Ship Hull Inspection Services Market Outlook 2026–2034: Remote Inspection Trends, Growth Drivers, Leading Companies, and Future Opportunities

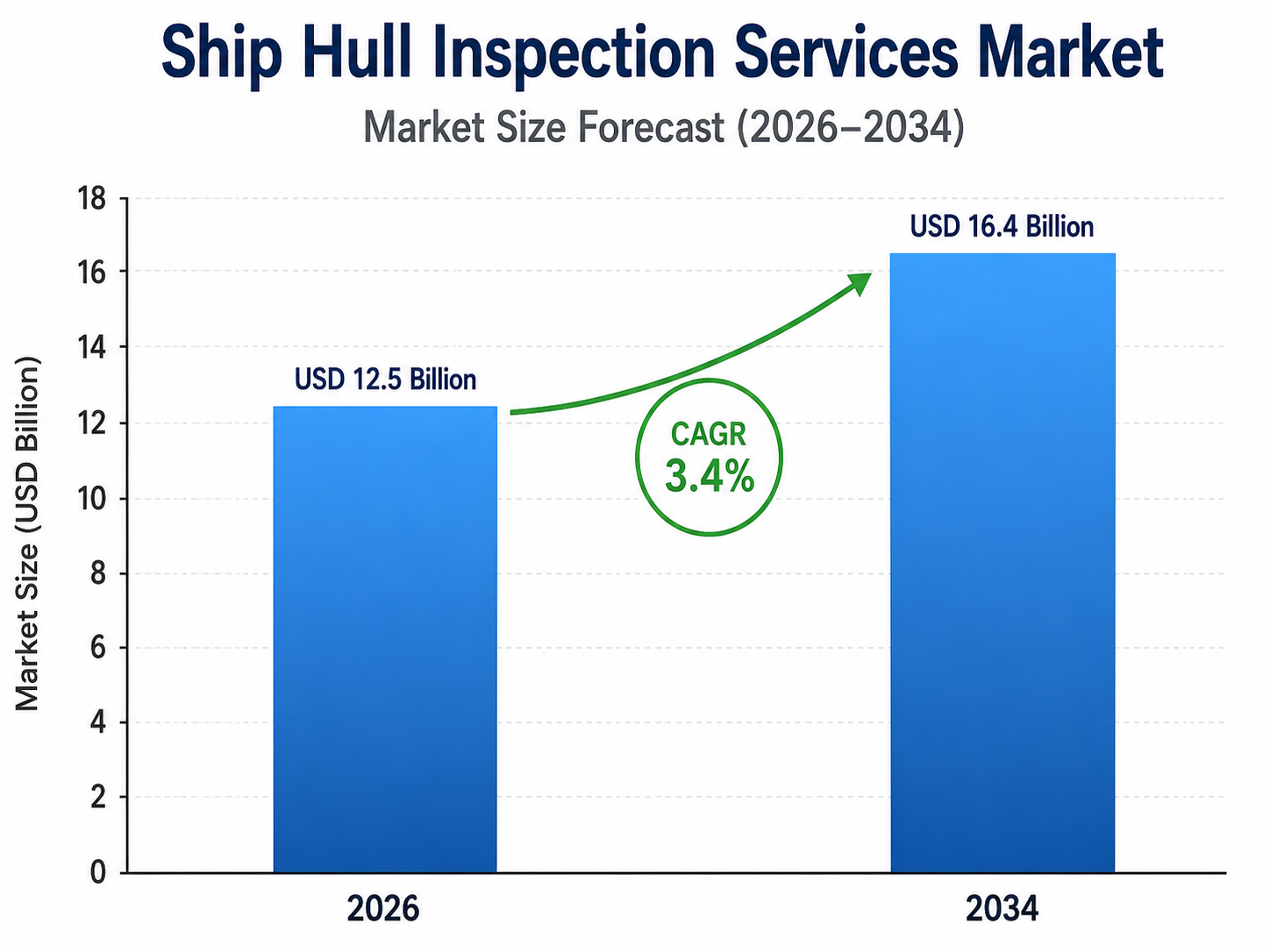

The Ship Hull Inspection Services Market is expected to grow from $ 12.5 billion in 2026 to $ 16.4 billion by 2034, registering a CAGR of 3.4%

During the forecast period. Ship hull inspection services are essential for evaluating the condition and structural integrity of vessels by identifying corrosion, cracks, coating damage, deformation, biofouling, and issues affecting underwater components such as propellers, rudders, and sea chests. These inspections are carried out using a range of methods, including dry-dock surveys, diver-assisted inspections, remotely operated vehicles (ROVs), underwater drones, robotic crawlers, ultrasonic thickness testing, and remote visual inspection technologies. Market growth is being driven by increasing global maritime trade, the aging commercial fleet, mandatory classification and safety inspections, and the need to minimize unexpected maintenance and operational downtime. In addition, shipowners are increasingly investing in digital and robotic inspection technologies to improve inspection accuracy, enhance crew safety, optimize maintenance planning, maintain fuel efficiency, and ensure compliance with evolving maritime regulations.

1. What is the latest trend in the Ship Hull Inspection Services Market?

The latest trend is the growing use of ROVs, underwater drones, robotic crawlers, and AI-assisted image analysis for remote hull surveys.

These technologies capture high-resolution video, sonar data, coating conditions, corrosion evidence, and structural abnormalities without extensive diver deployment.

Digital reporting, 3D hull mapping, and remote participation by classification surveyors are also gaining adoption.

The trend is reducing inspection time, safety risks, and vessel off-hire periods.

2. What are the key challenges in the Ship Hull Inspection Services Market?

Key challenges include poor underwater visibility, strong currents, marine growth, equipment reliability, port restrictions, and variations in class-approval requirements.

Accurate defect detection can be difficult when hull surfaces are heavily fouled or damaged coatings obscure structural conditions.

Service providers also require trained divers, ROV pilots, nondestructive-testing specialists, and certified survey personnel.

Data quality, cybersecurity, and acceptance of remotely collected evidence remain important concerns.

3. What is the major driving factor for the Ship Hull Inspection Services Market?

The major driving factor is the need to maintain vessel safety, regulatory compliance, and operational availability throughout the ship’s lifecycle.

Regular inspections identify corrosion, cracks, coating failure, deformation, biofouling, and propulsion-system damage before major failure occurs.

Rising dry-docking expenses and vessel downtime are encouraging shipowners to use approved in-water inspection alternatives.

Growing maritime trade and an aging global fleet are further increasing recurring service demand.

4. What is the major segment in the Ship Hull Inspection Services Market and why?

Underwater and in-water hull inspection services represent a major segment because they allow vessels to be assessed without complete dry-docking.

These services examine hull plating, propellers, rudders, sea chests, anodes, welds, coatings, and underwater appendages while the vessel remains afloat.

ROV- and diver-supported surveys can lower downtime and support faster repair planning.

Their recurring use across scheduled, emergency, and condition-based inspections sustains market demand.

5. Which application or end-user is driving more demand?

Commercial shipping is driving significant demand, particularly across container ships, bulk carriers, tankers, LNG carriers, and passenger vessels.

These vessels operate under intensive schedules and require regular class, flag-state, insurance, and maintenance inspections.

Offshore support vessels, naval fleets, ferries, and cruise ships also generate important service demand.

Large fleet operators value inspection services that minimize downtime and provide consistent multi-port coverage.

6. Which region offers the highest growth potential and why?

Asia Pacific offers the highest growth potential due to its major shipbuilding centers, large commercial fleets, busy ports, and extensive ship-repair capacity.

China, South Korea, Japan, Singapore, and India are important markets for newbuild surveys, maintenance, dry-docking, and underwater inspection.

The region’s strong position in maritime trade creates continuous demand for hull-condition assessment.

Europe and North America remain important due to stringent compliance standards and advanced robotic inspection adoption.

7. What strategies are major companies adopting in the market?

Major companies are investing in ROV fleets, autonomous inspection systems, ultrasonic testing, sonar imaging, and AI-based defect recognition.

They are expanding class approvals, port networks, rapid-response teams, and standardized digital reporting capabilities.

Partnerships with shipowners, classification societies, shipyards, and marine technology providers are becoming increasingly important.

Companies are also offering integrated inspection, hull cleaning, repair planning, and maintenance services.

8. What are the leading companies in the Ship Hull Inspection Services Market?

Leading participants include DNV, Bureau Veritas, Lloyd’s Register, ABS, SGS, Intertek, Hydrex, Subsea Global Solutions, MME Group, Geo Oceans, and regional underwater survey specialists.

Classification societies provide statutory and class-related survey oversight, while specialist contractors perform diver-, ROV-, drone-, and NDT-based inspections.

Companies compete through geographic coverage, class approvals, response time, inspection technology, and reporting quality.

Providers with global port networks and integrated inspection-and-repair capabilities hold a strong position.

9. Why are ship hull inspection services strategically important for vessel operators?

Hull inspection services help vessel operators prevent structural failures, unplanned repairs, environmental incidents, and costly operational interruptions.

They provide evidence for classification, insurance, maintenance planning, asset valuation, and dry-dock preparation.

Early identification of biofouling and coating damage can also support fuel-efficiency and emissions-reduction objectives.

For fleet managers, inspection data is becoming central to condition-based maintenance and lifecycle cost control.

10. What is the future outlook for the Ship Hull Inspection Services Market?

The market outlook remains positive as fleet operators increase investment in predictive maintenance, remote surveys, and robotic inspection technologies.

Future services will increasingly combine autonomous navigation, AI defect detection, digital twins, sonar, and real-time data transmission.

Regulatory acceptance of remote inspection techniques is expected to widen their use across difficult and hazardous spaces.

Companies offering class-compliant, technology-enabled, and globally scalable inspection services are likely to gain market share.

Browse Related Reports:

https://www.oganalysis.com/industry-reports/pet-supplement-market

https://www.oganalysis.com/industry-reports/paper-and-paperboard-packaging-market

https://www.oganalysis.com/industry-reports/textured-vegetable-protein-market

https://www.oganalysis.com/industry-reports/microgreens-market

https://www.oganalysis.com/industry-reports/flexible-paper-packaging-market