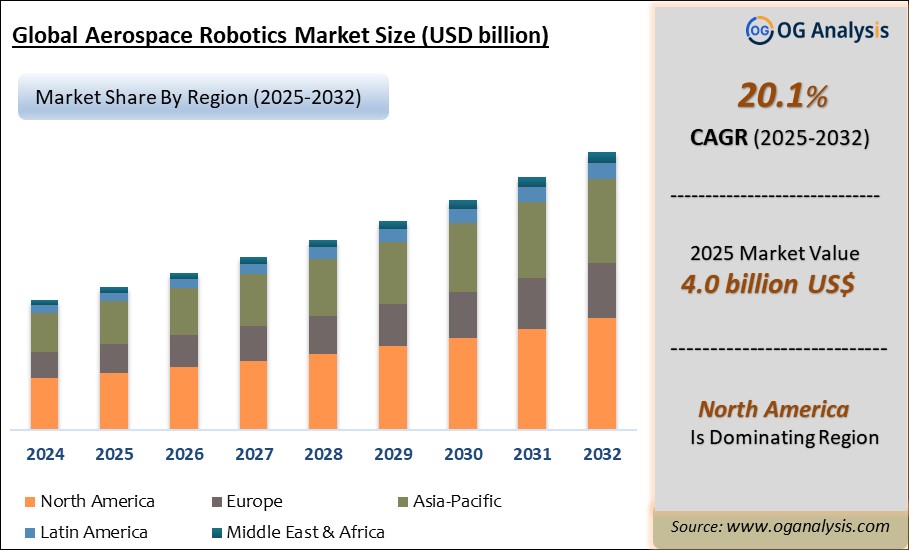

"The Aerospace Robotics Market was valued at $ 4.80 billion in 2026 and is projected to reach $ 20.79 billion by 2034, growing at a CAGR of 20.1%."

The aerospace robotics market is a high-value segment of the advanced manufacturing and automation industry, focused on robotic systems used to improve precision, productivity, safety, and repeatability across aircraft and spacecraft production, assembly, inspection, maintenance, and material handling. Aerospace robots are widely used by aircraft manufacturers, defense contractors, space system producers, component suppliers, maintenance providers, and tiered aerospace supply chains. Key applications include drilling, fastening, welding, painting, composite layup, sealing, inspection, nondestructive testing, material removal, logistics, and automated assembly of wings, fuselage sections, engines, and structural components. Demand is being driven by increasing aircraft production complexity, rising need for lightweight composite structures, labor efficiency requirements, quality consistency expectations, and growing investment in digital manufacturing. Robotics is becoming strategically important as aerospace manufacturers seek to reduce cycle time, improve accuracy, and address skilled labor constraints in high-precision production environments.

Recent trends in the aerospace robotics market include growing adoption of collaborative robots, mobile robotic platforms, AI-enabled inspection systems, automated fiber placement, robotic drilling and fastening, and digital twin-supported production workflows. Manufacturers are focusing on robots that can operate safely near humans, manage complex geometries, integrate with manufacturing execution systems, and support flexible production lines for multiple aircraft programs. Growth is further supported by aircraft fleet modernization, defense aviation programs, space launch activity, and the need for automated maintenance and inspection solutions. Competitive dynamics are shaped by industrial robot manufacturers, aerospace automation specialists, system integrators, aircraft OEMs, and software providers competing on precision, payload capability, programming flexibility, safety features, and integration expertise. At the same time, high capital cost, long qualification cycles, complex certification requirements, and integration challenges continue to influence adoption across aerospace production facilities.

Key Insights

- Aircraft assembly remains one of the most important application areas for aerospace robotics, as robotic systems improve accuracy and repeatability in drilling, fastening, sealing, and structural joining operations. These tasks require high precision and consistent process control because aerospace components must meet strict quality and safety standards. Robotics helps reduce manual variability and supports higher production efficiency across complex aircraft manufacturing programs.

- Composite manufacturing is a major growth driver, with robotics increasingly used in automated fiber placement, tape laying, trimming, and inspection of lightweight structures. As aerospace manufacturers continue adopting advanced composites for weight reduction and fuel efficiency, robotic systems are becoming essential for scalable and repeatable composite processing. This creates opportunities for automation providers with strong material handling and process integration expertise.

- Inspection and nondestructive testing applications are gaining importance as manufacturers seek faster, more consistent quality assurance across aircraft structures, engines, and components. Robotic inspection platforms can improve coverage, reduce human exposure to difficult work areas, and generate digital records for quality tracking. AI-enabled image analysis and sensor integration are strengthening the value of robotics in aerospace quality control.

- Collaborative robots are expanding adoption in aerospace facilities by supporting tasks that require flexibility, human-robot interaction, and lower-volume production environments. Cobots are useful in small-part assembly, tool handling, inspection assistance, and repetitive support tasks where full automation may not be practical. Their ease of deployment and adaptability are helping aerospace suppliers improve productivity without fully redesigning production lines.

- Maintenance, repair, and overhaul operations are emerging as an opportunity area for aerospace robotics, particularly in inspection, surface treatment, cleaning, painting, and component handling. MRO providers are seeking automation that can improve safety, reduce turnaround time, and support repeatable maintenance quality. Robotics is becoming more relevant as aircraft fleets age and maintenance workloads become more complex.

- Defense and space programs are supporting demand for high-precision robotics in specialized manufacturing, propulsion systems, satellite structures, and mission-critical components. These applications often require advanced materials processing, tight tolerances, and secure production environments. Robotics suppliers that can meet aerospace-grade reliability and program-specific customization needs are well positioned in these high-value segments.

- System integration capability is a critical competitive factor because aerospace robotics must work within complex production environments involving large parts, tight tolerances, specialized tools, and rigorous validation procedures. Buyers value suppliers that can provide robotics, tooling, software, safety systems, and process engineering as an integrated solution. Successful implementation often depends on deep aerospace manufacturing expertise.

- Future market growth will be shaped by aircraft production recovery, expansion of composite structures, digital factory initiatives, autonomous inspection, and rising demand for flexible automation in aerospace supply chains. Opportunities will grow where robotics can improve throughput, quality, and worker safety while reducing production bottlenecks. Long-term competitiveness will depend on precision, adaptability, certification support, and seamless integration with digital manufacturing systems.

Regional Analysis

North America Aerospace Robotics Market

North America remains a leading aerospace robotics market, supported by strong aircraft manufacturing, defense production, space programs, and advanced aerospace supply chains. Market dynamics are shaped by demand for precision assembly, robotic drilling, fastening, composite processing, inspection, and MRO automation. Lucrative opportunities are strong in aircraft OEM production lines, defense aviation, space systems, and automated quality inspection. The forecast remains favorable as manufacturers prioritize productivity, labor efficiency, and digital factory transformation, while latest developments focus on collaborative robots, AI-enabled inspection, and flexible automation.

Asia Pacific Aerospace Robotics Market

Asia Pacific is a fast-growing aerospace robotics market, driven by expanding aircraft assembly, rising defense aviation investment, space sector development, and increasing participation in global aerospace supply chains. Market dynamics are influenced by manufacturing localization, growing demand for advanced production technologies, and the need to improve quality consistency across aerospace components. Lucrative opportunities are visible in robotic assembly, composite manufacturing, parts handling, inspection, and MRO support. The forecast remains robust as regional aerospace capabilities strengthen, while latest developments focus on automation adoption, supplier modernization, and technology partnerships.

Europe Aerospace Robotics Market

Europe represents a mature and innovation-led aerospace robotics market, supported by advanced aircraft manufacturing, strong engineering capability, and high adoption of automation in commercial aviation, defense, and space applications. Market dynamics are shaped by demand for precision robotics in fuselage assembly, wing production, composite layup, inspection, and sustainable aircraft manufacturing. Lucrative opportunities are concentrated in automated fiber placement, collaborative robotics, robotic inspection, and digital manufacturing integration. The forecast remains constructive as aerospace companies pursue efficiency, quality, and sustainability, while latest developments center on smart factories, lightweight materials processing, and advanced production automation.

Middle East & Africa Aerospace Robotics Market

The Middle East & Africa aerospace robotics market is developing gradually, supported by defense modernization, aviation infrastructure growth, MRO expansion, and increasing interest in aerospace manufacturing localization. Market dynamics are influenced by investment in aircraft maintenance hubs, unmanned systems, and technology-enabled defense capabilities. Lucrative opportunities are emerging in MRO robotics, inspection systems, surface treatment, parts handling, and defense aerospace support operations. The forecast remains positive as regional aviation and defense sectors expand, while latest developments focus on automation in maintenance, industrial partnerships, and gradual adoption of advanced manufacturing technologies.

South & Central America Aerospace Robotics Market

South & Central America presents emerging opportunities in the aerospace robotics market, supported by aircraft manufacturing capabilities, aviation maintenance demand, defense modernization, and supplier participation in global aerospace programs. Market dynamics are shaped by the need to improve production efficiency, component quality, and maintenance turnaround across aerospace facilities. Lucrative opportunities are visible in robotic inspection, component assembly, painting, material handling, and MRO automation. The forecast remains encouraging as aerospace suppliers modernize operations, while latest developments focus on selective automation, workforce productivity, and improved manufacturing competitiveness.

Market Scope

| Parameter | Aerospace Robotics Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Type, By Application, By Component, By End-User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Type:

- Articulated Robots

- Cartesian Robots

- SCARA Robots

- Cylindrical Robots

- Collaborative Robots

By Application:

- Manufacturing

- Maintenance & Inspection

- Quality Control

- Surface Treatment

- Welding

By Component:

- Controllers

- Sensors

- Drives

- End Effectors

- Others

By End-User:

- Commercial Aerospace

- Defense

- Space

By Region:

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Companies Covered

ABB Ltd., KUKA AG, FANUC Corporation, Yaskawa Electric Corporation, Mitsubishi Electric Corporation, Comau S.p.A., Electroimpact Inc., MTorres Diseños Industriales S.A.U., Broetje-Automation GmbH, Dürr AG, Universal Robots A/S, Nachi-Fujikoshi Corp., Stäubli International AG, Mikrosam AD, ATI Industrial Automation, Güdel Group AG, Janicki Industries Inc., Gemcor Systems LLC, Fives Group, Manz AG.

Recent Developments

- March 2026 – Airbus expanded deployment of automated drilling and fastening robotics across commercial aircraft production programs, strengthening manufacturing efficiency and precision in large aerostructure assembly operations.

- February 2026 – Boeing advanced the use of robotic automation for composite fabrication and aircraft assembly processes, focusing on improving production consistency, reducing rework, and supporting future aircraft manufacturing scalability.

- January 2026 – Spirit AeroSystems increased investment in automated manufacturing technologies, including robotic drilling, fastening, and inspection systems, to enhance productivity and quality across aerostructure production facilities.

- November 2025 – Electroimpact introduced advanced robotic assembly solutions for large aerospace structures, supporting higher production rates and improved precision in aircraft wing and fuselage manufacturing.

- October 2025 – MTorres strengthened its aerospace automation portfolio with next-generation robotic systems for composite processing and automated assembly, targeting increased flexibility and efficiency in aircraft manufacturing environments.

- September 2025 – GKN Aerospace expanded implementation of automated fiber placement and robotic composite manufacturing technologies to support next-generation lightweight aerospace structures and improved production throughput.

- July 2025 – Airbus Helicopters increased the use of robotic inspection technologies and automated manufacturing systems to improve quality assurance, traceability, and production efficiency across rotorcraft programs.

- June 2025 – RTX business Collins Aerospace expanded digital manufacturing initiatives integrating robotics, automation, and advanced inspection technologies to improve aerospace component production and operational performance.

- April 2025 – Lockheed Martin advanced robotic manufacturing applications across defense aerospace programs, focusing on precision assembly, automated inspection, and production efficiency for complex military platforms.

- February 2025 – Northrop Grumman expanded deployment of robotic systems in aerospace manufacturing facilities, supporting automated fabrication, inspection, and material handling for aircraft, space, and defense-related production programs.

FAQ's

The Aerospace Robotics Market is estimated to generate $ 4.80 billion in revenue in 2026.

The Aerospace Robotics Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 20.1% during the forecast period from 2026 to 2034.

The Aerospace Robotics Market is estimated to reach $ 20.79 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!