Companies, and Future Opportunities

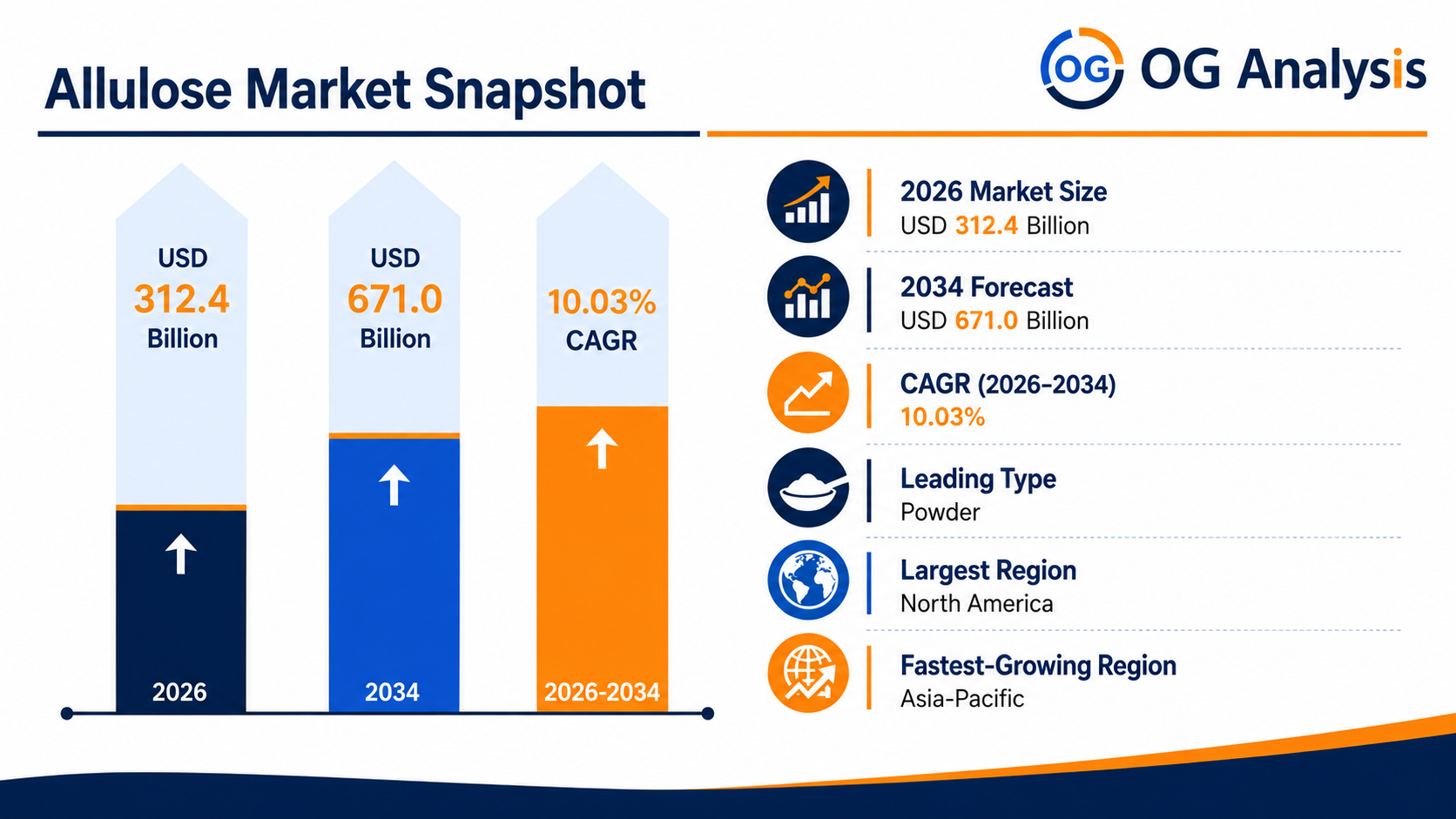

The Allulose Market is valued at $ 312.4 billion in 2026 and is expected to grow at a CAGR of 10.03% to reach $ 671.0 billion by 2034.

Allulose is a rare sugar and low-calorie sweetener used as a sugar-reduction ingredient in food and beverage products. It provides sugar-like taste, browning, bulk, and texture benefits while supporting low-sugar, reduced-calorie, diabetic-friendly, keto, and clean-label product positioning. The market includes allulose powder, liquid allulose, and blends used across bakery, confectionery, dairy, beverages, desserts, sauces, nutrition bars, tabletop sweeteners, and functional foods. Growth is supported by rising consumer demand for sugar reduction, obesity and diabetes management, low-carb diets, reformulation of packaged foods, and increasing use of alternative sweeteners by food manufacturers. Product development is increasingly focused on better taste profiles, cost-efficient fermentation or enzymatic production, improved solubility, and blends with stevia, monk fruit, erythritol, and other sweeteners.

Get Your Free Sample Report for In-Depth Market Insights :

https://www.oganalysis.com/industry-reports/allulose-market/free-sample

1. What is the latest trend in the Allulose Market?

The latest trend is the rising use of allulose in low-sugar, keto-friendly, diabetic-friendly, and reduced-calorie food and beverage formulations.

Manufacturers are using allulose to replace sugar while maintaining taste, browning, mouthfeel, and texture.

Allulose blends with stevia, monk fruit, and sugar alcohols are gaining popularity to improve sweetness balance.

Clean-label and better-for-you product launches are increasing demand across bakery, confectionery, dairy, and beverages.

2. What are the key challenges in the Allulose Market?

Key challenges include high production cost, limited raw material availability, regulatory differences, consumer awareness gaps, and formulation complexity.

Allulose is more expensive than many conventional sweeteners, which can limit adoption in price-sensitive mass-market products.

Food manufacturers must balance sweetness, texture, solubility, stability, and labeling requirements across applications.

Digestive tolerance, taste optimization, and supply-chain scalability are also important product-development concerns.

3. What is the major driving factor for the Allulose Market?

The major driving factor is increasing global demand for sugar reduction in packaged foods and beverages.

Consumers are looking for sweet-tasting products with fewer calories and lower sugar content.

Food brands are reformulating products to address obesity, diabetes, metabolic health, and clean-label wellness trends.

Allulose is attractive because it performs more like sugar than many high-intensity sweeteners in certain applications.

4. What is the major segment in the Allulose Market and why?

Powder allulose represents a major segment because it is easy to transport, store, dose, and blend into dry food formulations.

It is widely used in bakery mixes, confectionery, nutrition products, tabletop sweeteners, desserts, and powdered beverage applications.

Powder formats also support better handling for industrial-scale food manufacturing.

Liquid allulose is gaining demand in beverages, syrups, sauces, dairy products, and ready-to-use sweetener formulations.

5. Which application or end-user is driving more demand?

Food and beverage manufacturers are driving the highest demand for allulose as they reformulate products with reduced sugar and lower calories.

Bakery, confectionery, dairy, beverages, nutrition bars, frozen desserts, and sauces are key application areas.

Health-focused brands use allulose to support keto, low-carb, diabetic-friendly, and clean-label positioning.

Retail tabletop sweeteners and direct-to-consumer low-sugar products are also expanding market visibility.

6. Which region offers the highest growth potential and why?

North America remains a leading market due to strong sugar-reduction demand, high adoption of keto and low-carb diets, and favorable labeling momentum.

The United States has strong demand from packaged food, beverage, nutrition, and tabletop sweetener brands.

Asia Pacific offers strong growth potential due to expanding food processing, rising diabetes concerns, and growing interest in functional sweeteners.

Europe also presents opportunities, although regulatory approval pathways and labeling requirements influence adoption speed.

7. What strategies are major companies adopting in the market?

Major companies are focusing on production scale-up, cost reduction, sweetener blends, application-specific solutions, and food-brand partnerships.

They are investing in enzymatic conversion, fermentation technologies, and improved purification processes to make allulose more commercially viable.

Ingredient suppliers are developing blends that combine allulose with stevia, monk fruit, erythritol, and fiber-based ingredients.

Companies are also supporting customers with formulation, labeling, taste optimization, and regulatory guidance.

8. What are the leading companies in the Allulose Market?

Leading companies include Cargill, Ingredion, Tate & Lyle, CJ CheilJedang, Samyang Corporation, Matsutani Chemical Industry, Anderson Advanced Ingredients, Apura Ingredients, Bonumose, and Icon Foods.

These companies compete through production capacity, ingredient quality, pricing, formulation support, regulatory expertise, and customer relationships.

Large ingredient suppliers benefit from established food and beverage manufacturer networks.

Specialist sweetener companies compete through blends, clean-label positioning, and application-specific product development.

9. Why is allulose strategically important for food and beverage companies?

Allulose is strategically important because it helps companies reduce sugar while preserving many functional properties of sucrose.

It supports reformulation in products where taste, bulk, texture, browning, and mouthfeel are difficult to maintain with high-intensity sweeteners alone.

The ingredient creates opportunities across low-calorie, keto, diabetic-friendly, and better-for-you product lines.

For brands, allulose can strengthen innovation in sugar reduction without sacrificing consumer eating experience.

10. What is the future outlook for the Allulose Market?

The market outlook remains positive as sugar-reduction trends, metabolic health awareness, and low-calorie product innovation continue to expand.

Future growth will be supported by improved production economics, wider regulatory acceptance, better supply availability, and broader consumer education.

Allulose is expected to gain stronger use in bakery, confectionery, beverages, dairy, nutrition products, and tabletop sweeteners.

Companies offering cost-effective supply, strong technical support, clean-label solutions, and reliable regulatory guidance are expected to gain market share.

Browse Related Reports

https://www.oganalysis.com/industry-reports/food-enzymes-market

https://www.oganalysis.com/industry-reports/coconut-sugar-market

https://www.oganalysis.com/industry-reports/invert-sugar-market

https://www.oganalysis.com/industry-reports/starch-derivatives-market

https://www.oganalysis.com/industry-reports/bakery-market

Stay Connected With Us

LinkedIn | Twitter