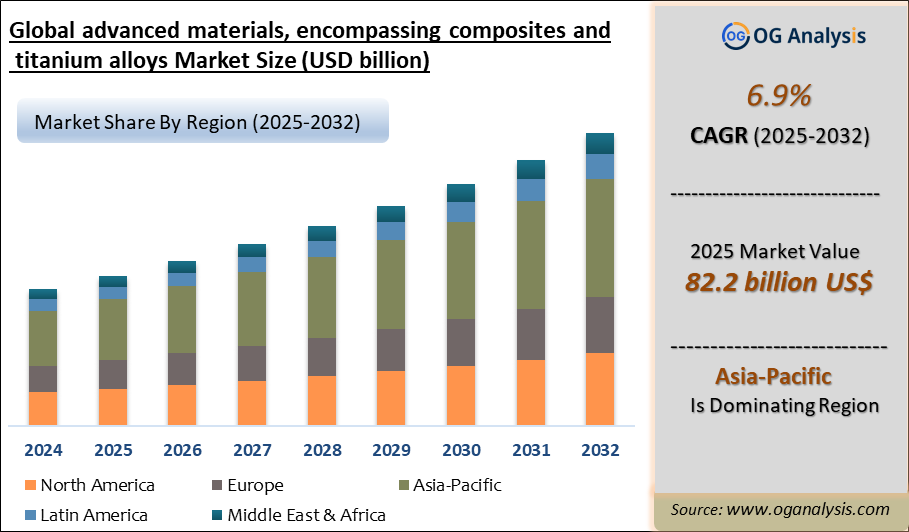

"The Global Advanced Materials Market Size was valued at USD 77.6 billion in 2024 and is projected to reach USD 82.2 billion in 2025. Worldwide sales of Advanced Materials are expected to grow at a significant CAGR of 6.9%, reaching USD 152.8 billion by the end of the forecast period in 2034."

Advanced materials, such as composites and titanium alloys, are pivotal in various industries due to their superior properties, including high strength-to-weight ratios, corrosion resistance, and durability. These materials are increasingly utilized in aerospace, automotive, construction, and medical sectors, driving innovation and performance enhancements. The global market for advanced materials is experiencing robust growth, fueled by technological advancements and the rising demand for lightweight and high-performance materials. The adoption of composites and titanium alloys is particularly notable in the aerospace and automotive industries, where there is a constant quest for materials that can enhance fuel efficiency and reduce emissions. Additionally, the construction industry is leveraging these materials for sustainable and resilient infrastructure development. The market's expansion is also supported by increased research and development activities and strategic collaborations among key players to develop innovative solutions that meet the evolving demands of various end-user industries.

North America is the leading region in the advanced materials (e.g., composites and titanium alloys) market, powered by robust aerospace and defense manufacturing, strong presence of key industry players, and increasing investments in lightweight material innovation. Meanwhile, the composites segment is the dominating segment in the market, fueled by rising demand for high-strength, corrosion-resistant materials in automotive, wind energy, and construction sectors, alongside growing emphasis on fuel efficiency and sustainability.

Market Latest Trends, Drivers, Challenges

The advanced materials market is witnessing several noteworthy trends that are shaping its future trajectory. One significant trend is the growing emphasis on sustainability and environmental impact. Companies are increasingly focusing on developing eco-friendly composites and alloys that reduce carbon footprints and promote recyclability. Another trend is the integration of smart technologies into advanced materials, enabling the creation of self-healing composites and alloys with enhanced performance characteristics. Furthermore, the aerospace industry is seeing a surge in the use of titanium alloys due to their ability to withstand extreme conditions while maintaining lightweight properties, which is crucial for improving fuel efficiency and reducing operational costs. Additionally, the automotive sector is embracing advanced composites to manufacture lightweight vehicles that comply with stringent emission regulations and enhance overall performance.

The rise of Industry 4.0 is also influencing the advanced materials market, with increased adoption of automation and digital technologies in manufacturing processes. This shift is leading to more efficient production methods, reduced waste, and improved material properties. Advanced materials are being tailored to specific applications through precise engineering and customization, which is made possible by advanced manufacturing techniques like 3D printing and additive manufacturing. These technologies are not only streamlining production but also enabling the creation of complex geometries that were previously unattainable with traditional methods.

Moreover, the medical sector is benefiting from the advancements in materials science, particularly with titanium alloys being used for implants and prosthetics due to their biocompatibility and strength. The ongoing research and development efforts are focused on enhancing the performance and longevity of these materials, making them more suitable for a wide range of medical applications. The increasing demand for minimally invasive surgical procedures is also driving the adoption of advanced materials that can facilitate precision and improve patient outcomes.

Several key drivers are propelling the growth of the advanced materials market. One of the primary drivers is the increasing demand for lightweight and high-strength materials in the aerospace and automotive industries. The need to improve fuel efficiency and reduce emissions is prompting manufacturers to adopt advanced composites and titanium alloys. Government regulations aimed at reducing environmental impact and enhancing vehicle safety are also contributing to the market growth. Additionally, the rapid urbanization and infrastructure development in emerging economies are boosting the demand for advanced materials in the construction industry. These materials are being used to build sustainable and resilient structures that can withstand extreme conditions and have a longer lifespan.

The growing focus on renewable energy sources is another significant driver for the advanced materials market. Composites and titanium alloys are being used in the production of wind turbines, solar panels, and other renewable energy systems due to their durability and efficiency. The energy sector's shift towards cleaner and more sustainable energy solutions is expected to further accelerate the demand for advanced materials. Moreover, the increasing investment in research and development by both public and private sectors is leading to the discovery of new materials and applications, driving innovation and market expansion.

In the medical field, the rising prevalence of chronic diseases and the aging population are driving the demand for advanced materials used in medical devices and implants. The biocompatibility and superior mechanical properties of titanium alloys make them ideal for orthopedic implants, dental implants, and other medical applications. The advancements in materials science are also enabling the development of next-generation medical devices that offer improved performance and patient outcomes. The increasing healthcare expenditure and the growing emphasis on improving healthcare infrastructure are further supporting the market growth.

Despite the promising growth prospects, the advanced materials market faces several challenges. One of the significant challenges is the high cost associated with the production and processing of advanced materials, particularly titanium alloys and high-performance composites. The complex manufacturing processes and the need for specialized equipment and skilled labor contribute to the overall cost, making it difficult for some industries to adopt these materials on a large scale. Additionally, the availability and sourcing of raw materials, such as rare earth elements used in certain composites, can pose supply chain challenges and affect market stability.

Another challenge is the need for standardized testing and certification procedures for advanced materials. The lack of uniform standards can hinder the adoption of these materials in certain industries, where stringent regulatory requirements and safety standards must be met. This issue is particularly relevant in the aerospace and medical sectors, where material performance and reliability are critical. The development of standardized testing protocols and certification processes is essential to ensure the widespread acceptance and use of advanced materials.

Moreover, the environmental impact of advanced material production and disposal remains a concern. While there is a growing focus on sustainability, the production processes for some advanced materials can be energy-intensive and generate significant waste. Developing more sustainable production methods and improving the recyclability of advanced materials are crucial steps towards mitigating their environmental impact. Addressing these challenges will require collaborative efforts from industry stakeholders, researchers, and policymakers to drive innovation and ensure the sustainable growth of the advanced materials market.

Major Players

1. Hexcel Corporation

2. Toray Industries, Inc.

3. Solvay S.A.

4. SGL Carbon SE

5. Owens Corning

6. Teijin Limited

7. Koninklijke Ten Cate BV

8. Mitsubishi Chemical Holdings Corporation

9. Renegade Materials Corporation

10. DuPont de Nemours, Inc.

11. BASF SE

12. 3M Company

13. VSMPO-AVISMA Corporation

14. Allegheny Technologies Incorporated (ATI)

15. Carpenter Technology Corporation

Market Scope

| Parameter | Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Material Type, By End-User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Material Type:

- Composites

- Titanium Alloys

- Others

By End-User Industry:

Aerospace

Automotive

Construction

Medical

Energy

Others

By Region:

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

FAQ's

The Advanced Materials (e.g., composites, titanium alloys) Market is estimated to reach USD 132.3 billion by 2032.

The Global Advanced Materials (e.g., composites, titanium alloys) Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 6.9% during the forecast period from 2025 to 2032.

The Global Advanced Materials (e.g., composites, titanium alloys) Market is estimated to generate USD 77.6 billion in revenue in 2024.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!