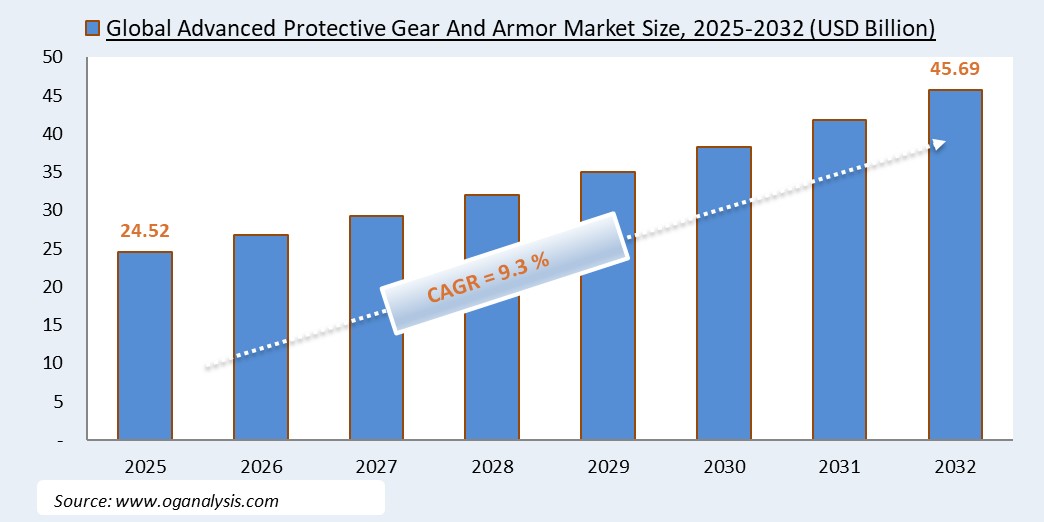

"The Global Advanced Protective Gear And Armor Market is valued at $ 24.52 Billion in 2025. Worldwide sales of Advanced Protective Gear And Armor Market are expected to grow at a significant CAGR of 9.3%, reaching $ 45.69 Billion by the end of the forecast period in 2032."

The global advanced protective gear and armor market is witnessing significant growth driven by rising security threats, increasing military modernization programs, and growing demand for protective solutions across defense, law enforcement, industrial, and civilian sectors. Advanced protective gear and armor include body armor, helmets, protective clothing, and ballistic-resistant equipment designed to provide enhanced protection against bullets, shrapnel, chemical agents, biological hazards, fire, and extreme environmental conditions. Defense forces worldwide are prioritizing the procurement of lightweight, high-strength armor systems that offer superior protection without compromising mobility and operational effectiveness. Additionally, the increasing frequency of military operations, peacekeeping missions, and counter-terrorism initiatives is driving the demand for advanced protective solutions to safeguard personnel in diverse combat and tactical environments.

The market is further supported by technological advancements in materials science, such as the development of aramid fibers, ultra-high-molecular-weight polyethylene (UHMWPE), ceramic composites, and nanotechnology-based coatings that enhance the durability, strength-to-weight ratio, and multi-threat protection capabilities of gear and armor systems. North America holds the largest market share owing to extensive defense budgets, continuous upgrades in soldier protection systems, and strong homeland security investments. Meanwhile, Asia Pacific is emerging as the fastest-growing region due to rising defense spending, border security concerns, and increasing procurement of advanced armor solutions in countries such as China, India, Japan, and South Korea. However, high production costs, stringent regulatory testing standards, and weight optimization challenges for multi-functional protection remain key market constraints. Leading companies are focusing on R&D to develop ergonomic, scalable, and integrated protective solutions for military, industrial, and emergency response applications globally. Overall, the advanced protective gear and armor market is expected to maintain steady growth as safety, survivability, and mission effectiveness remain top priorities across defense and critical infrastructure sectors worldwide.

Body armor is the largest product type segment in the advanced protective gear and armor market due to its extensive use among military personnel, law enforcement, and security forces globally. Its critical role in providing ballistic protection against bullets and shrapnel, combined with continuous advancements in lightweight and multi-threat resistant designs, drives its dominant market share in defense and security applications.

Aramid fibers are the largest material type segment as they offer high strength-to-weight ratios, excellent thermal stability, and superior impact resistance, making them ideal for manufacturing body armor, helmets, and protective clothing. Their widespread adoption in military and industrial protective solutions supports their market leadership over other material categories.

Key Insights

-

The advanced protective gear and armor market is driven by increasing military modernization programs and rising geopolitical tensions worldwide. Defense forces are prioritizing procurement of lightweight, high-strength protective solutions to ensure soldier safety and operational mobility during combat, peacekeeping, and counter-terrorism operations.

-

Body armor and ballistic protection systems remain the largest product segment due to their extensive use among military personnel, law enforcement officers, and security forces. Continuous improvements in ballistic resistance, weight reduction, and ergonomics are supporting their adoption in both developed and emerging defense markets.

-

North America dominates the global market owing to large defense budgets, regular troop deployment, and strong homeland security initiatives. The U.S. Department of Defense continues to invest in advanced soldier protection programs with enhanced survivability, multi-threat resistance, and integrated communication features.

-

Asia Pacific is the fastest-growing regional market driven by increasing defense spending, border security requirements, and modernization programs in China, India, Japan, and South Korea. These countries are investing in advanced protective gear to enhance troop protection and maintain regional security resilience.

-

Technological advancements in material science, such as aramid fibers, UHMWPE, ceramic composites, and nanotechnology-based coatings, are improving the strength-to-weight ratio, thermal resistance, and multi-functional protection capabilities of protective gear and armor systems globally.

-

Integration of sensors and smart technologies in protective gear is emerging as a key trend, enabling real-time health monitoring, environmental sensing, and threat detection for soldiers and first responders, thereby enhancing operational effectiveness and safety outcomes in critical missions.

-

The industrial segment is also witnessing steady demand for protective clothing and gear in hazardous work environments such as mining, oil and gas, chemical processing, and firefighting. Regulatory standards mandating workplace safety are driving investments in certified protective equipment for worker safety assurance.

-

High production costs and stringent testing and certification standards remain market challenges, especially for multi-functional armor solutions. Companies are focusing on cost optimization and design innovations to improve affordability while ensuring compliance with national and international protection standards.

-

Leading players including 3M, Honeywell, DuPont, BAE Systems, Point Blank Enterprises, and ArmorSource are investing in R&D to develop scalable, ergonomic, and integrated protective solutions tailored for military, industrial, and emergency response applications worldwide.

-

The market outlook remains positive as safety, survivability, and mission readiness continue to drive demand for advanced protective gear and armor. Defense and industrial sectors globally are expected to maintain stable procurement pipelines supported by continuous material innovation and safety regulations.

Global crude steel production, 2018–2024 (million tonnes)

Figure: Global crude steel production has risen from about 1.83 billion tonnes in 2018 to around 1.89 billion tonnes in 2024, sustaining the upstream supply base for armor plate and steel-intensive protective systems used across vehicle armor kits, ballistic doors/panels, protective barriers, and structural backings for composite/ceramic solutions. OG Analysis compilation, derived from worldsteel (World Steel Association) world crude steel output data, highlights how a broadly stable global steel production backdrop supports long-term availability of core steel inputs, while specialty plate rolling, heat treatment, and qualification capacity can still drive lead-time and cost volatility for advanced protective gear and armor programs.

World totals are taken from the World Steel Association (worldsteel) time series for world crude steel production (2000–2024) published in World Steel in Figures 2025. The series is used here as a macro upstream capacity indicator relevant to steel-based armor and protective structures; it does not represent armor-grade steel output specifically, which depends on specialty plate capacity, alloying, heat-treatment, and qualification constraints.

Reort Scope

| Parameter | Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By Material type By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Segmentation

By Type

-

Personal armor (vests/soft armor, hard plates, helmets, shields)

-

Tactical protective gear (plate carriers, load-bearing, add-on protectors, ballistic eyewear/gloves)

-

Vehicle armor solutions (add-on kits, spall liners, underbody/blast kits, transparent armor)

-

Structural/infrastructure armor (ballistic doors, wall panels, partitions, ballistic glass)

-

CBRN protective gear

By Threat/Protection

-

Ballistic

-

Blast / fragmentation

-

Stab / slash / spike

-

Multi-threat (hybrid)

By Material

-

Aramid

-

UHMWPE

-

Ceramics (alumina, SiC, B4C)

-

Metals (steel, titanium, aluminum alloys)

-

Hybrid composites

By End User

-

Defense / military

-

Law enforcement

-

Homeland security / border protection

-

Private security / VIP protection

-

Critical infrastructure / industrial security

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key companies

- 3M Co.

- Armorsource Llc

- Avon Protection Plc

- Bae Systems Plc

- Dupont

- Honeywell International Inc.

- Kimberly Clark Professional

- Msa Safety Inc.

- Point Blank Enterprises Inc.

What You Receive

• Global Advanced Protective Gear And Armor market size and growth projections (CAGR), 2024- 2034

• Impact of recent changes in geopolitical, economic, and trade policies on the demand and supply chain of Advanced Protective Gear And Armor.

• Advanced Protective Gear And Armor market size, share, and outlook across 5 regions and 27 countries, 2025- 2034.

• Advanced Protective Gear And Armor market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2025- 2034.

• Short and long-term Advanced Protective Gear And Armor market trends, drivers, restraints, and opportunities.

• Porter’s Five Forces analysis, Technological developments in the Advanced Protective Gear And Armor market, Advanced Protective Gear And Armor supply chain analysis.

• Advanced Protective Gear And Armor trade analysis, Advanced Protective Gear And Armor market price analysis, Advanced Protective Gear And Armor Value Chain Analysis.

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products.

• Latest Advanced Protective Gear And Armor market news and developments.

The Advanced Protective Gear And Armor Market international scenario is well established in the report with separate chapters on North America Advanced Protective Gear And Armor Market, Europe Advanced Protective Gear And Armor Market, Asia-Pacific Advanced Protective Gear And Armor Market, Middle East and Africa Advanced Protective Gear And Armor Market, and South and Central America Advanced Protective Gear And Armor Markets. These sections further fragment the regional Advanced Protective Gear And Armor market by type, application, end-user, and country.

FAQ's

The Global Advanced Protective Gear And Armor Market is estimated to generate USD 24.52 Billion revenue in 2025.

The Global Advanced Protective Gear And Armor Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 9.3% during the forecast period from 2025 to 2032.

By 2032, the Advanced Protective Gear And Armor Market is estimated to account for USD 45.69 Billion.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!