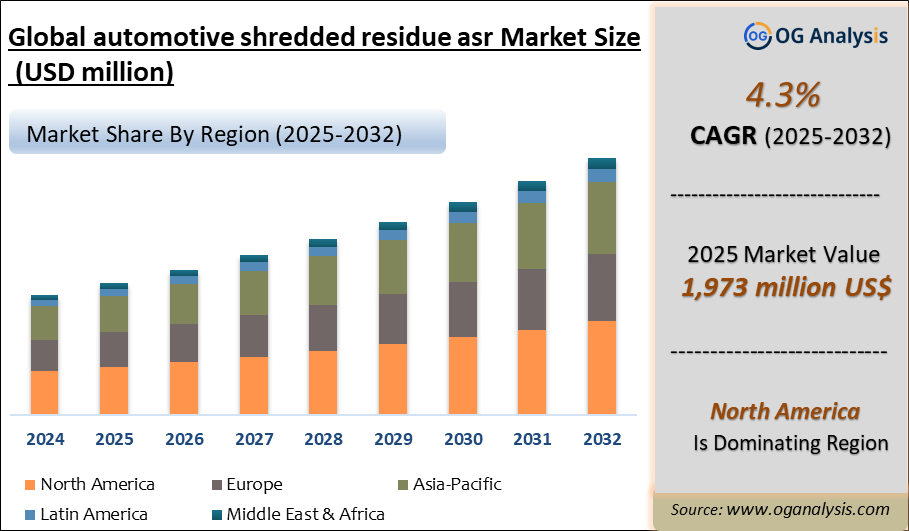

"The Automotive Shredded Residue (Asr) Market valued at $ 2,037 million in 2026, is expected to grow by 4.3% CAGR to reach market size worth $ 2,943. million by 2034."

The Automotive Shredded Residue (ASR) Market is a specialized segment of end-of-life vehicle recycling, waste management, circular materials recovery, and automotive sustainability. ASR refers to the non-metallic material left after vehicles are dismantled, crushed, shredded, and processed for ferrous and non-ferrous metal recovery. It typically contains plastics, rubber, foam, glass, textiles, wood, coatings, wiring residues, fines, dirt, and other mixed materials. ASR management is important for vehicle recyclers, metal shredders, automotive OEMs, waste processors, plastics recyclers, cement producers, energy recovery companies, and regulatory agencies. Traditionally, a large share of ASR has been sent to landfill because of its complex mixed composition, contamination, and difficulty in separating recyclable fractions.

The market is gaining traction as automotive manufacturers, recyclers, and governments focus on landfill diversion, recycled material use, extended producer responsibility, and improved end-of-life vehicle recovery. ASR is increasingly being treated as a resource stream rather than only a disposal problem, with growing interest in plastics recovery, polyurethane foam recycling, rubber separation, mineral fraction recovery, energy recovery, pyrolysis, gasification, and chemical recycling. Regulatory pressure is especially strong in Europe, where new end-of-life vehicle recycling requirements are moving toward stronger reuse, recycling, and recycled-content expectations for vehicles. Recent pilot work also shows rising interest in extracting valuable polymers such as polyamides from ASR, reflecting the industry’s movement toward higher-value material recovery. However, challenges include variable ASR composition, contamination, high separation cost, limited recycling economics, hazardous substance concerns, landfill dependency, technology scalability, and the need for stronger cooperation between vehicle manufacturers, dismantlers, shredders, recyclers, and material buyers.

Regional Analysis

North America Automotive Shredded Residue (ASR) Market

North America represents a mature ASR market, supported by a large end-of-life vehicle recycling base, established dismantling networks, metal shredding infrastructure, and growing interest in landfill diversion. The United States is the key regional market, where millions of vehicles are processed annually through auto recyclers, dismantlers, remanufacturers, and shredders, creating a steady ASR stream after metal recovery. ASR processing opportunities are strongest in plastics recovery, residual metal recovery, foam separation, fines treatment, chemical recycling, and energy recovery. Market dynamics are shaped by landfill costs, environmental compliance, OEM sustainability targets, recycled-content demand, and the economics of separating mixed plastics, rubber, textiles, glass, and contaminants. Growth is expected to remain steady as recyclers invest in more advanced post-shredder separation technologies and as automakers increase focus on circular material use. The U.S. vehicle recycling system already has a broad infrastructure base, with more than ninety-five percent of scrapped vehicles entering organized recycling channels.

Asia Pacific Automotive Shredded Residue (ASR) Market

Asia Pacific is a major growth region for the Automotive Shredded Residue Market, driven by large vehicle fleets, rising scrappage volumes, expanding auto recycling systems, and growing policy focus on resource recovery. Japan is one of the most advanced markets due to its structured end-of-life vehicle recycling framework, where automakers are responsible for handling ASR, airbags, and fluorocarbons under the country’s ELV recycling system. China, South Korea, India, Australia, and Southeast Asian countries are also increasingly relevant as vehicle ownership rises and governments encourage formal recycling channels. Opportunities are strong in ASR plastics sorting, non-ferrous metal recovery, rubber and foam recycling, thermal treatment, and chemical recycling. However, informal dismantling, uneven recycling infrastructure, technology cost, and mixed-material contamination remain challenges in some emerging markets. Japan’s established ASR recycling practices provide a reference model for wider regional adoption.

Europe Automotive Shredded Residue (ASR) Market

Europe is one of the most regulation-driven markets for ASR management, supported by circular economy policies, end-of-life vehicle rules, recycling targets, landfill restrictions, and strong pressure to recover more value from vehicle waste streams. Germany, France, the United Kingdom, Italy, Spain, the Netherlands, Belgium, and Nordic countries are important markets, with demand coming from vehicle dismantlers, shredders, polymer recyclers, energy recovery operators, and automotive OEMs. The region is moving toward stronger vehicle circularity requirements, including mandatory recycled plastic targets and possible future targets for recycled steel, aluminum, and critical raw materials in vehicles. This is expected to increase interest in ASR plastics recovery, solvent-based recycling, chemical recycling, and OEM-recycler partnerships. BASF’s recent pilot work on extracting polyamides from ASR highlights Europe’s focus on higher-value polymer recovery from complex shredder waste.

Middle East & Africa Automotive Shredded Residue (ASR) Market

The Middle East & Africa ASR market is developing gradually, supported by rising vehicle ownership, expanding scrap vehicle flows, metal recycling activity, and growing awareness of environmental waste management. Gulf countries, particularly the UAE and Saudi Arabia, offer opportunities due to organized industrial recycling zones, automotive trade, and investments in waste management infrastructure. South Africa is the most developed African market for vehicle recycling, while Egypt, Morocco, Nigeria, Kenya, and other countries offer gradual opportunities as formal dismantling and metal recovery networks expand. ASR treatment remains limited in many areas because recycling systems are still heavily focused on metal recovery rather than mixed non-metallic residue processing. Key opportunities include residual metal separation, plastics sorting, fuel recovery, cement kiln co-processing, and landfill diversion. Growth will depend on stronger ELV regulations, better dismantling standards, investment in shredder infrastructure, and partnerships with global recycling technology providers.

South & Central America Automotive Shredded Residue (ASR) Market

South & Central America is an emerging market for ASR processing, supported by growing vehicle parc, automotive manufacturing, used vehicle flows, metal recycling, and gradual modernization of waste management systems. Brazil and Mexico are the leading markets due to their large automotive industries and established scrap metal recovery activities, while Argentina, Chile, Colombia, Peru, and other countries provide opportunities in vehicle dismantling, recycling, and industrial waste treatment. The region’s ASR market is still largely shaped by metal recovery economics, with limited high-value recovery of plastics, foams, textiles, and other non-metallic fractions. Growth opportunities are strongest in formal ELV collection, post-shredder separation, residual non-ferrous metal recovery, ASR-to-energy applications, and partnerships with plastics recyclers. However, informal recycling, weak enforcement, limited landfill diversion pressure, technology costs, and uneven recycling infrastructure remain barriers. Future demand will improve as automotive circularity, recycled materials, and environmental compliance become stronger priorities.

Key Insights

- End-of-life vehicle recycling is the core driver of the Automotive Shredded Residue Market. As vehicle fleets age and scrappage volumes increase, shredding operations generate significant quantities of residual non-metallic material that require proper sorting, treatment, recovery, or disposal.

- Landfill diversion is becoming a major market priority because ASR contains recoverable materials that are increasingly viewed as unsuitable for direct disposal. Recycling companies are investing in sorting, density separation, thermal treatment, and chemical recycling routes to reduce landfill dependence.

- Plastic recovery is one of the most important opportunity areas in ASR processing. Vehicles contain growing amounts of polypropylene, polyurethane, ABS, polyamide, PVC, and engineering plastics, creating demand for technologies that can separate, clean, and upgrade mixed automotive plastics.

- Metal recovery remains linked to ASR economics because residual metals can remain trapped in shredded waste streams. Improved post-shredder separation helps recover additional ferrous and non-ferrous metals while improving the quality of remaining non-metallic fractions.

- Chemical recycling is gaining attention for complex ASR plastics that are difficult to recycle mechanically. Pyrolysis, gasification, solvent-based recycling, and depolymerization routes are being explored to convert mixed plastics and polymers into fuels, feedstocks, or reusable raw materials.

- Energy recovery remains relevant where material recycling is technically or economically limited. ASR fractions with suitable calorific value can be used in waste-to-energy systems, cement kilns, or thermal treatment processes, although emissions control and regulatory approval remain critical.

- Automotive lightweighting is influencing ASR composition. Modern vehicles use more plastics, composites, foams, electronics, and specialty materials, which improves vehicle efficiency but makes end-of-life recycling more complex and increases the need for advanced separation systems.

- Electric vehicles are creating new ASR management considerations. EVs contain different mixes of plastics, electronics, insulation materials, battery-related components, lightweight structures, and thermal management materials, requiring adapted dismantling and recycling workflows.

- Regulatory pressure is shaping market growth, especially in regions adopting stronger end-of-life vehicle rules, recycled-content targets, and producer responsibility frameworks. These policies encourage OEMs and recyclers to improve design-for-recycling and recovery performance.

- Future market growth will be shaped by circular economy policies, advanced sorting technologies, automotive plastic recycling, chemical recycling pilots, OEM-recycler partnerships, and demand for lower-landfill vehicle recycling. Companies offering scalable, cost-effective, compliant, and high-recovery ASR processing solutions are expected to remain competitive.

Market Scope

| Parameter | Automotive Shredded Residue (Asr) Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application and By End-User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Composition

- Ferrous Materials

- Non-Ferrous Materials

- Plastics

- Rubber

- Glass

By Application

- Automotive Recycling

- Construction

- Energy Generation

- Agriculture

- Manufacturing

By Shredding Technology

- Single-Stage Shredding

- Two-Stage Shredding

- Three-Stage Shredding

- Cryogenic Shredding

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, South Korea, Rest of APAC)

- The Middle East and Africa (Saudi Arabia,

- UAE, Iran, South Africa, Rest of MEA)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

Recent Developments

April 2026 – Japan introduced a Resource Recovery Incentive System aimed at reducing ASR by encouraging dismantlers to recover plastics and glass before shredding. The system redirects part of ASR recycling funds toward dismantlers that supply recovered materials for recycling.

April 2026 – Japan announced a broader circular economy investment plan to strengthen recycling hubs and recycled-resource supply chains. The plan includes recycled plastic utilization reporting requirements for manufacturers, supporting stronger demand for recovered automotive plastics and ASR-related recycling systems.

December 2025 – European Parliament and Council reached a provisional agreement on new automotive circularity rules requiring recycled plastic content in new vehicle types, with part of the target to come from end-of-life vehicles or removed vehicle components.

October 2025 – BASF and ETH Zurich published study results showing that recycling automotive shredder residue together with biomass through gasification can reduce greenhouse gas emissions compared with incineration for energy recovery.

October 2025 – BASF presented a solvent-based recycling route for polyamides recovered from automotive shredder residue. The pilot extracted polyamides from ASR, purified them, and reprocessed them into PA6 compounds for automotive component validation.

September 2025 – BASF, Porsche, and BEST completed a chemical recycling pilot using automotive shredder residue and biomass in a gasification process. The project evaluated ASR as a future secondary raw material source for high-quality automotive applications.

July 2025 – Toyota Tsusho announced that ASR-derived recycled plastic manufactured by group company Planic was adopted for the first time in a Toyota vehicle in Japan, specifically for the front fender seal of the Crown Sport.

July 2025 – Toyota Tsusho completed the acquisition of Radius Recycling, strengthening its North American recycling network and supporting closed-loop supply chains for high-quality recycled materials from end-of-life vehicles and metal recycling operations.

July 2025 – CEN approved CEN/TS 18084:2025, providing design recommendations for polymeric products used in road vehicles to improve separation and recycling after shredding. The standard supports improved recovery from ASR and post-shredder recycling infrastructure.

FAQ's

The Global Automotive Shredded Residue (Asr) Market is estimated to generate USD 2037.6 million in revenue in 2026

The Global Automotive Shredded Residue (Asr) Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 4.3% during the forecast period from 2026 to 2034.

The Automotive Shredded Residue (Asr) Market is estimated to reach USD 2,943.0 million by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!