Beer Packaging Market Outlook 2026–2034: Sustainable Cans, Glass Bottle Innovation, Growth Drivers, Leading Companies, and Future Opportunities

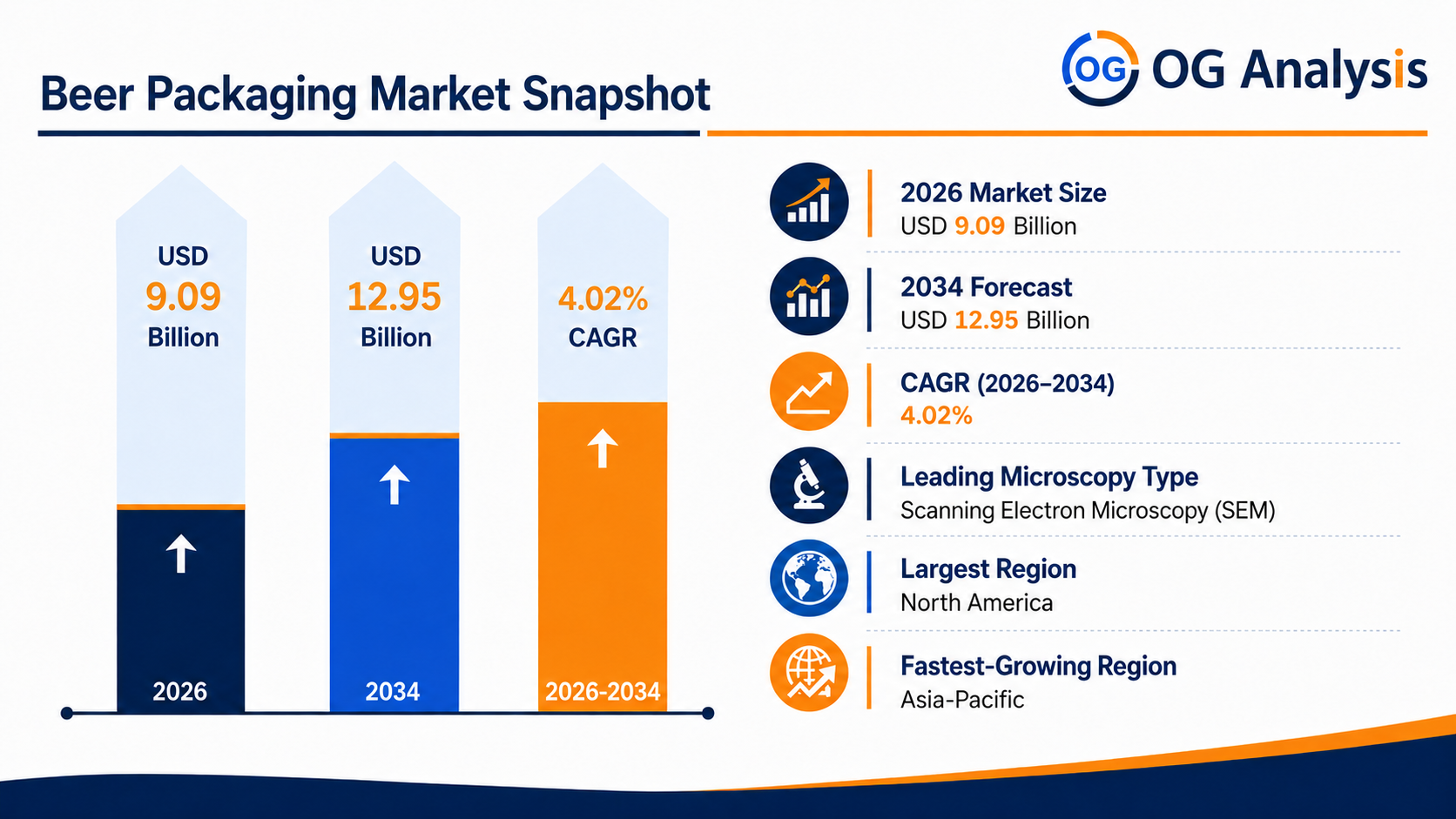

The Beer Packaging Market is estimated to be valued at $ 9.09 billion in 2026 and is projected to reach $ 12.95 billion by 2034, expanding at a CAGR of 4.02% from 2026 to 2034.

Beer packaging includes bottles, cans, kegs, cartons, multipacks, carriers, labels, closures, crowns, caps, and secondary packaging used to protect, transport, brand, and serve beer across retail, on-trade, and export channels. Market growth is supported by rising beer consumption, craft brewery expansion, premiumization, ready-to-drink convenience trends, sustainable packaging demand, and increasing preference for lightweight, recyclable, and transport-efficient formats. Glass bottles remain important for premium and traditional beer branding, while aluminum cans are gaining strong adoption due to portability, light protection, fast chilling, lower breakage risk, and improved recyclability. Kegs continue to serve bars, restaurants, breweries, events, and hospitality channels.

Get Your Free Sample Report for In-Depth Market Insights :

https://www.oganalysis.com/industry-reports/beer-packaging-market

1. What is the latest trend in the Beer Packaging Market?

The latest trend is the rising adoption of aluminum cans, lightweight bottles, recyclable packaging, and premium label designs.

Brewers are using packaging to improve shelf visibility, support brand storytelling, and attract younger consumers.

Craft breweries are increasingly choosing cans because they are portable, protect beer from light, and support colorful full-body artwork.

Sustainability trends are also pushing companies toward recycled aluminum, lighter glass, returnable bottles, and reduced secondary packaging.

2. What are the key challenges in the Beer Packaging Market?

Key challenges include glass and aluminum price volatility, energy-intensive manufacturing, packaging waste regulations, and supply-chain disruptions.

Brewers must balance packaging cost, product protection, shelf appeal, logistics efficiency, and sustainability targets.

Small breweries may face higher unit costs for custom cans, printed labels, bottles, cartons, and minimum order volumes.

Deposit-return systems, recycling rules, and extended producer responsibility policies are also shaping packaging decisions.

3. What is the major driving factor for the Beer Packaging Market?

The major driving factor is growing demand for convenient, safe, attractive, and sustainable beer packaging across retail and on-premise channels.

Packaging plays a critical role in protecting beer quality from oxygen, light, contamination, and handling damage.

Rising craft beer launches, premium beer branding, and flavored or low-alcohol beer innovation are increasing demand for differentiated packaging.

Growth in supermarkets, convenience stores, online alcohol delivery, and event consumption is further supporting packaged beer sales.

4. What is the major segment in the Beer Packaging Market and why?

Cans are a major packaging segment because they are lightweight, portable, stackable, recyclable, and suitable for both mass-market and craft beers.

They protect beer from light exposure and are less prone to breakage compared with glass bottles.

Glass bottles remain highly important in premium, returnable, export, and traditional beer formats due to their strong brand appeal.

Kegs are also significant for draught beer consumption in bars, restaurants, breweries, festivals, and hospitality venues.

5. Which application or end-user is driving more demand?

Breweries, craft beer producers, beverage brands, pubs, bars, restaurants, hotels, retailers, and distributors are driving demand.

Large breweries require high-volume bottles, cans, crowns, labels, carriers, and secondary packaging for mass distribution.

Craft brewers demand smaller-batch cans, custom labels, specialty bottles, shrink sleeves, and branded multipacks.

On-trade channels continue to support keg demand, while retail and e-commerce channels support cans and bottled beer packaging.

6. Which region offers the highest growth potential and why?

Asia Pacific offers strong growth potential due to rising beer consumption, urbanization, expanding middle-class spending, and growth in modern retail.

China, India, Japan, South Korea, Vietnam, Thailand, and Australia are important markets for packaged beer and beverage packaging.

North America remains important due to craft beer activity, canned beer adoption, and strong retail distribution.

Europe is supported by premium beer culture, returnable glass systems, draught beer demand, and strong sustainability regulation.

7. What strategies are major companies adopting in the market?

Major companies are focusing on lightweight packaging, recycled content, returnable systems, premium printing, smart labeling, and improved barrier performance.

Can makers are expanding aluminum beverage can capacity, while glass manufacturers are improving lightweight and refillable bottle designs.

Packaging suppliers are offering customized labels, sleeves, secondary packs, multipack carriers, and sustainable closure solutions.

Companies are also strengthening partnerships with breweries, beverage brands, distributors, and recycling-system operators.

8. What are the leading companies in the Beer Packaging Market?

Leading companies include Ball Corporation, Crown Holdings, Ardagh Group, O-I Glass, Amcor, CANPACK, Smurfit Westrock, Berry Global, TricorBraun, ALPLA, Berlin Packaging, AGI glaspac, THIELMANN, INOXCVA, and Gamer Packaging.

These companies compete through material quality, design capability, production scale, sustainability performance, supply reliability, and customer relationships.

Ball and Crown are major players in aluminum beverage packaging, while O-I and Ardagh are important in glass bottle packaging.

Grand View Research also identifies Ardagh Group, Amcor, ALPLA, Berry Global, Smurfit Westrock, Crown Holdings, CANPACK, and Ball Corporation among key beer packaging players.

9. Why is beer packaging strategically important for brewers?

Beer packaging is strategically important because it protects taste, freshness, carbonation, shelf life, and brand identity.

The right packaging format helps brewers reach different channels such as retail shelves, bars, festivals, exports, and online delivery.

Packaging also influences consumer perception, premium positioning, product differentiation, and repeat purchase behavior.

For breweries, packaging choices directly affect logistics cost, sustainability performance, regulatory compliance, and market competitiveness.

10. What is the future outlook for the Beer Packaging Market?

The market outlook remains positive as brewers continue investing in sustainable, lightweight, premium, and convenient packaging formats.

Future growth will be supported by aluminum cans, returnable glass bottles, recyclable multipacks, digital printing, smart labels, and eco-friendly carriers.

Craft beer, premium beer, low-alcohol beer, flavored beer, and export-oriented beer brands will create demand for differentiated packaging.

Companies offering reliable supply, strong design support, sustainable materials, and cost-efficient packaging solutions are expected to gain market share.

Browse Related Reports

https://www.oganalysis.com/industry-reports/food-grade-gases-market

https://www.oganalysis.com/industry-reports/ecommerce-packaging-market

https://www.oganalysis.com/industry-reports/point-of-purchase-packaging-market

https://www.oganalysis.com/industry-reports/paper-and-paperboard-packaging-market

https://www.oganalysis.com/industry-reports/beer-market

Stay Connected With Us