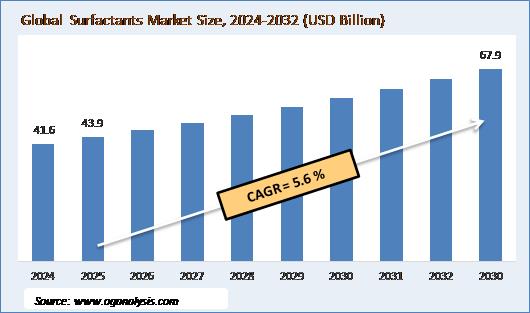

"The Global Surfactants Market is valued at USD 41.6 billion in 2024. Worldwide sales of Surfactants Market are expected to grow at a significant CAGR of 5.6%, reaching USD 64.33 billion by the end of the forecast period in 2032."

Surfactants Market Introduction and Overview

The surfactants market is a dynamic and ever-evolving sector that plays a pivotal role in numerous industries. Surfactants, or surface-active agents, are chemical compounds that reduce surface tension between liquids, solids, and gases. These versatile substances are widely used in industries such as personal care, detergents, agrochemicals, oil and gas, and industrial applications. The growing demand for household and industrial cleaning products, coupled with the expanding application of surfactants in cosmetic formulations, has significantly boosted market growth. In recent years, surfactants have also found their place in the food and beverage, textile, and pharmaceutical industries, further contributing to the market's expansion. Increasing urbanization, a growing consumer base, and shifting consumer preferences towards eco-friendly and sustainable products have provided additional momentum to the surfactants market. Manufacturers are increasingly focusing on innovation and the development of bio-based, biodegradable surfactants to cater to these changing demands, while also addressing environmental concerns associated with traditional surfactants.

The surfactants market is segmented based on product types such as anionic, cationic, non-ionic, and amphoteric surfactants. Among these, anionic surfactants are the most widely used due to their superior cleaning properties and cost-effectiveness. Non-ionic surfactants are also gaining popularity due to their mildness and reduced toxicity, making them ideal for personal care and cosmetics applications. Cationic surfactants, known for their anti-static and antimicrobial properties, find applications in fabric softeners, hair conditioners, and other specialty products. The market's growth is also driven by technological advancements that improve the performance and functionality of surfactants, alongside stringent environmental regulations that promote the shift to more sustainable alternatives. The rise of green chemistry has propelled the demand for surfactants derived from renewable sources, offering eco-friendly options that are biodegradable and have lower toxicity levels. This trend is expected to continue gaining traction as businesses and consumers alike become more conscious of the environmental impact of their purchasing choices, creating new opportunities for market players to innovate and expand their product portfolios.

Trade Intelligence for Surfactants Market

| Global Surface-active preparations Trade, Imports, USD million, 2020-24 | |||||

|

| 2020 | 2021 | 2022 | 2023 | 2024 |

| World | 17,563 | 18,139 | 1,153 | 622 | 187 |

| Guatemala | 48.34 | 56.22 | 80.30 | 99.06 | 104 |

| Trinidad and Tobago | 20.60 | 18.72 | 23.63 | 19.44 | 20.83 |

| Guyana | 6.75 | 11.20 | 11.41 | 13.35 | 12.92 |

| Barbados | 7.65 | 7.63 | 9.02 | 8.92 | 9.25 |

| French Polynesia | 9.27 | 8.19 | 9.71 | 8.32 | 5.67 |

|

| |||||

| Source: OGAnalysis | |||||

- Guatemala, Trinidad and Tobago, Guyana, Barbados and French Polynesia are the top five countries importing 81.5% of global Surface-active preparations in 2024

- Guatemala accounts for 55.6% of global Surface-active preparations trade in 2024

- Trinidad and Tobago accounts for 11.1% of global Surface-active preparations trade in 2024

- Guyana accounts for 6.9% of global Surface-active preparations trade in 2024

| Global Surface-active preparations Export Prices, USD/Ton, 2020-24 |

| |

| Source: OGAnalysis |

Latest Trends in the Surfactants Market

One of the prominent trends in the surfactants market is the increasing shift towards sustainable and eco-friendly surfactant products. Consumers and industries are becoming more environmentally conscious, prompting manufacturers to develop biodegradable and non-toxic alternatives. Bio-based surfactants, derived from renewable resources such as plant oils, sugars, and natural fats, are gaining significant traction. These products are not only sustainable but also perform well in terms of efficacy and safety. In addition to the environmental benefits, bio-based surfactants often meet the growing demand for "green" certifications in various industries such as cosmetics, personal care, and cleaning products. As sustainability becomes a key concern, manufacturers are investing in research and development (R&D) to create surfactants that are both functional and eco-friendly, catering to the evolving demands of the market.

Another key trend is the increasing use of surfactants in personal care and cosmetic formulations. Surfactants are essential in the formulation of a wide range of products such as shampoos, conditioners, body washes, and facial cleansers. With the rising consumer demand for high-quality personal care products, manufacturers are focusing on creating surfactants that offer enhanced skin compatibility, mildness, and improved sensory experiences. The growing trend towards "clean beauty" and the demand for products with fewer synthetic chemicals have driven the preference for surfactants derived from natural sources. Additionally, surfactants are being integrated into new product categories such as anti-aging creams, sunscreens, and other therapeutic skin treatments, further expanding their application range in the cosmetics sector.

Furthermore, the increasing demand for surfactants in the oil and gas industry is an emerging trend in the market. Surfactants play a crucial role in oil recovery, fracking fluids, and enhanced oil recovery (EOR) processes. They are used to reduce the surface tension between the oil and water, which improves the efficiency of extraction processes. As global energy demand rises, there is a greater focus on improving the efficiency of oil and gas extraction techniques, further driving the demand for surfactants. Additionally, surfactants are also employed in cleaning and maintenance activities within the oil and gas industry. The development of surfactants that can perform effectively in high temperatures and harsh conditions is a key area of innovation within this sector, as industries strive to enhance operational efficiency and reduce costs.

Market Drivers in the Surfactants Industry

The surfactants market is experiencing significant growth due to several key drivers. The rising demand for household and industrial cleaning products is a primary factor contributing to the market's expansion. Surfactants are integral components of detergents, surface cleaners, dishwashing liquids, and other cleaning formulations due to their ability to break down grease and remove dirt effectively. As urbanization increases, there is a greater need for cleaning products, especially in emerging economies where disposable incomes are rising, and there is a growing preference for convenience. Additionally, the expansion of industries such as automotive, textiles, and healthcare further fuels the demand for surfactants in cleaning and maintenance applications.

Another significant driver of the surfactants market is the growing demand for personal care and cosmetic products. With the increase in disposable income and changing lifestyles, consumers are becoming more inclined to purchase high-quality skincare, haircare, and beauty products. Surfactants, which are essential for emulsification, foaming, and cleansing in these products, are seeing increased demand. The desire for natural, organic, and sustainably sourced beauty products is also influencing market growth. Consumers are increasingly opting for cosmetics and personal care items that are free from harmful chemicals, driving the demand for mild and bio-based surfactants that meet these standards.

Technological advancements and innovations in surfactant production are further accelerating market growth. Manufacturers are adopting advanced technologies to improve the performance and functionality of surfactants, enhancing their applications in various industries. The growing adoption of green chemistry principles is encouraging the development of sustainable surfactants with lower environmental impact. This shift toward sustainability, combined with the demand for high-performance surfactants, is creating new opportunities for innovation. Furthermore, the rise in research and development activities aimed at improving surfactant formulations to meet the diverse needs of end-users is fostering the market’s evolution. Manufacturers are increasingly focused on creating multifunctional surfactants that cater to the varying demands of sectors like automotive, pharmaceuticals, and oil and gas.

Challenges in the Surfactants Market

Despite its growth potential, the surfactants market faces several challenges that could hinder its development. One of the main challenges is the volatility of raw material prices, particularly the costs associated with petrochemical-based feedstocks. The reliance on petroleum for the production of many conventional surfactants exposes manufacturers to price fluctuations in the global oil market. This unpredictability in raw material costs can create uncertainty for businesses and make it difficult to maintain consistent pricing for surfactants. Additionally, while the demand for bio-based surfactants is rising, the higher cost of production compared to traditional surfactants remains a challenge for manufacturers, limiting their widespread adoption in some industries.

Report Scope

| Parameter | Surfactants Market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By Substrate, By Application, |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

By Product Type

- Anionic Surfactants

- Amphoteric Surfactants

- Cationic Surfactants

- Non-Ionic Surfactants

- Others

By Substrate

- Bio-Based

- Synthetic

By Application

- Personal Care

- Textiles

- Industrial

- Agriculture

- Food and Beverage

- Plastics and Adhesives

- Others

Key Market Players Presented in the Report Include

BASF SE

Stepan Company

Evonik Industries AG

Dow Inc.

Nouryon

Solvay S.A.

Clariant AG

Kao Corporation

Croda International Plc

Indorama Ventures Public Company Limited

Galaxy Surfactants Limited

Oxiteno

SNF Floerger

Inolex

Windtree Therapeutics

Recent Developments

- Pilot Chemical partnered with Novvi LLC to exclusively introduce CalCare® AOS, a biobased alpha olefin sulfonate surfactant, for North American home, industrial, and personal care markets—leveraging renewable feedstock while maintaining high performance.

- Pilot Chemical became the sole sulfonator and distributor of Novvi’s sustainable surfactant line, aiming to begin commercial-scale production at its Ohio facility in the coming months.

- Pilot Chemical also partnered with Kao Corporation to bring Bio IOS®, another bio-based surfactant technology, to the North American market, strengthening its focus on eco-friendly offerings.

FAQ's

The Global Surfactants Market is estimated to generate USD 41.6 Billion in revenue in 2024.

The Global Surfactants Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 5.6% during the forecast period from 2025 to 2032.

The Surfactants Market is estimated to reach USD 64.33 Billion by 2032.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!